Apollo: Don’t mistake the sprinkle for the cupcake.

Fundraisings from Arctos, BlackRock, Santander Alternative Investments and Accession Capital Partners.

👋 Hey, Nick here. A big welcome to the new subscribers from Golborne Capital, Point72, and Audax Private Debt. You’re now part of a select group of 3,167 subscribers, reading the 175th edition of my private credit newsletter.

If you’re reading this on Outlook, most of the graphs won’t show. I’d recommend you read it online

Apollo: Don’t mistake the sprinkle for the cupcake.

You may question Apollo’s market sizing numbers, but its marketing is memorable.

👉 Learn how Apollo aims to lead with investment-grade private credit.

📕 Reads of the Week

“Periods of volatility [are] usually the best time to invest capital...

People are nervous, capital structures are a little more conservative, and pricing is a little wider.”

Brad Marshall, Global Head of Private Credit Strategies, Chairman and Co-CEO of BCRED and BXSL

Market Updates

Ares on Real Estate

“For the first time in a while, mainstream commercial property looks ‘cheap’ on an income basis, relative to most other major asset classes.

Not every commercial building screams “bargain.” Yet at the portfolio level, prices have dropped far enough for investors to feel more confident about the risk/reward profile — particularly in sectors with stabilizing fundamentals and falling supply.

That distinction matters for those who worry about “trying to catch a falling knife.” In much of the market, the knife is just sticking up out of the floor, waiting for someone to get the handle.

Avoiding SaaSpocalypse is an underwriting skill for lenders

Headline software exposure numbers are becoming less useful on their own.

Two private credit managers may report identical software allocations while holding radically different underlying risks depending on the durability of the businesses they finance.

Pimco estimates that $5 trillion in total AI-related capex is expected by 2030.

~40% may need to be financed through debt markets.

Demand has been so strong that one lender described it as a “food fight.” 🍔

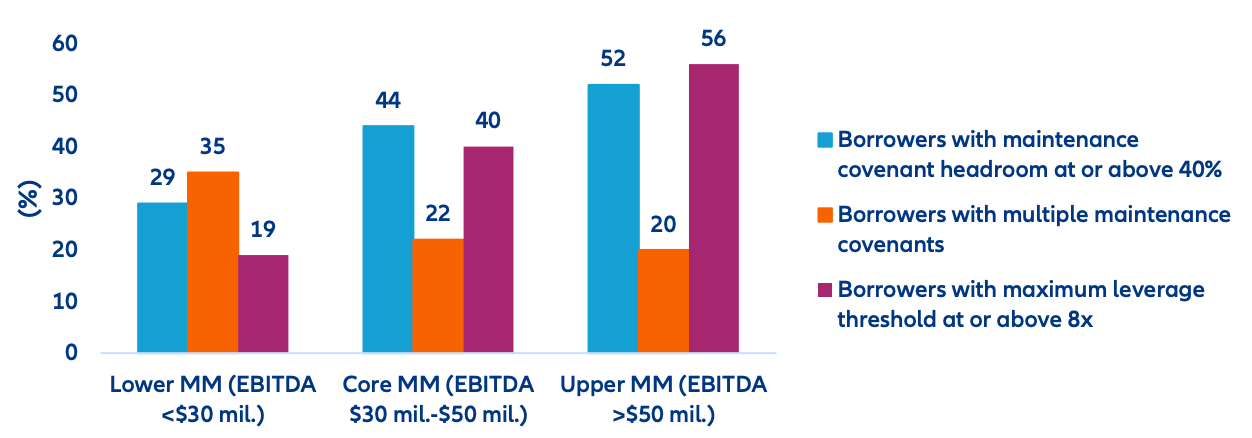

The weakening of maintenance covenants in private credit

An analysis of over 2,000 private credit agreements shows that more than a third of borrowers with maintenance covenants carry headroom exceeding 40%.

Not because they have deleveraged, but because covenants were set wide at origination to win mandates in a competitive deployment environment.

Manager Updates

Mubadala is opening its private credit platform to external investors for the first time as it seeks to attract institutional capital.

Mubadala will transfer a $25 billion credit portfolio to Mubadala Capital, allowing the investment business to raise third-party funds alongside capital from its parent for the first time.

Mubadala will also commit an additional $4.65 billion to support the platform’s continued expansion.

HSBC pulls back from private credit. Link

Temasek will double its private credit allocation by 2031

The Nor’easter Problem

In February 2026, a nor’easter shut down much of the East Coast for the better part of two days. More than 8,000 flights were cancelled. And then the storm passed. The runways were plowed, the airports reopened, the clouds cleared, and the sun was shining… and frustrated travelers still could not get home.

The reason was the queue. Two days of cancelled flights had created a backlog of displaced passengers that vastly exceeded the number of remaining seats on any given day. Most flights are booked in advance with over 80% utilization. People are booked to fly unrelated to the storm. Travelers looking to rebook that morning simply have to grab the few seats left then join the back of a line that was already days long. It took most of a week for the system to clear, long after the event that caused it had become a memory.

This is the most important thing to understand about the redemption pressure now building across non-traded private credit funds. The prevailing assumption, stated explicitly by many managers is that once sentiment normalizes and the headlines fade, the redemption queues will resolve.

That is the “the storm has passed, so we must be fine” fallacy. The storm passing is necessary, but nowhere near sufficient. What governs how long investors wait is not when requests stop rising, but how large a backlog accumulated and how slowly the exit can clear it.

👉 After the Storm: Why Private Credit Redemption Queues Will Endure

2026 Private Credit Rankings

PERE’s Inaugural Credit 100

Infrastructure Investors’ Debt 30

Private credit may be the market’s favourite talking point, but Apollo argues much of the debate is focused on the wrong segment.

John Zito joked that he is asked about private credit “nine times a day”, despite viewing it as a relatively safe and unexciting asset class.

More importantly, John believes direct lending is only a small part of Apollo’s business. People forget that private investment-grade credit is the much larger exposure.

💰Fundraising News

Arctos, a KKR-owned manager, closed its $6.2 billion Keystone Partners Fund I. The Keystone platform offers flexible, non-dilutive capital solutions for GPs across private markets and will target relationships with sponsors in North America and Europe. To date, more than 30% of the Fund’s capital has been deployed across 11 sponsors. This includes Keystone’s backing of Hayfin’s management buyout from British Columbia Investment Management Corporation. More here and here

BlackRock held a first close of $1.7 billion for its European Middle Market Private Debt Fund II. The fund will finance European mid-market companies in defensive industries such as healthcare, business services, and software/technology. More here

Santander Alternative Investments, the alternatives asset manager of Santander Bank, announced a first close of $170 million for its second Asset Backed Corporate Lending Fund. The fund provides asset-backed corporate financing to SMEs across Europe. The fund is targeting a total raise of €500 million, with a final closing scheduled for June 2027. More here

Accession Capital Partners, a Poland-based manager, held a first close of ~$100 million for its first direct lending fund. ACP Credit will focus on high-growth small- and medium-sized companies in Central Europe. It will lend between €5-15 million per deal of senior-secured debt. The fund, which has a target of up to €200 million. More here

This newsletter is for educational and entertainment purposes only. It should not be taken as investment advice.