Bain & Company: Lunch and a handshake simply won’t cut it anymore

The State of Private Equity in 2026

👋 Hey, Nick here. A big welcome to the new subscribers from Zobito, TCW and Thomson Reuters. You’re now part of a select group of 2,570 subscribers. This is the 157th edition of my weekly newsletter.

One favour to ask: if you like this, please share it with a friend. If someone forwarded this to you, you can subscribe here.

If you’re reading this on Outlook, most of the graphs won’t show. I’d recommend you read it online

📕 Reads of the Week

Market Updates

If the private credit market goes through as UBS said, a 15% default rate, the idea that the public high yield and public equity market would be completely fine is extremely unlikely. To say we shouldn’t worry about these other markets when in fact we’re senior debt on all these other markets, there’s not really logic behind this.

Barings: Digital infrastructure varies widely in quality. Many deal have already encountered challenges, and we expect more to follow. We’re extremely selective and these are a very small proportion of our portfolio. More here

Apollo: Dispersion in private markets is meaningfully wider than in public markets.

Manager selection matters.

Ares: Private credit has consistently offered durable income at a premium

Manager Updates

🔉HPS’s Scott Kapnick on The Next Wave in Private Credit Link.

🔉RECOMMENDED LISTEN: Ares’ Joel Holsinger on Asset-Based Finance. Link

BDC Updates

“In the first quarter of 2026 , HLEND received shareholder requests to repurchase approximately 9.3% of shares outstanding as of December 31, 2025, exceeding the 5% framework for the first time since its inception…

BCRED meets its record 7.9% redemption request. Link

PIMCO: Don’t Mistake Private Credit for Just BDCs. Link

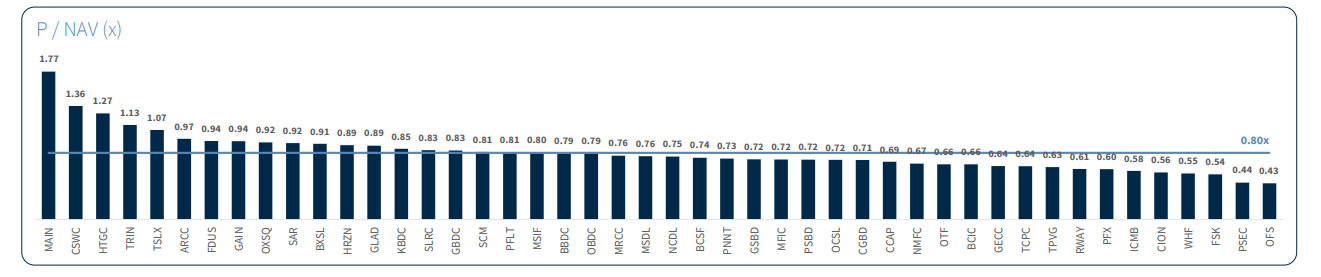

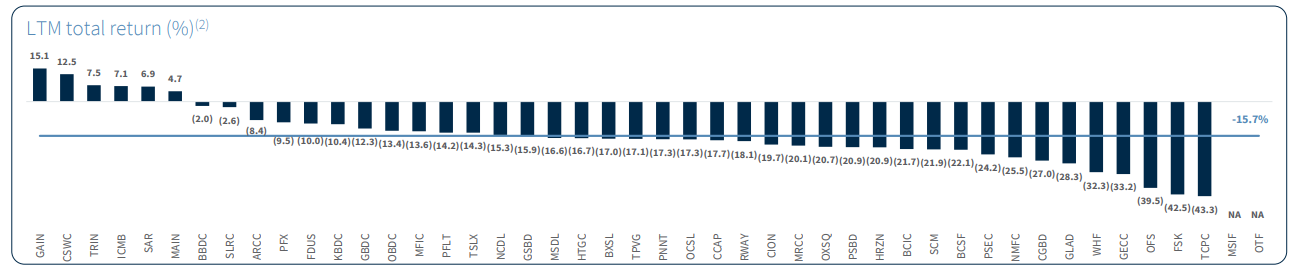

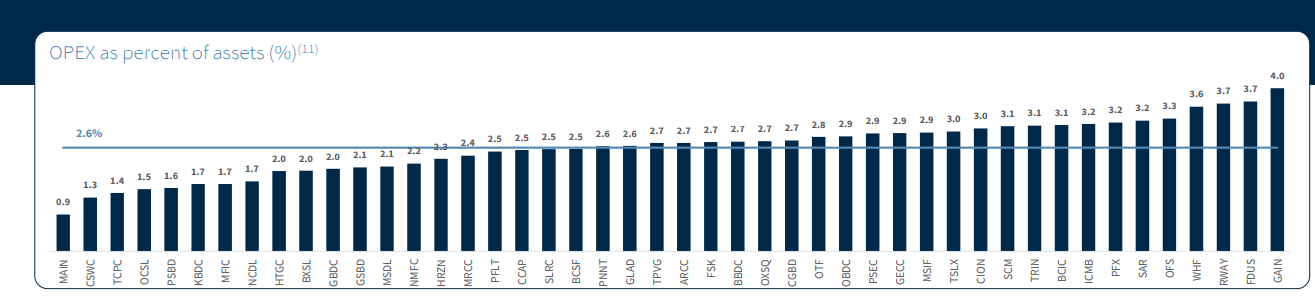

Raymond James BDC Update

Raymond James posted a great update on BDCs.

Three of my favourite charts below

BDCs Trade Around 0.8x NAV, with Significant Dispersion

LTM Total Returns Averaged -15.7%

BDCs Generate Meaningful Fees for Managers

Partnership Updates

AlbaCore partnered with MUFG to launch an infrastructure debt platform. The fund will finance UK and European infrastructure projects. Link

Barings partnered with U.S. farmland investor Homestead Capital to launch a $300 million asset-based finance program. Homestead acquires, finances, and manages diversified portfolios of high-quality farmland assets. With operations across much of the U.S., Homestead’s credit strategy provides capital solutions to borrowers ranging from small and mid-sized farmers to large, vertically integrated agribusinesses. Link

Bain & Company: Lunch and a handshake simply won’t cut it anymore

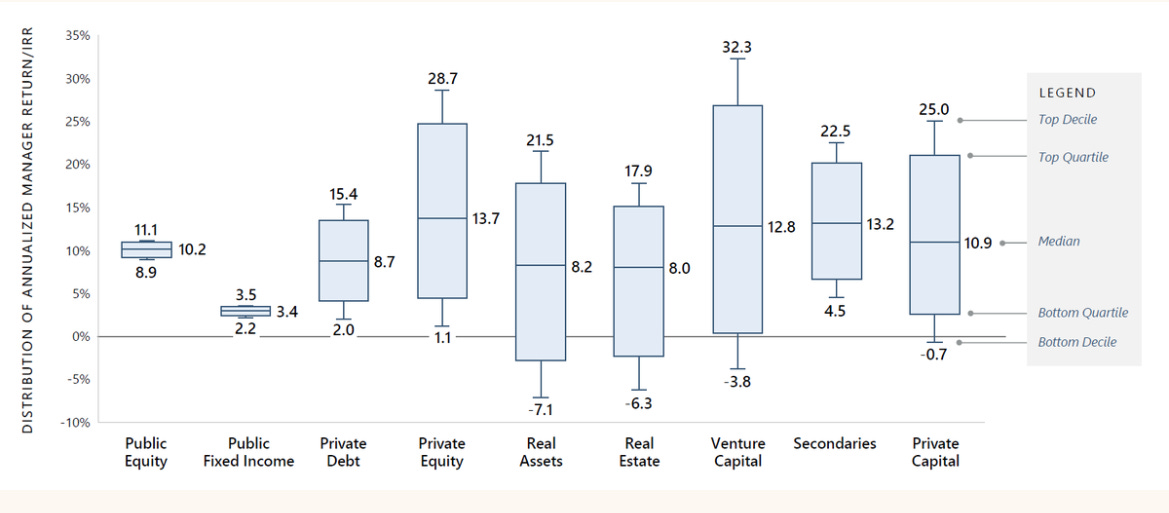

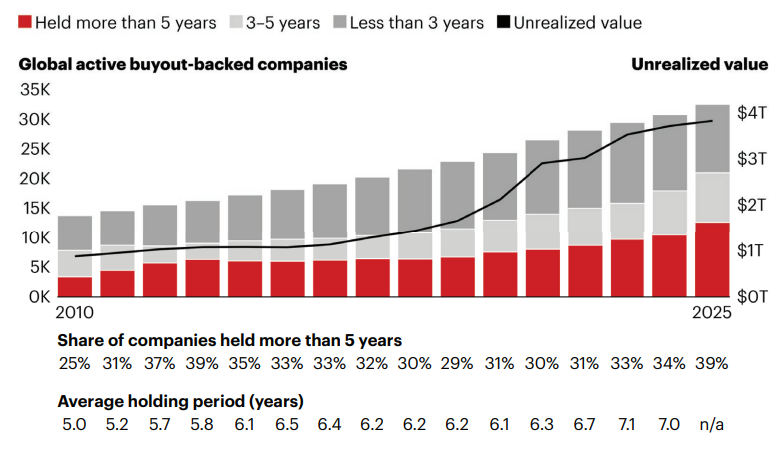

This week’s feature is not strictly about private credit. But Bain’s Private Equity Report is an excellent all-round read. Below are my key takeaways. I’d also recommend reading why 12 is the new 5.

Average hold periods have steadily increased since 2017.

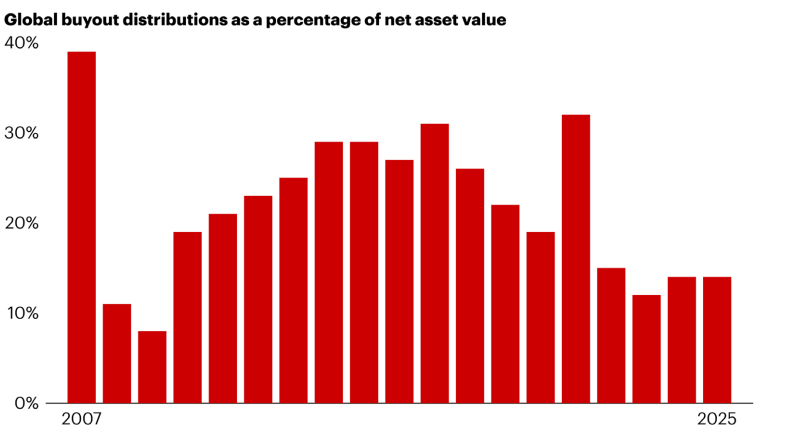

But global distributions as a share of net asset value are at multidecade lows

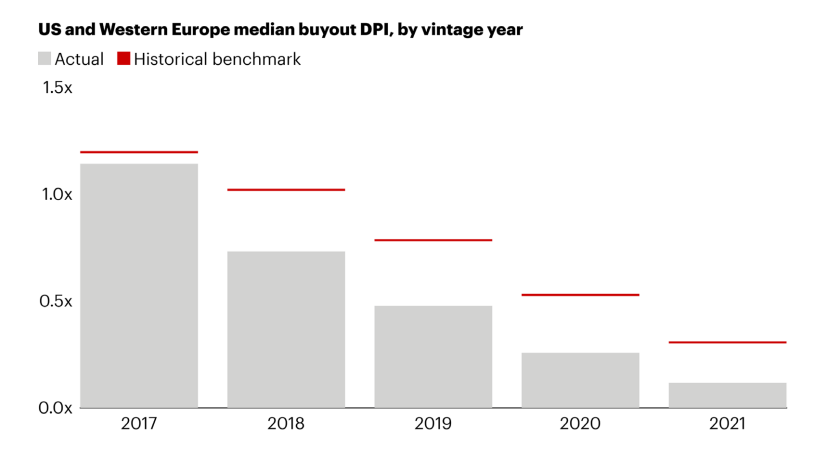

The root problem can be seen in DPI for recent fund vintages.

Looking at the cohort from 2017 to 2021, GPs have underdelivered vs. historical performance for every vintage.

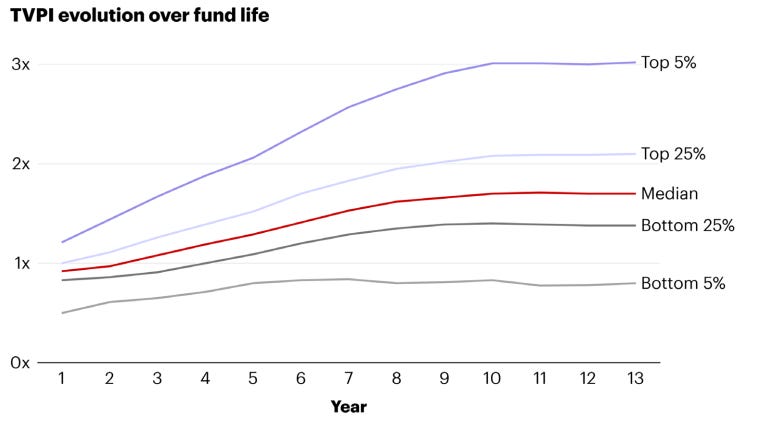

TVPI begins to flatten after year eight

And IRR starts to fall off even earlier.

A hard look at each asset in the portfolio throughout the hold and ask a key question: Is there really more value to be realized here, and what would it take to capture it? If the answer is “the juice isn’t worth the squeeze,” then sell it and move on.

None of this is exactly new.

With distributions to investors in drought stage for four years running, it’s no surprise that fund-raising continued to lag in 2025.

The GPs attracting capital in this period of scarcity are those that have delivered both strong returns and steady distributions.

LPs have become significantly more demanding. Increasingly, they are looking for top-quartile returns from recent funds as well as consistent, top-quartile DPI across funds.

Not only is it critical for a fund to be able to define and articulate a truly differentiated and repeatable strategy, focusing on sector specialization, world-class capabilities, or whatever else separates it from its peers.

The most effective firms are also transforming how they communicate that strategy in the marketplace. A professionalized investor relations capability is rapidly becoming table stakes in the buyout world. These organizations define the market clearly and learn what specific LPs want to hear in terms of metrics, coinvestment opportunities, fees, and DPI.

They target the right decision makers with well-crafted sales plays and ensure that the right message is getting to the right “customer.” Old-school networking still matters, of course. But lunch and a handshake simply won’t cut it anymore, even for firms that have been around for decades.

💰Fundraising News

Sound Point Capital, a New York-based alternative credit manager, closed its $1.5 billion Strategic Capital Fund III. The fund originates loans secured by cash-generative collateral, including accounts receivable, equipment, inventory, and other asset-based assets. More here

360 One, an Indian alternative asset manager, announced a final close of $400 million for its fifth vintage private credit strategy. The fund will continue providing structured and customised credit solutions to the established Indian companies. More here

Avila Real Estate, a US-based private credit platform, announced a second close of $200 million for its latest real estate debt fund. The fund provides senior credit solutions to land developers and homebuilders, including project-level, first mortgage loans for land development and first lien revolver facilities to support vertical construction. Combined with Hillwood as an anchor LP, the fund has some of the largest builders and developers in the country supporting the strategy. More here

Partners for Growth, a California-based credit manager, launched a $180 million fund for later-stage, technology-focused borrowers. The PFG Income Fund has completed a first close and begun deploying capital. The fund will invest in structured growth debt, asset-backed financing and warehouse funding, including for fintechs and alternative lenders building loan and asset book. More here

This newsletter is for educational and entertainment purposes only. It should not be taken as investment advice.