BDC Redemption Season Is Back

Fundraisings from Crescent Capital Group, Eurazeo, HSBC AM, PGIM,

👋 Hey, Nick here. A big welcome to the new subscribers from Quareo Capital, Apogem Capital and Castlelake. You’re now part of a select group of 3,070 subscribers, reading the 170th edition of my private credit newsletter.

If you’re reading this on Outlook, most of the graphs won’t show. I’d recommend you read it online

📕 Reads of the Week

Market Updates

Mercer’s Guide to GP-Led Continuation Vehicle Terms:

Management fees typically range between 0.75-1.00%. This hasn’t changed over the past five years.

Nearly all vehicles used tiered carry structures with an average of nearly 3 tiers and a maximum carry of 20%,

GPs commit between 6% and 10%.

Watch out for the deferred payments…

17Capital: NAV loans uncovered. Link

Ares: A Comprehensive Guide to Private Infrastructure. Link

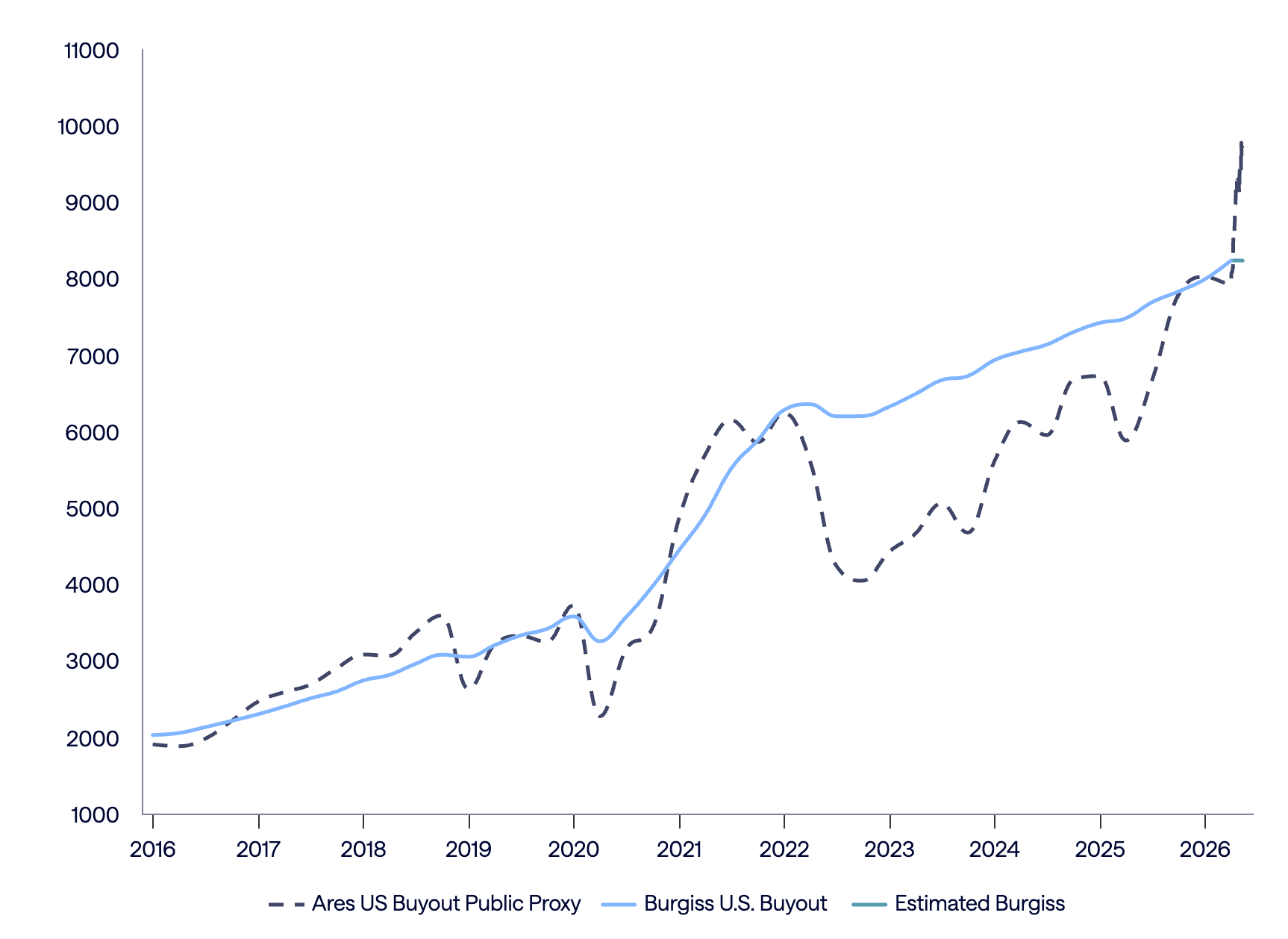

Ares: Public Market Valuations Overtake Private Markets. Link

Manager Updates

Fasanara Capital launched its Ferrari Lending Platform. The platform is a partnership with Mattioli Automotive Group and will allow Fasanara to originate and manage loans secured by Ferrari cars. Link

Partnership Updates

Blackstone signed a new private credit partnership with Nippon Life, one of Japan’s largest insurers. As part of the agreement, Nippon expects to allocate at least $9.4 billion to Blackstone’s private credit and structured credit strategies over the next five years. More here

Your chance to buy alleged MFS fraudster Paresh Raja’s Ferrari.

European Prestige UK Limited, a dealer in “luxurious, high-performance and limited-production vehicles”, is the lucky buyer of Raja’s 8 supercars. Readers interested in owning a piece of financial scandal history will doubtless be hitting refresh on the listings on their website. (Source FT:here)

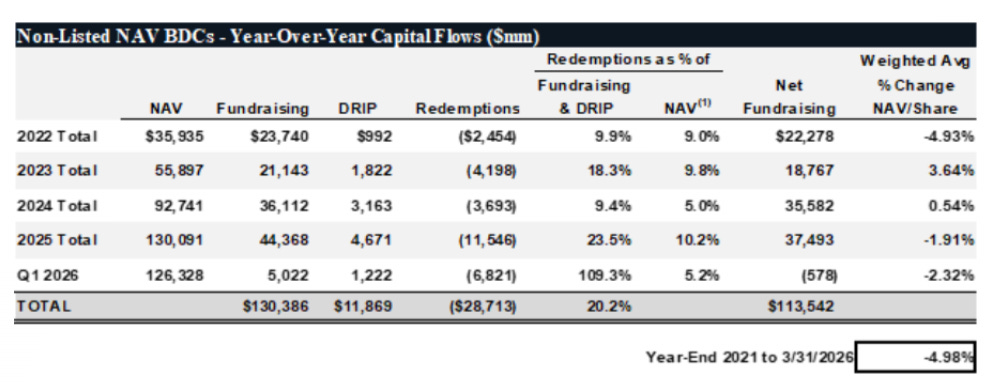

BDC Redemption Season is Back

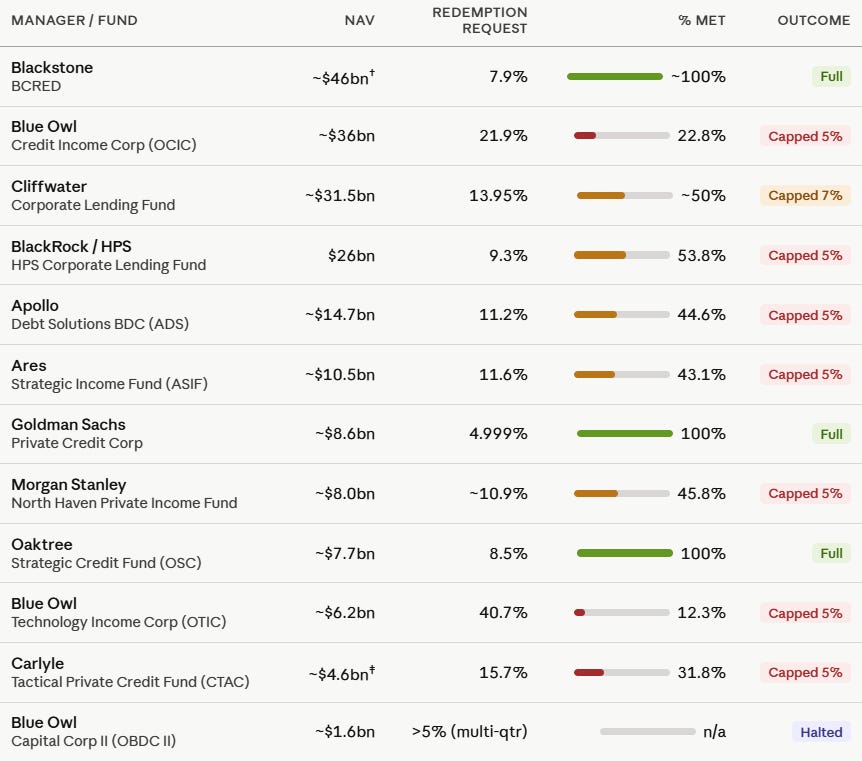

If you missed Season 1 of BDC redemptions, here’s a recap of what happened in Q1:

Non-traded BDC redemption requests averaged ~10%.

Most managers capped payouts at 5%.

Blackstone and Oaktree decided to meet the full redemption requests.

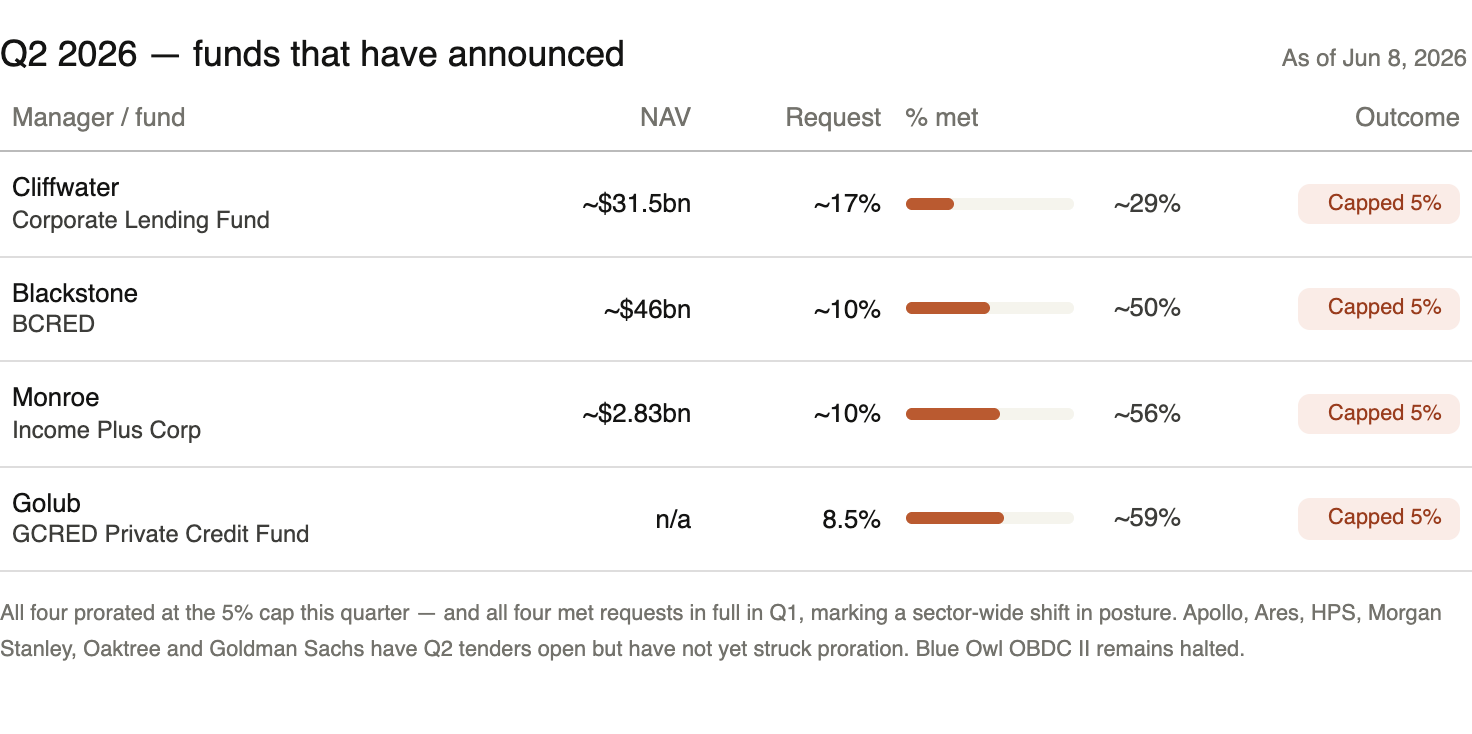

BDCs Q2 Updates: Week 1

Last week saw the first wave of redemption announcements:

Redemption requests have increased for all managers so far.

Cliffwater’s redemption requests increased 20% QoQ.

All managers have decided to cap at 5%.

Season 2 Spoilers

Redemption requests will likely increase for all managers.

Most managers will cap at 5%.

Expect some fairly dramatic headlines.

So before your uncle forwards you an article asking if everything is okay, here are a few points worth keeping in mind.

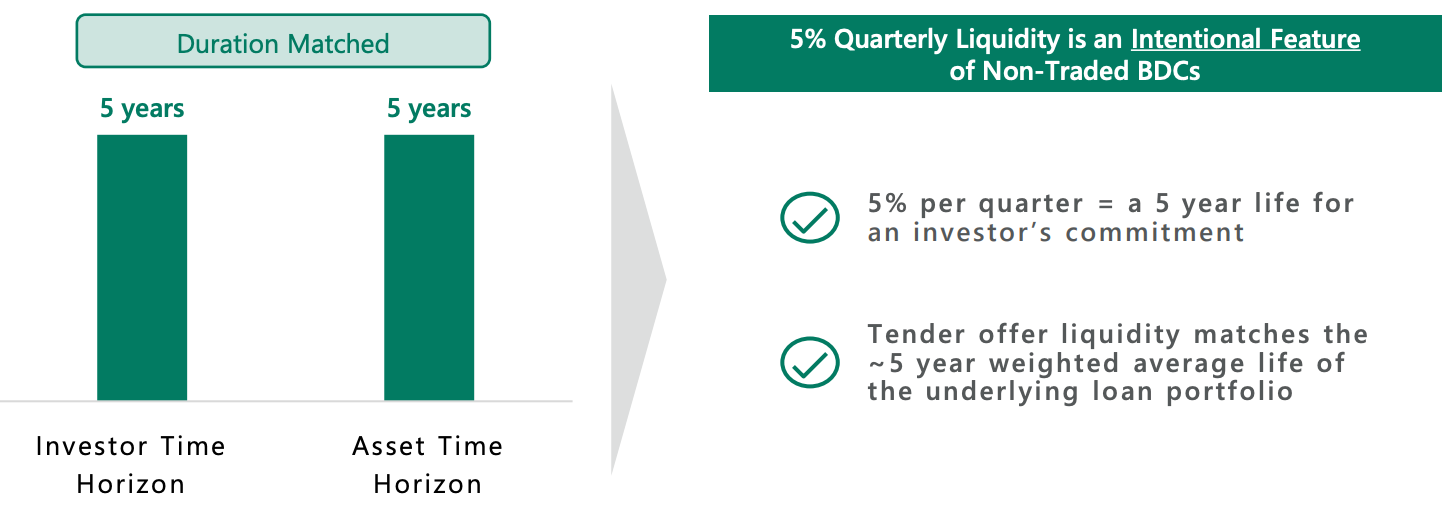

The gates exist for a reason

Before non-traded BDCs existed, investors could either have daily liquidity in a traded BDC or illiquidity in a 10-12 year private commingled fund.

The innovation of non-traded BDCs was to allow investors to own illiquid assets while providing a structured path to liquidity, with the structure self-amortizing so investors could be made whole without forced asset liquidations.

The 5%/20% limits weren’t pulled out of thin air but rather designed to track the weighted average life of the underlying loan portfolio.

Meeting the contractual 5%/20% is exactly what these structures were designed to do.

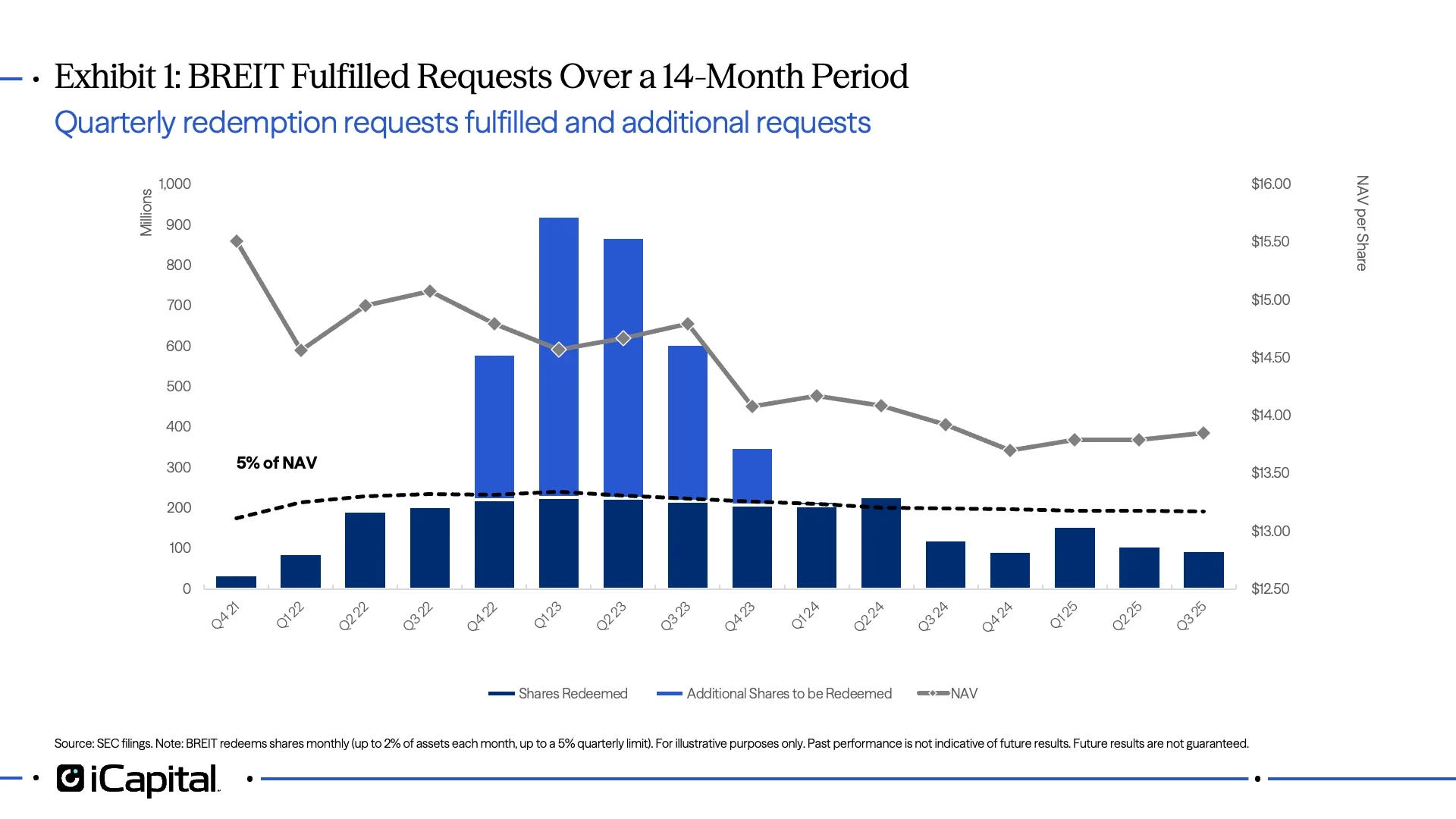

We’ve Seen This Redemption Playbook Before

It’s helpful to look back at history and understand how managers worked through similar instances when they were oversubscribed.

Blackstone’s Real Estate Income Trust (BREIT) is one fund that faced a period of heightened redemption requests where investors asked to withdraw roughly 20% of shares at the peak (Exhibit 1). The fund ultimately fulfilled 100% of requests over a fourteen-month period.

Assuming redemptions spike two to four times their quarterly limit in Q1 2026, iCapital estimates oversubscriptions could continue for a three to five quarter period.

Not all BDCs are equal

“Generalization errors are insidious because they can catch the unwary investor too focused on the big picture and not enough on the details.”

Much of the media hype focuses on BDCs as a whole.

However, as Neuberger highlighted,BDCs Have Shown Wide Performance Dispersion .

Lending money isn’t hard. Getting repaid can be hard. The managers who understood that during the very good times are the ones who will stand out now in this less certain environment.

It’s the boulders NOT the pebbles.

“Contrary to this popular idea that it is small investors leading the charge, it is actually a smaller number of large investors who are double the size, on average, of the typical account in these vehicles… It is the bigger boulders, as opposed to the pebbles, where you get more movement in terms of redemptions”

Focus has been on HNW investors.

In reality, the redemptions are largely driven by a few larger family offices or single institutions (See Vista Credit).

90% of investors are choosing to remain invested.

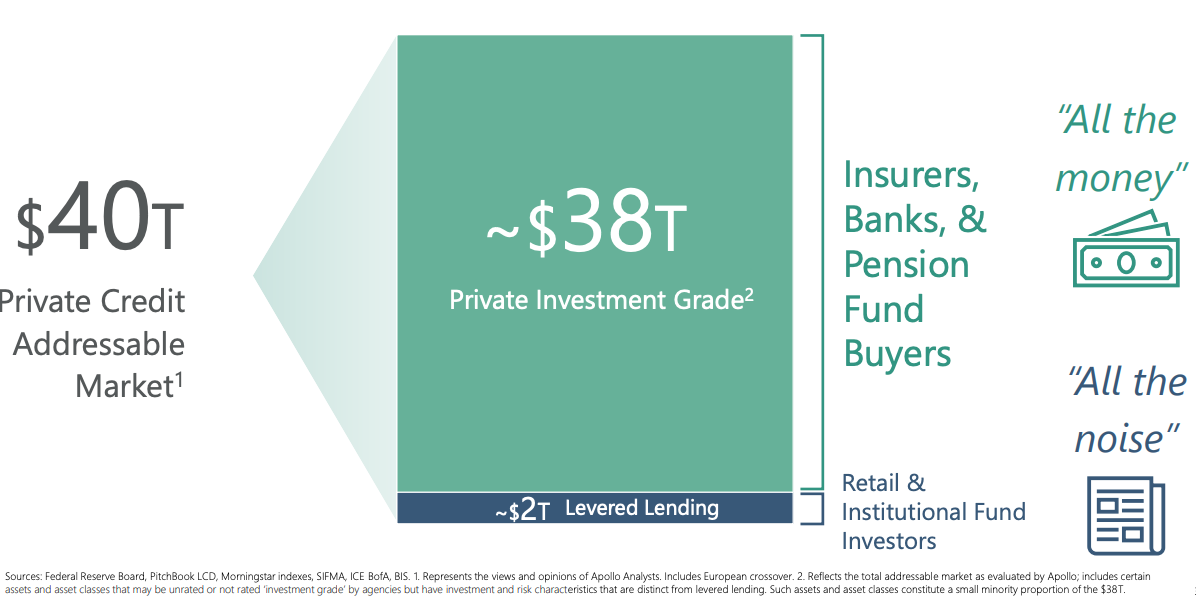

Non-Traded BDCs ≠ All Private Credit

Attention will be focused on the non-traded BDCs.

As Apollo and others have pointed out, the market is much larger than this.

Much of the focus has been on wealth vehicles like BDCs, interval funds, and tender funds. These funds make up around $550 billion in AUM — or about 25% — of the $2.2 trillion private credit industry. Institutional demand is actually accelerating

Morgan Stanley: Private Credit Still an All-Weather Asset Class?

Morgan Stanley released a white paper on US and European Direct Lending. Below are a few graphs which might be helpful in your fundraising decks.

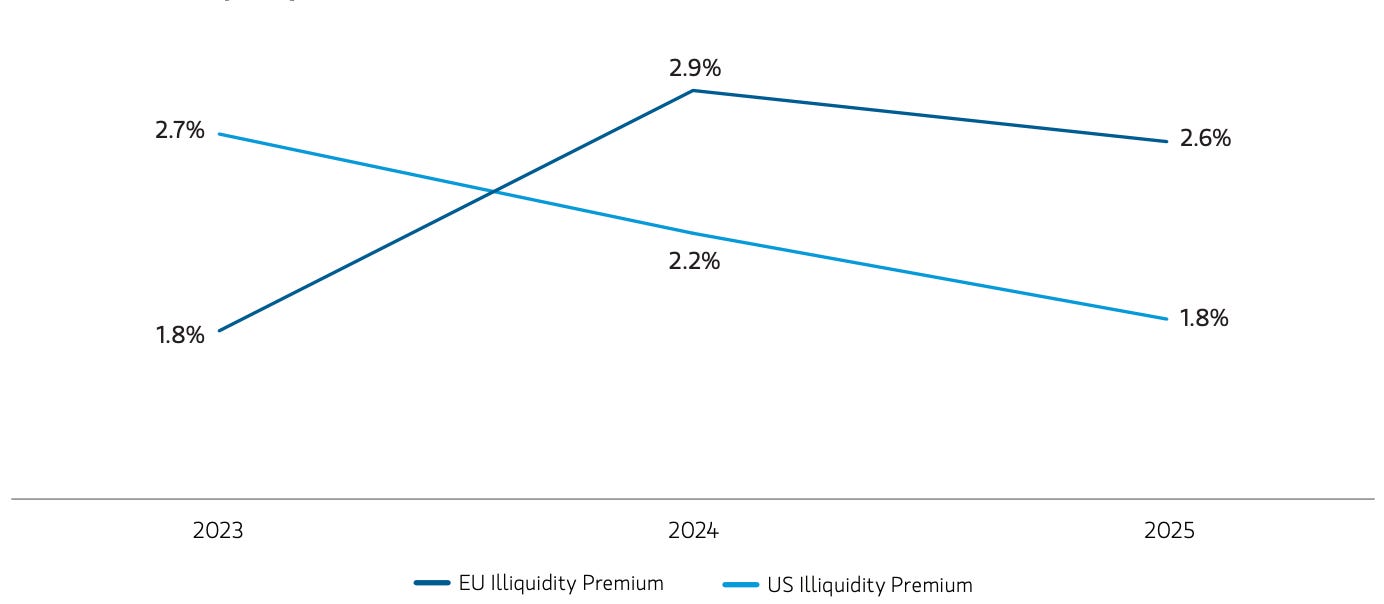

Europe Overtakes the US on Direct Lending Premiums

Over the past three years, European direct lending has delivered an average premium of ~240 bps.

Europe saw an increase in illiquidity premium from ~180 bps in 2023 to ~260 bps in 2025.

In the US, the premium has compressed from ~270 bps in 2023 to ~180 bps in 2025.

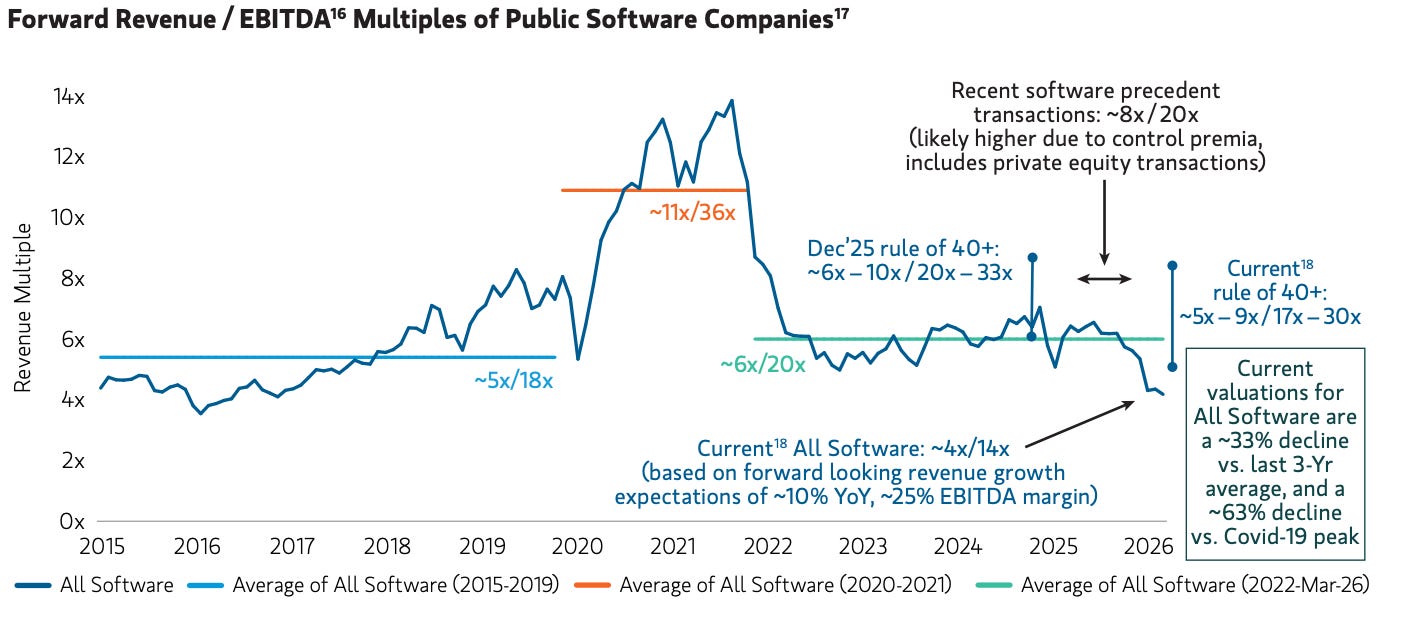

Software Valuations have Normalised

Software accounts for ~20-30% of Direct Lending

Valuation multiples exceeded ~30x EV/EBITDA at their 2021 peak.

They have since normalised significantly.

Listed software companies continue to deliver revenue growth of approximately 10–15% with forward expectations of 10–11% p.a. for the next two years.

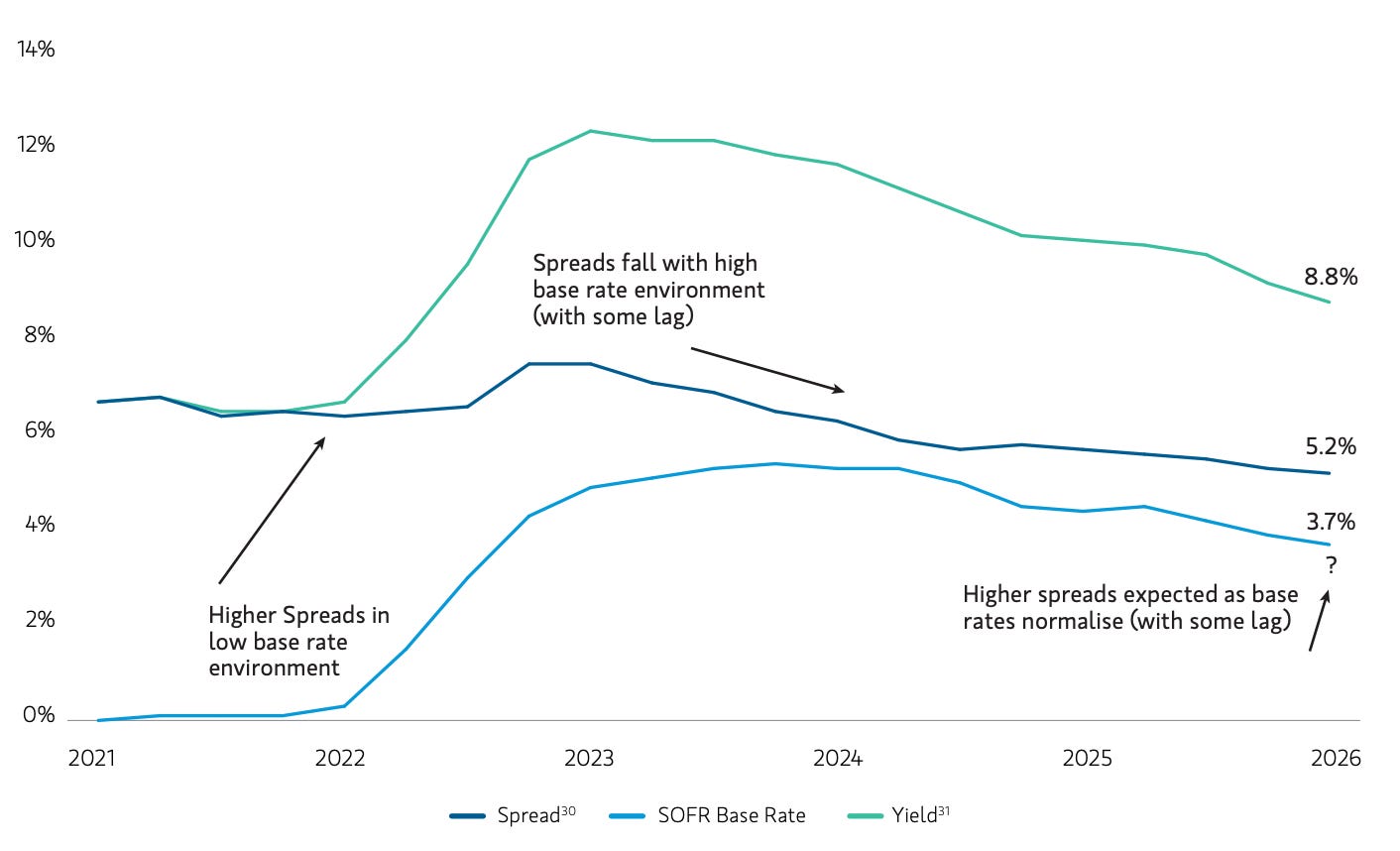

Direct lending benefited from a “golden age” of higher base rates

As policy rates have declined and spreads have compressed from peak levels, headline returns have moderated accordingly.

More recently, wider public credit spreads and the reset in public software valuations may have created an impression that private credit software assets may be susceptible to future markdowns. .

💰Fundraising News

Crescent Capital Group, a Los Angeles-based credit manager, raised $10.8 billion for its fourth U.S. direct lending fund, the largest fund in the firm’s history. The fund invests in sponsored lower middle market companies across the United States, targeting companies with EBITDA ranging from $5 million to $50 million. More here

Eurazeo, a Paris-based asset manager, closed its $4.5 billion Private Debt VII fund. The firm’s flagship direct lending strategy focuses on financing lower mid-market companies across Europe and is already 65 percent deployed across more than 70 portfolio companies, totalling €2.5 billion in investments. More here

HSBC Asset Management closed its $2 billion UK direct lending fund II. The strategy invests alongside HSBC’s bank in senior secured loans to lower- and core-middle-market businesses. It typically lends at 3-4x leverage with robust maintenance covenants and equity cushions of c.70%. More here

PGIM, a Newark-based global asset manager and the investment arm of Prudential Financial, launched the PGIM Global Private Credit Fund SCA, a Luxembourg-domiciled fund targeting wealth investors in the United Kingdom, continental Europe and Asia. The fund invests in senior secured loans to middle market companies across North America, Europe and Australia, focusing on companies with EBITDA of $10 million to $75 million. More here

Didn’t make the cut

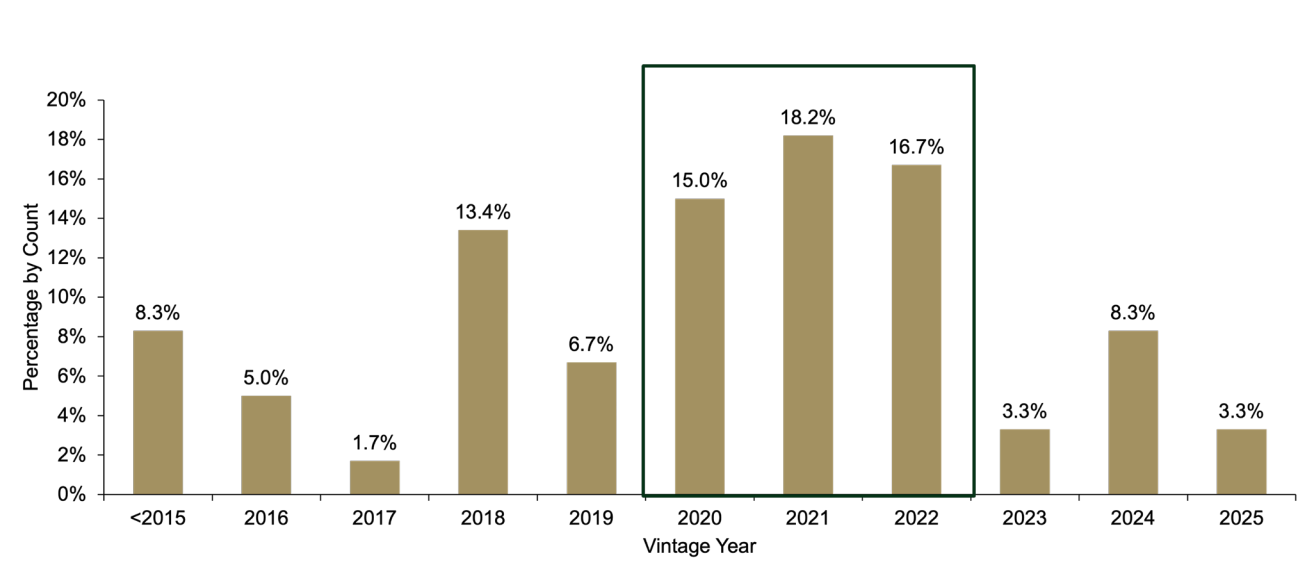

Software Deal Activity Was Elevated in the 2020-2022 Vintage. Link

https://www.connectmoney.com/stories/nav-reits-bdcs-have-returned-over-82b-to-investors-since-22/

This newsletter is for educational and entertainment purposes only. It should not be taken as investment advice.