Brookfield: Seeking Resilience in Turbulent Times

Fundraisings from Hayfin, Ares, Orbit Capital, TLG and More

👋 Hey, Nick here. A big welcome to the new subscribers from Ninety One, Pathway Capital, and Black Diamond. You’re now part of a select group of 3,141 subscribers, reading the 174th edition of my private credit newsletter.

If you’re reading this on Outlook, most of the graphs won’t show. I’d recommend you read it online

📕 Reads of the Week

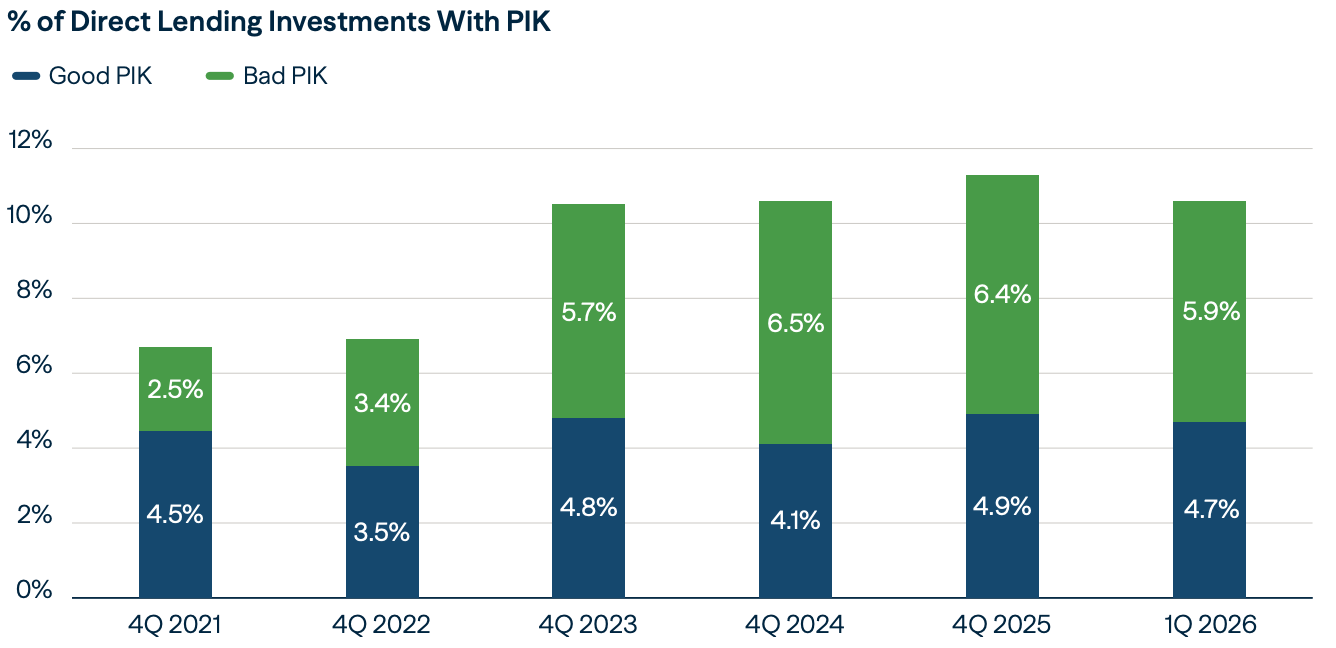

"There really is no good PIK, there’s bad PIK and worse PIK.

If you’re initiating PIK at the onset of a loan, it means that the company can’t pay you your interest in cash.”

Market Updates

Accredited Investor Insights: Blue Owl vs Oaktree - A Tale of Two Redemption Queues. Read here

Sovereign funds move from public markets to private credit. Read the FT article

Rithm Capital: Banks did not exit corporate lending. They repositioned inside it. Link

Churchill: Mid-market fundamentals are sound. Focus on the fundamentals. Link

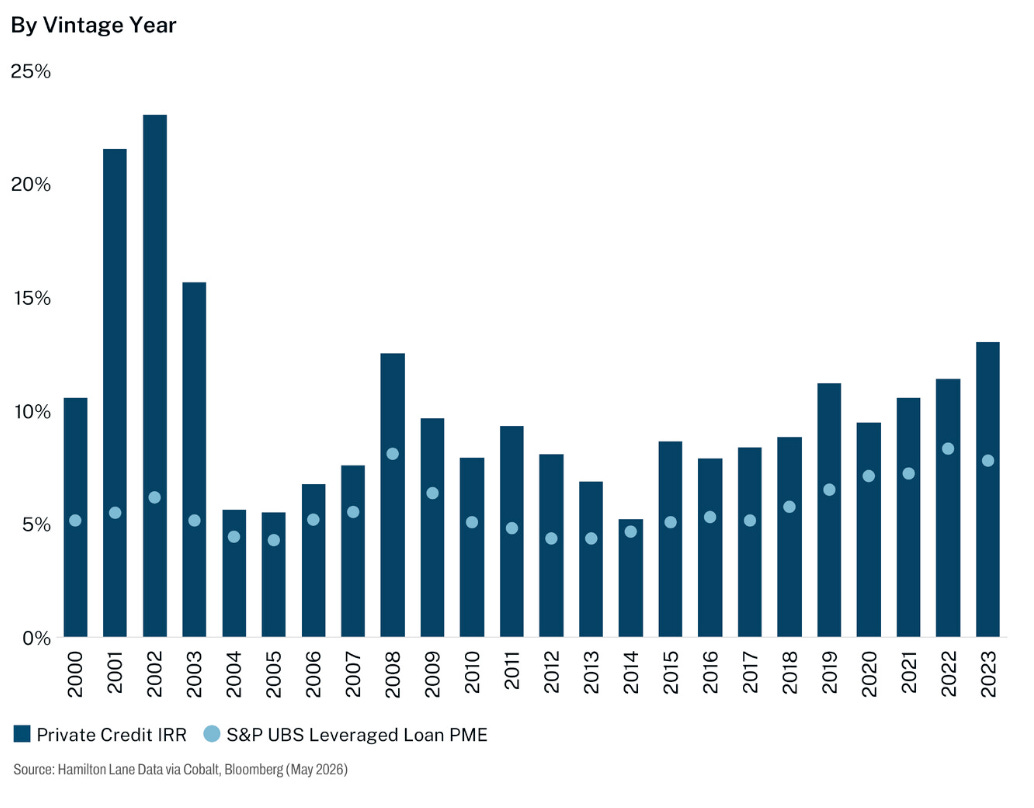

Hamilton Lane: Private credit has consistently outperformed public credit

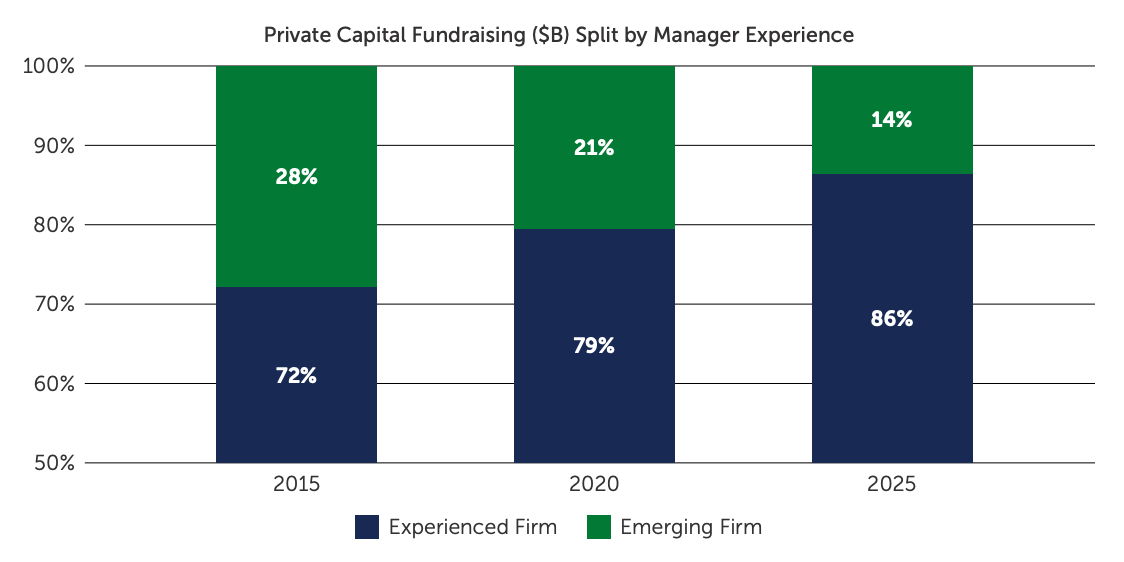

Direct lending capital is becoming more concentrated and increasingly centered among a smaller group of large, established platforms.

Manager Updates

Why Apollo Created Their Onchain Credit Fund. Link

Apollo: Increasing Transparency and Tradability in Private Credit. Read here

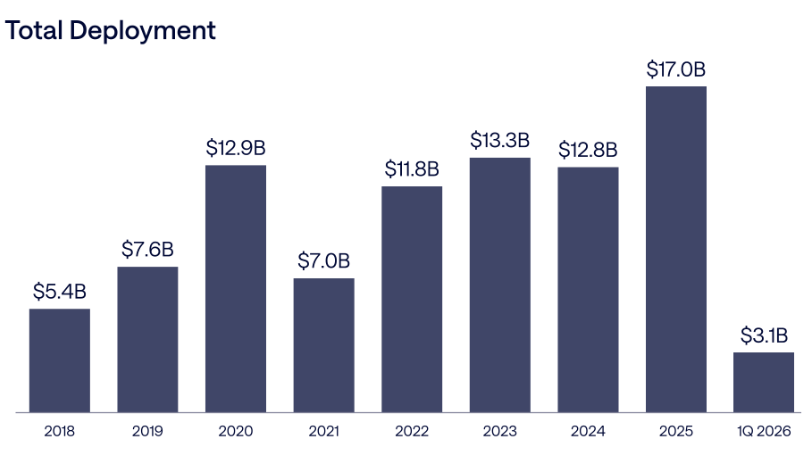

Ares Alt Credit has over $57 Billion in AUM, with over $85 Billion deployed since inception and $12.7 Billion invested over the last twelve months alone.

“The level and the universality of worry about software is probably excessive…

Things will not be as bad as people believe at this time.

Certainly, some will have problems on a case-by-case basis, but you have to lose a lot of value and a lot of revenues before companies actually have problems paying their debts.”

Partnership Updates

Coller Capital and Cherry Bank announced a distribution partnership to provide Italian wealth investors access to private credit secondaries. Link

BDC Updates

“Show me the incentive, and I will show you the outcome.” The FT’s deep-dive into Thoma Bravo’s Medallia acquisition. Link

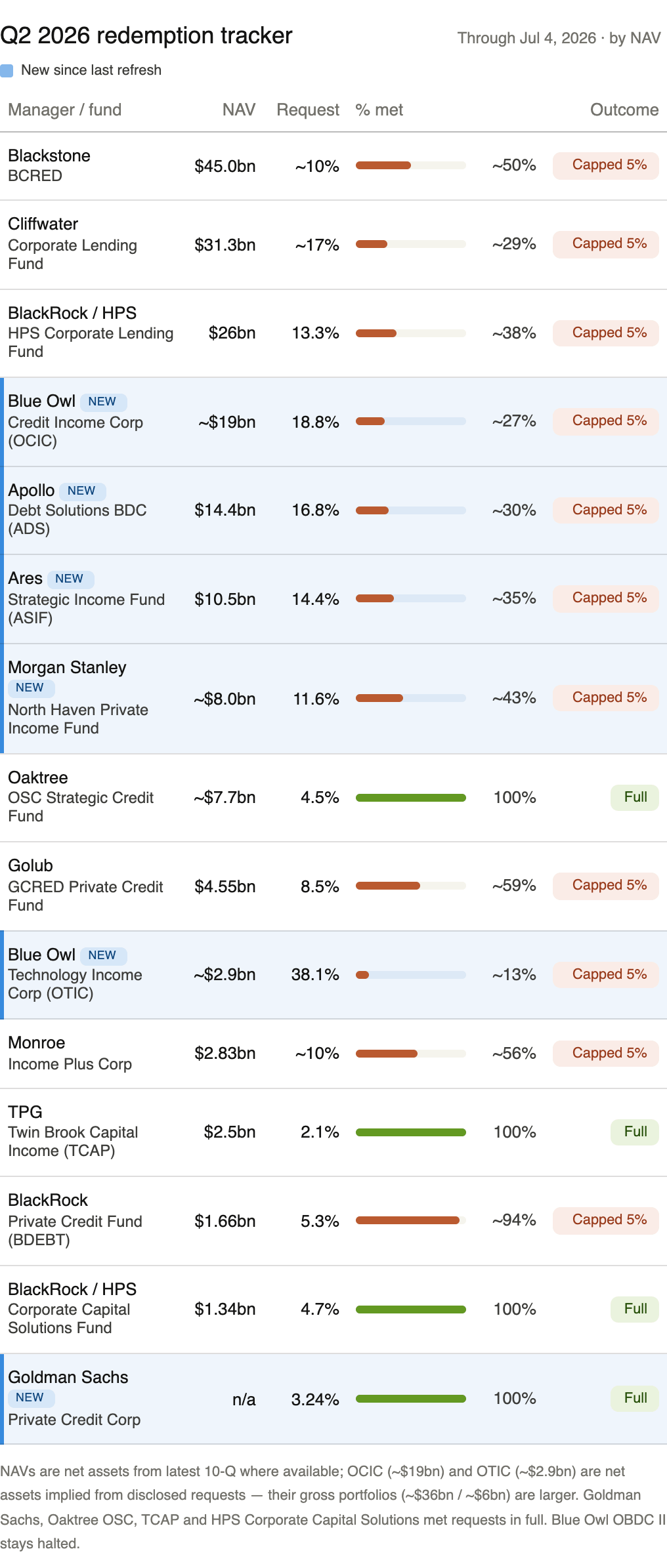

BDC’s Q2 Redemption Wrap Up

Q2 is largely behind us, and most of the largest non-traded BDCs have reported their redemption requests received. Below is a summary of the insights from the quarter.

The headline

Investors asked to withdraw ~$24bn across the 15 funds we track (See below)

Sponsors paid ~$8bn

Aggregate requests rose sharply. Q1 2026 saw roughly $13.9bn requested across the NAV-BDC landscape, with about $7.4bn honored.

Requests were worst at the biggest funds

Median requests were ~10% of NAV, but the asset-weighted average was 13.5%; pressure is concentrated in the largest vehicles.

Cliffwater (17%), Blue Owl OCIC (18.8%), Apollo ADS (16.8%), and HPS HLEND (13.3%) received worse than average requests.

All managers capped redemptions

Unlike Q1, all managers capped the redemption payouts 5%, calling it “operating as designed.”

The most-stressed funds eased

Blue Owl OCIC (21.9%→18.8%),

OTIC (40.7%→38.1%),

Oaktree OSC (8.5%→4.5%)

Brookfield: Seeking Resilience in Turbulent Times

Brookfield published its quarterly outlook to explain how investors can navigate private credit during this market volatility. Below are the key takeaways.

👉 Read Brookfield’s Full Report Here

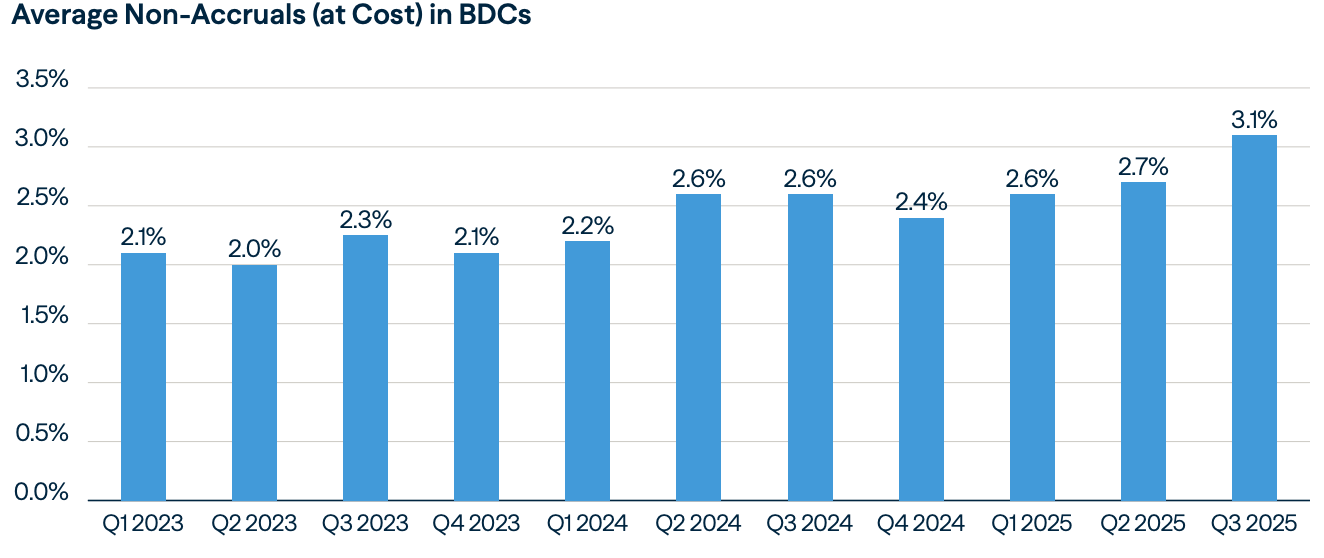

Non-Accruals in BDCs Remain Low

Private credit sentiment has shifted from enthusiasm to caution.

The current market is a consequence of company-specific issues and underwriting standards, not a fundamental break in the system.

This explains why the dispersion of returns is increasing across lenders, sectors, and vintages.

While PIK Usage Is a Concern, Levels Are Stabilizing, and Non-Accrual Rates Remain Low

While PIK activity, particularly PIK introduced through amendments, can be a sign of credit deterioration, usage has stabilized recently as borrowers’ ability to pay cash interest is improving.

Market stress has been more pronounced among smaller and middle-market borrowers, particularly companies in the $25–50 million EBITDA range, while larger issuers have generally remained more stable.

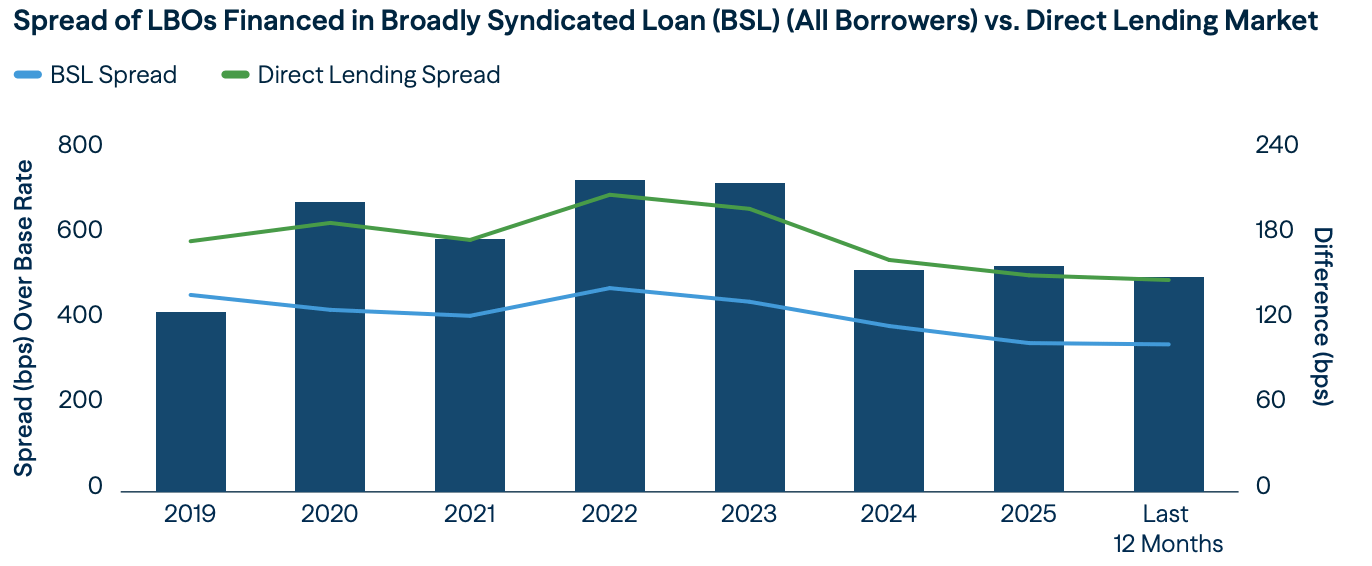

Direct Lending Spreads Remain Attractive

One of the inevitable consequences of a market dislocation is that it creates opportunities in distressed assets, and this is no exception.

This is particularly evident in sector-specific areas that have borne the brunt of negative sentiment, but is also a result of refinancing pressure.

More than $1.3 trillion in loans are maturing in 2026; public markets are likely to absorb much of this volume, but may be less receptive to more complex credit situations, creating opportunities for private lenders

There are four key themes driving the private credit outlook over the next few months

Dispersion is key. There will be increased dispersion among private credit manager returns. To put it simply, this is a credit pickers’ market.

Yields remain attractive. The private credit premium—in other words, the return relative to public credit investments—has compressed in recent months, but it has not disappeared. Yields remain compelling relative to public markets.

Selection-driven returns. Performance will increasingly depend on a strong focus on borrower quality, underwriting discipline, and the structuring and sourcing of loans. Direct lending is and remains a core allocation of investors’ fixed-income portfolios, but sustained performance will come from lenders that emphasize selectivity and disciplined underwriting, with a focus on risk mitigation.

Opportunities are emerging. One of the inevitable consequences of a market dislocation is that it creates opportunities in distressed assets, and this is no exception. This is particularly evident in sector-specific areas that have borne the brunt of negative sentiment, but is also a result of refinancing pressure. More than $1.3 trillion in loans are maturing in 2026; public markets are likely to absorb much of this volume, but may be less receptive to more complex credit situations, creating opportunities for private lender.

👉 Read Brookfield’s Full Report Here

💰Fundraising News

I’m really excited for the next two years to invest, especially where we are in the lower middle market

Hayfin, a UK-based manager, closed its $17.2 billion Direct Lending Fund V. The fund lends senior‑secured loans to European middle‑market and upper‑middle‑market businesses. Since it was founded in 2009, Hayfin has invested over €55bn of capital across more than 500 portfolio companies via its private credit strategies. More here

Ares is raising its second Asia private credit fund focused on financing leveraged buyouts across the Asia Pacific. The fund, Asia Direct Lending II, could reportedly be larger than its predecessor, which raised $1.7bn, although final details have not yet been set. More here

RGreen Invest, a Paris-based manager, closed its $572 million Infrabridge IV fund, more than doubling the size of its previous vintage. The infrastructure debt fund provides short-term senior debt/bridge financing to energy-transition infrastructure projects in Europe, focusing on the lower-mid market. Its portfolio spans a broad range of sectors, including geothermal energy, biomethane, energy storage, hybrid solar and wind projects incorporating battery storage. More here

Incus Capital, the Madrid-based real assets private credit specialist, announced a second close of $640 million for its European Credit Fund V. The fund provides asset-backed financing to mid-market businesses across Europe. Investments completed to date include financing for prime residential development projects, logistics assets, the hospitality industry, energy transition infrastructure, and residential repositioning opportunities. The fund typically lends between €25 million and €60 million per company. More here

Eiffel Investment, a Paris-based manager, announced the first closing of $570 million for its Impact Debt III. The fund provides financing to European mid-sized companies, where the capital is used to support one of three impact objectives: reducing temperature impact, preserving ecosystems, or promoting diversity. It will invest in 40 to 50 European companies. More here

Orbit Capital, a Czech Republic-based manager, announced a second close of $122 million for its second Growth Debt Fund II. Orbit Capital is a growth-stage investor managing over €200 million in AUM through venture debt and growth equity vehicles. The firm has a primary focus on technology leaders in CEE, while remaining actively engaged in opportunities across the DACH region and broader European markets. Tickets range from €3 million to €15 million. More here

TLG Capital, a London-based emerging markets manager, announced the $120 million second close of its Africa Growth Impact Fund II. The fund finances African SMEs through local banking partners, with each loan structured for a longer tenor than African banks typically provide and backed by a guarantee from the originating bank. Since its $75 million first close in April 2025, the fund has invested in nine SMEs across seven countries and seven sectors, with debt facilities ranging from $5 million to $15 million. More here

This newsletter is for educational and entertainment purposes only. It should not be taken as investment advice.