Credit Secondaries: Solving Private Credit’s DPI Problem

Fundraisings from Ares, Hunter Point, Man Group and KKR

👋 Hey, Nick here. A big welcome to the new subscribers from Eurazeo, Golub, and Prudential. You’re now part of a select group of 3,085 subscribers, reading the 171st edition of my private credit newsletter.

If you’re reading this on Outlook, most of the graphs won’t show. I’d recommend you read it online

📕 Reads of the Week

Top 3 Market Updates

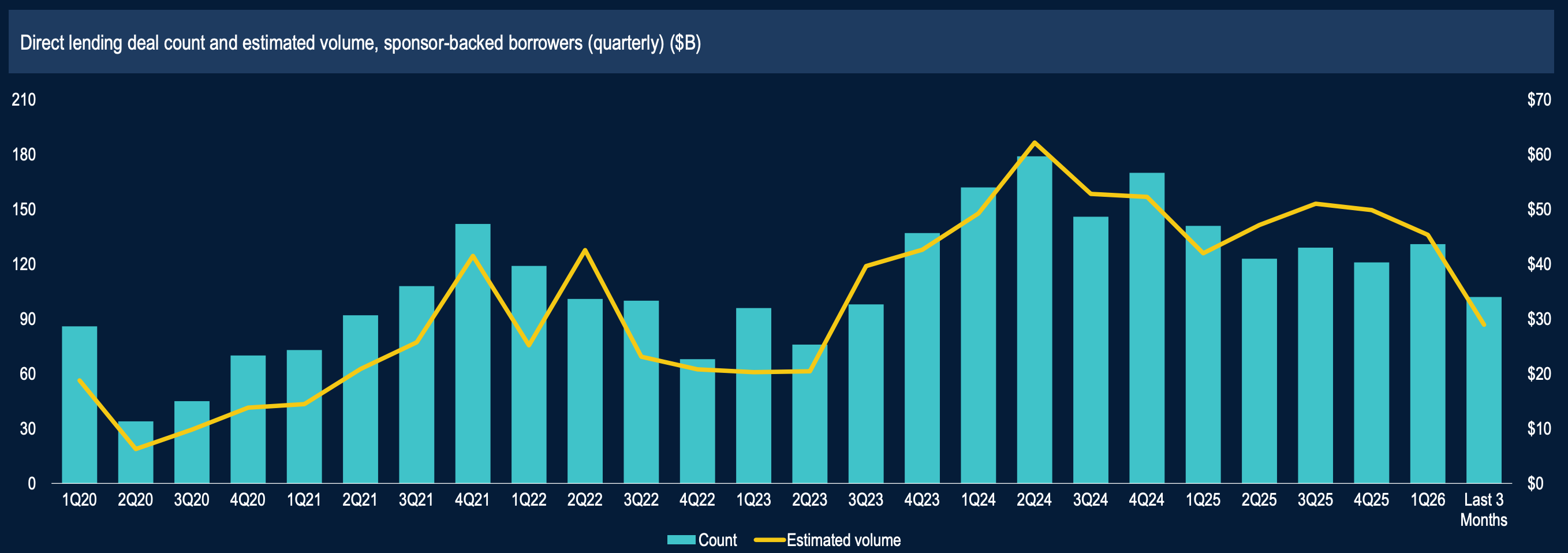

US Direct lending volume fell to a three-year low. Pitchbook

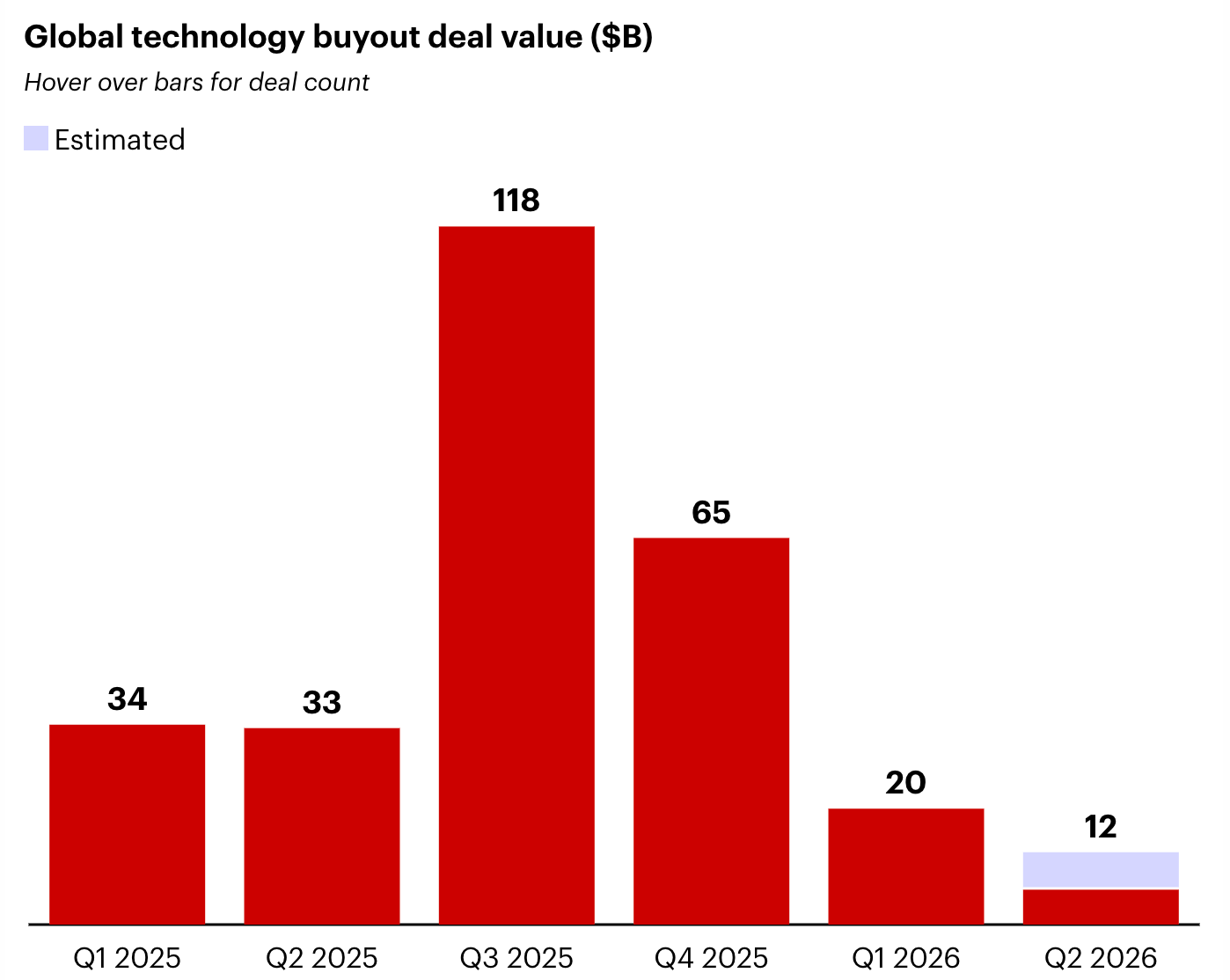

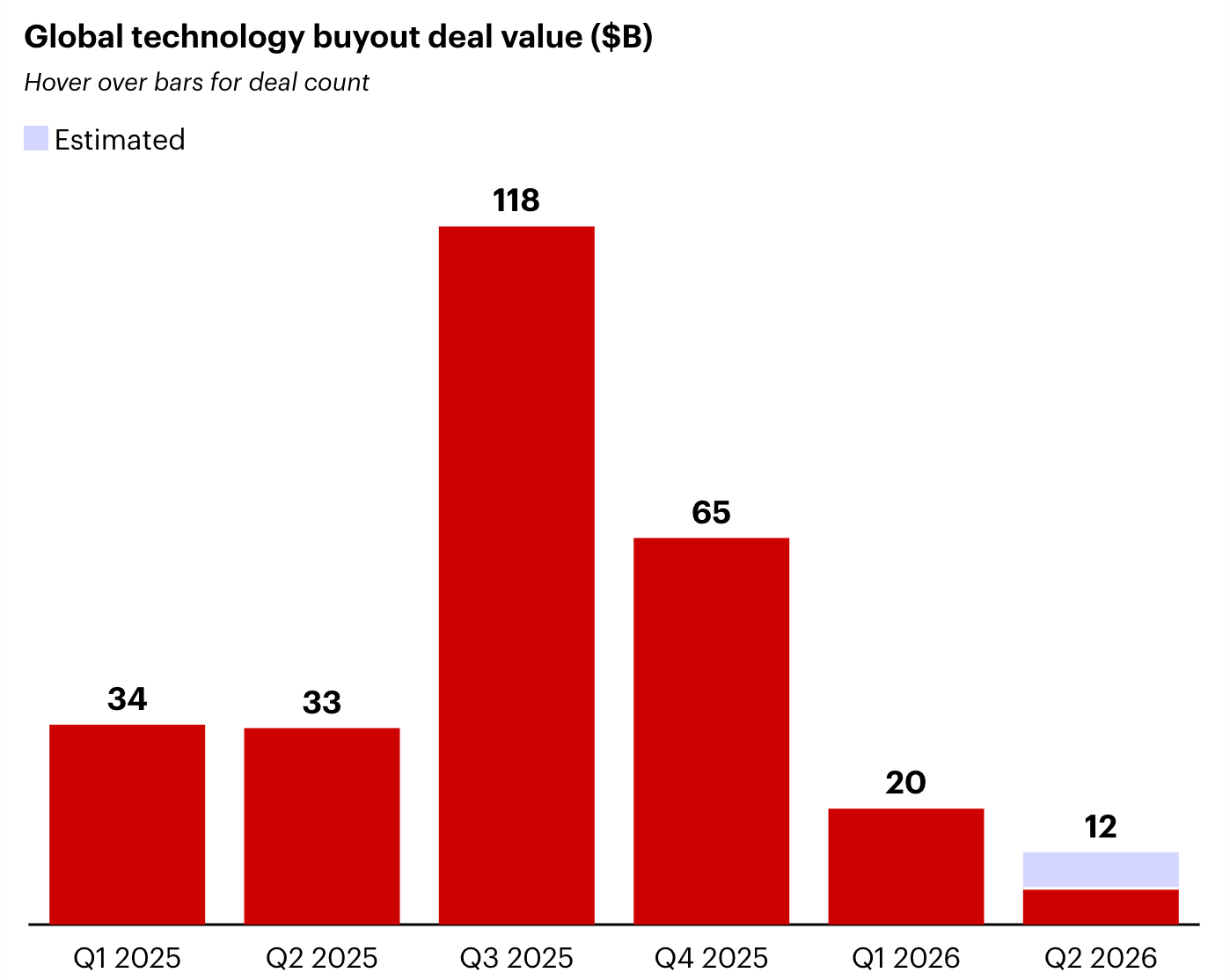

Global Technology buyout deal value has also fallen sharply. Bain & Company

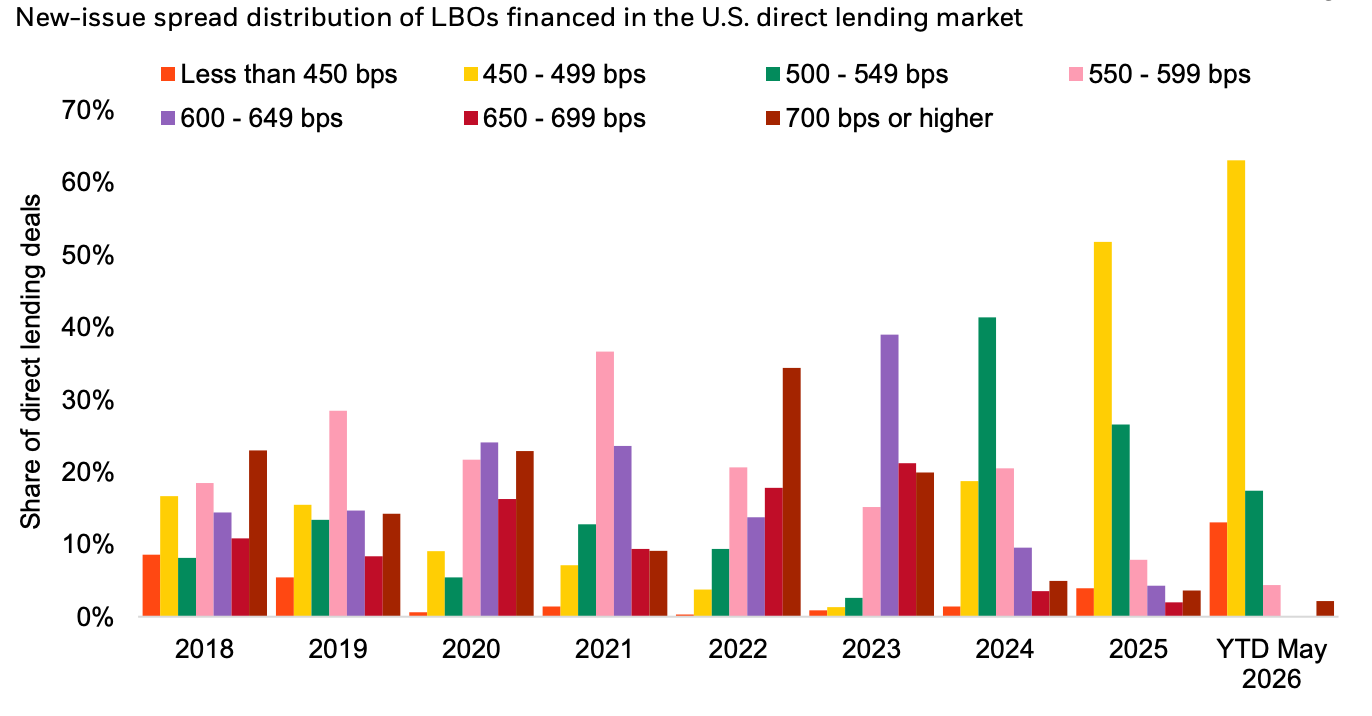

Despite this, deals priced between 450-499bps represent more than half of YTD activity. Blackrock

“A lot of companies restructured through liability management exercises where they kicked the can down the road and did out-of-court type of deals to give them more runway…

Eventually, this will come home to roost…

From a distressed investor’s point of view, if it stays higher for longer, there’s an opportunity to purchase meaningful amounts of distressed debt and/or provide capital solutions that allow companies to de-lever through equity infusions.”

Manager Updates

Ares raised $12.7 billion for its Pathfinder Fund III, the largest global asset-based finance fund in the market. Ares Alternative Credit now manages ~$57.3 billion, including $33.1 billion dedicated to non-investment grade assets. More here

The Pathfinder family of funds has pledged to donate at least 5-10% of the carried interest to global health and education charitable organisations. Based on performance to date, the Pathfinder funds have already accrued approximately $56.9 million in pledged charitable contributions. Read more about Promote Giving here

Apollo and Blackstone announced a $35 bilion package to finance Broadcom’s new AI XPV Platform. The financing will enable over 20GW in compute capacity for leading frontier AI labs through 2028. The initial transaction will facilitate Anthropic’s previously announced capacity expansion of more than 1GW of compute infrastructure for training and inference starting in mid-2026. Link

Partnership Updates

Janus Henderson is acquiring Rantum Capital, a Frankfurt‑based private markets investment manager. Founded in 2013, Rantum Capital focuses on providing private debt and private equity financing solutions to family and entrepreneur‑owned small and mid‑sized companies in Germany, Austria and Switzerland. The firm has raised around €1.2 billion of capital across its private credit and private equity strategies. Link

This acquisition builds on Janus Henderson’s recent expansion in private markets, they also acquired NBK Capital in the Middle East and Victory Park in the US in 2024.

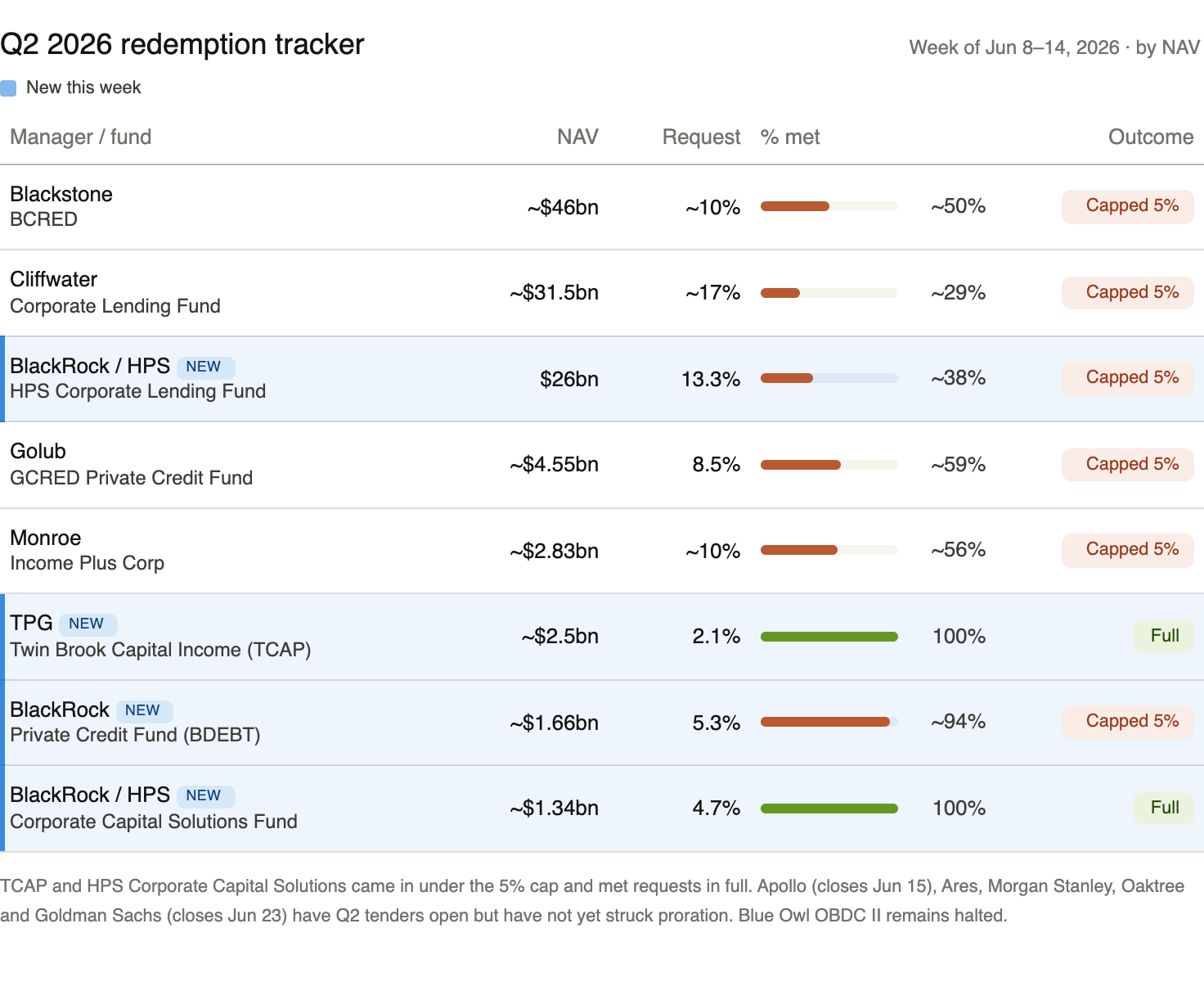

BDC’s Q2 Redemptions: Week 2

4 BDC’s announced redemption requests last week: HLEND, TPG, BDEBT, and HPS Corporate Capital Solutions.

HPS’s $26 billion HLEND generated much of the attention, and as expected, capped its 13.3% of redemption requests at 5%.

Below is a summary of Q2 so far.

Credit Secondaries: Solving Private Credit’s DPI Problem

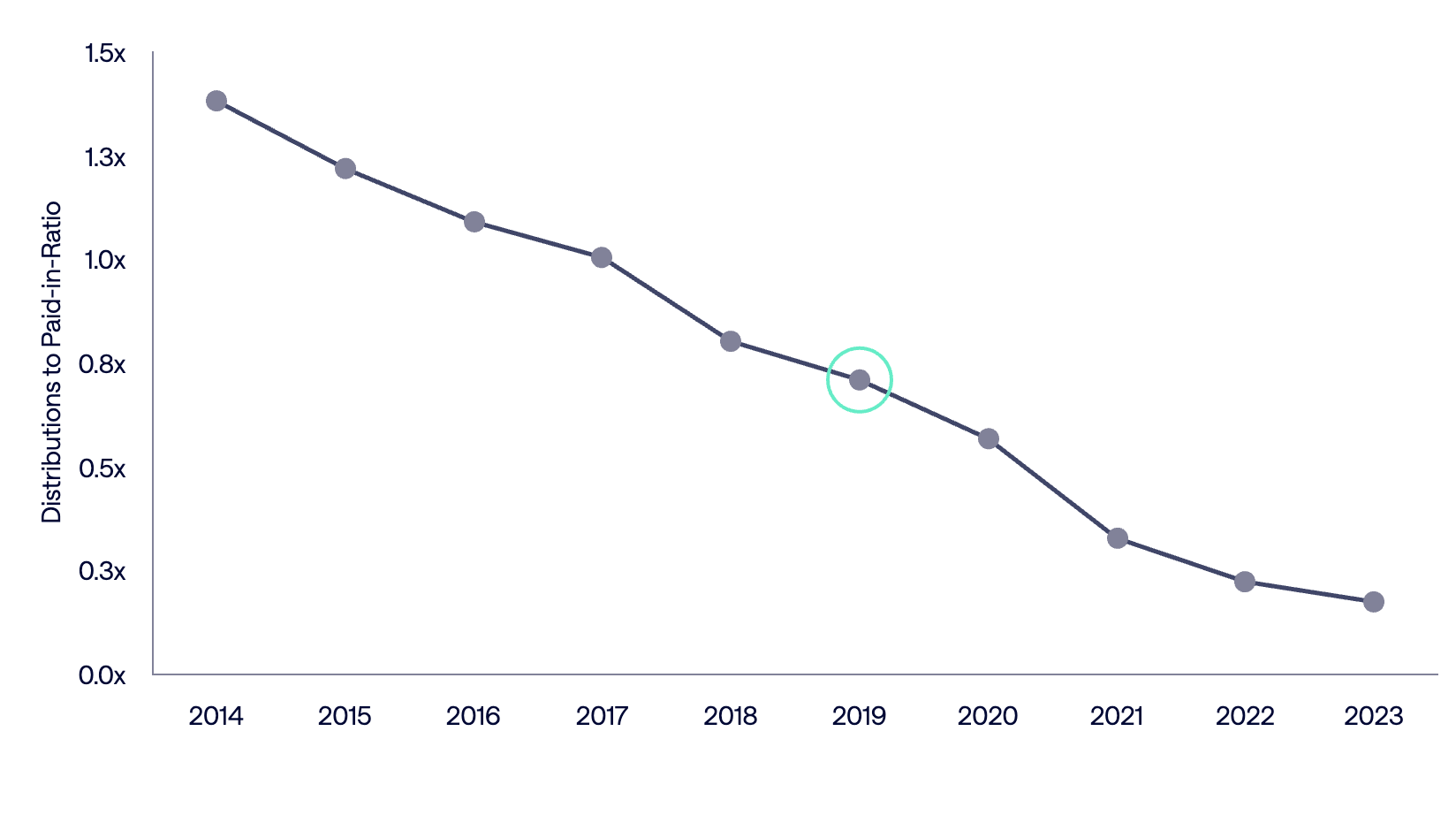

The 2019 Vintage Is Running Out of Road

Ares believes that 2019 vintage private credit funds have an average DPI multiple of ~0.7x.

These funds only have a few years to convert a meaningful share of NAV into distributions.

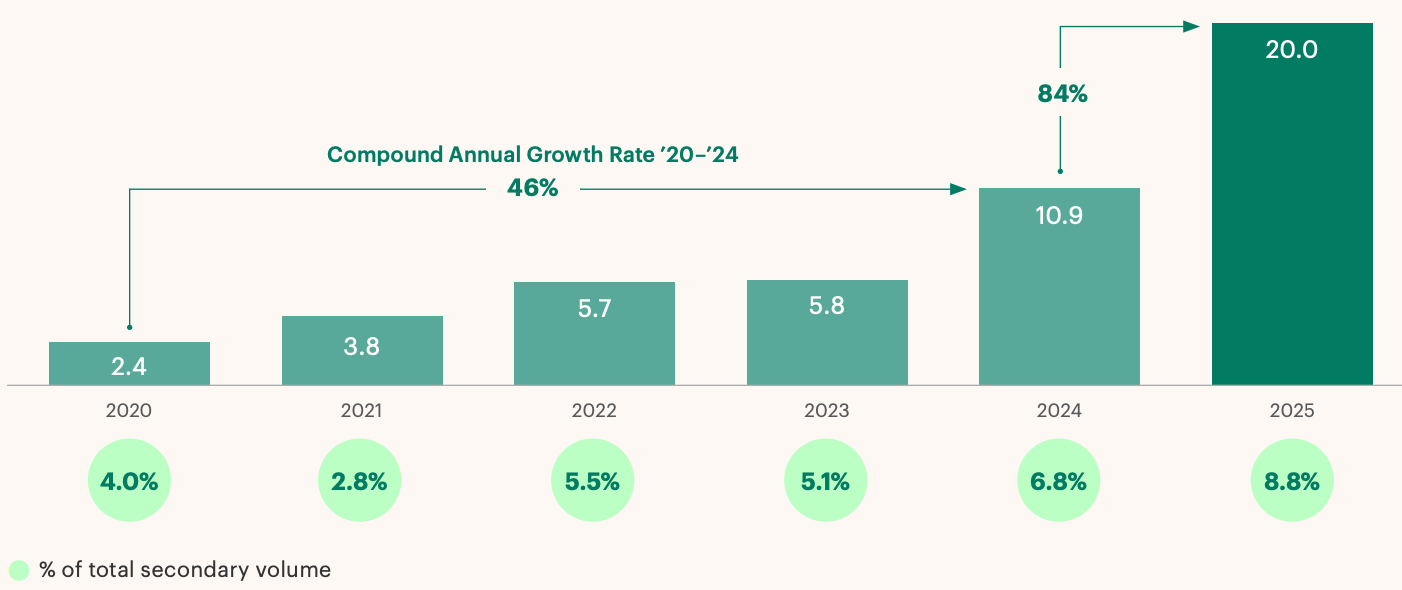

Credit secondaries are one of the fastest-growing segments of private markets.

Beginning in the early 2020s, and accelerating meaningfully through 2022 and 2023. Apollo

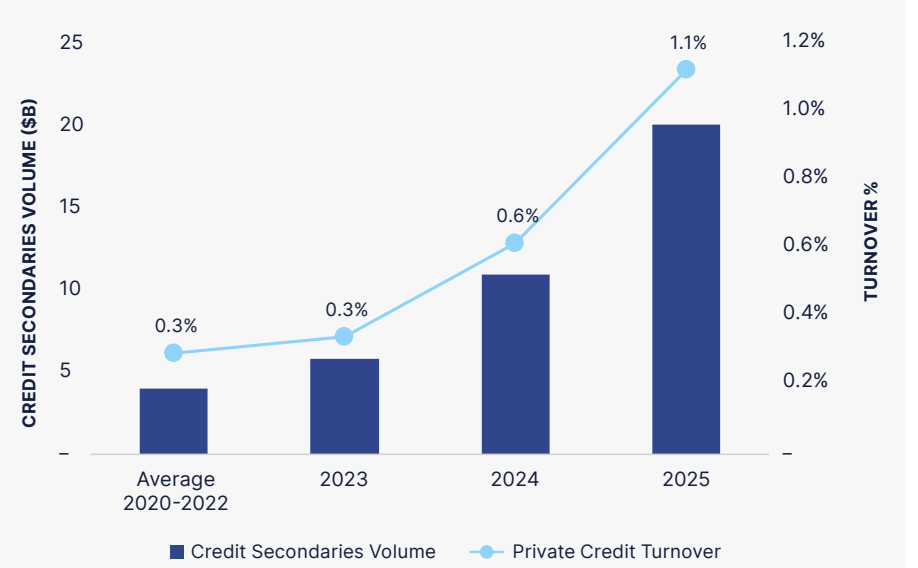

Despite this growth, credit secondaries remain a fraction of the overall direct lending market.

Carlyle estimates that only $20 billion of credit fund exposures traded in 2025.

This impliying a fund turnover rate (Secondaries Market / Direct Lending Market) of ~1%.

This is well below the 2–3% observed in private equity secondaries. Carlyle

This gap highlights the headroom for growth

Apollo expects the private credit secondaries market to scale from $20 billion in 2025 to $50 billion within two to three years.

Carlyle believes the credit secondaries market will grow to $80+ billion by 2030, comprised of ~$55 billion in GP- centered volume, which is experiencing the most significant growth, and ~$25 billion in LP-centered volume.

GP solutions are experiencing the most growth

Unlike private equity continuation vehicles, where one or a small number of assets are typically selected, credit continuation vehicles are generally structured as full-fund solutions, with diversification as a core feature.

Alignment is typically stronger than in LP interest transactions since the new vehicle is supported by GP carry rollover, additional GP capital commitments, and refreshed governance frameworks, such as enhanced reporting, Limited Partner Advisory Committee (“LPAC”) rights, tighter structural safeguards, and tailored downside mitigation features.

For buyers, continuation vehicles offer the opportunity to deploy capital into seasoned portfolios with known performance characteristics. Buyers can benefit from full access to GP deal teams and detailed asset-level information, including underwriting memoranda, financial models, portfolio reviews, and valuation materials.

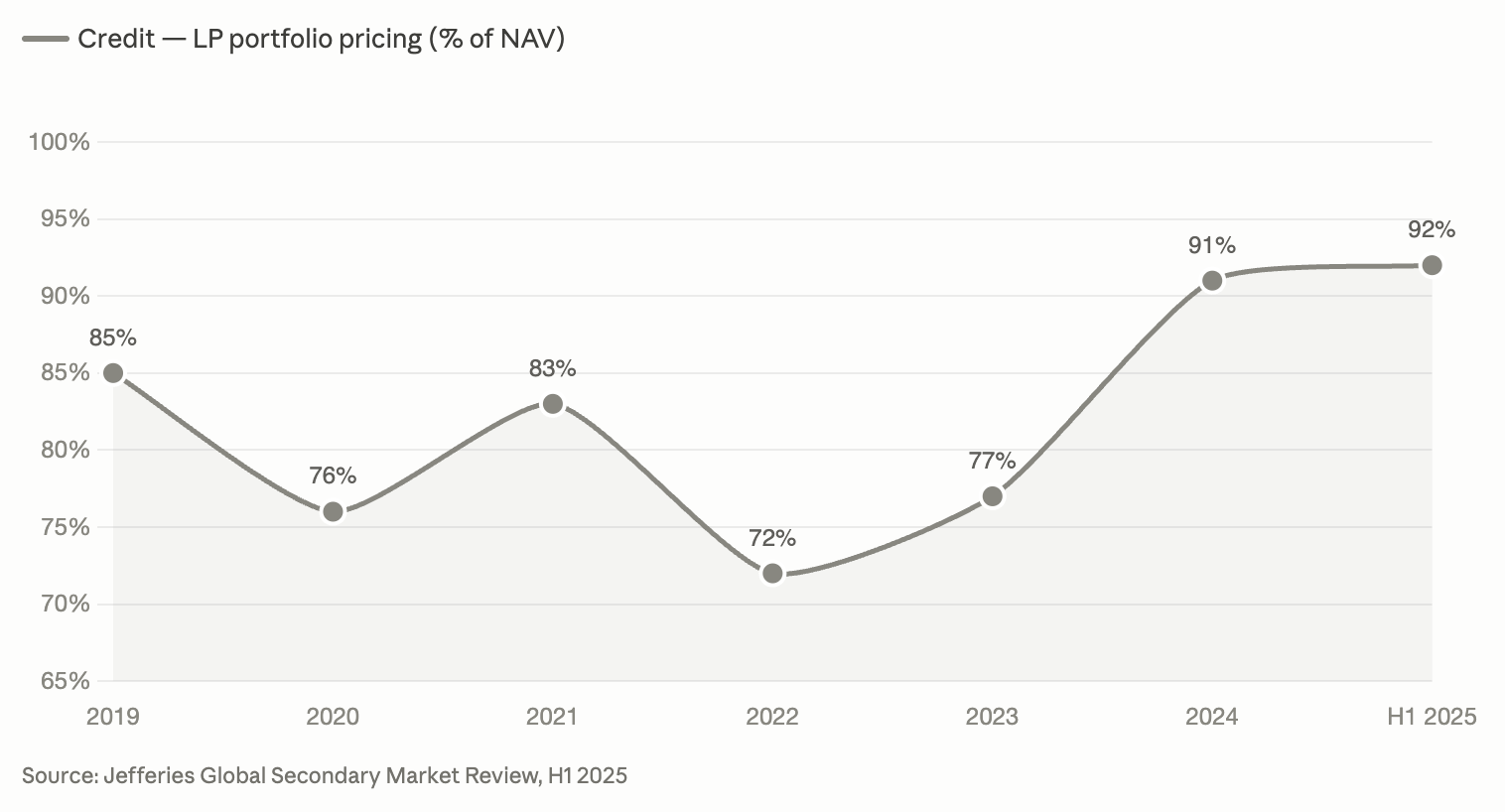

Pricing is one of the most easily misconstrued elements of the market

Credit secondaries priced at 92% of NAV on average in H1 2025, up from 91% at the end of 2024.

Strong pricing was fueled by significant fundraising dedicated to private credit and strong demand for senior direct lending interests. Jefferies

Beware of Discrete Discounts

Credit secondaries sources that have participated in or worked on the half-dozen mega-continuation vehicles in the market gave LCD generalized but realistic figures to illustrate how these processes usually work.

For example, a deal that prices nominally above par — for example, 102 — may get three points of discount from the portfolio’s NAV (which may be marked at 97) and another four points from the two quarters of post-reference date cash flows that have accrued to the buyers’ benefit. This brings the indirect discount to a total of seven points, and an effective price of 95, on a deal that may have a headline price of 102.

This is why no deals have traded at a “true premium” to par, a number of sources said. One banker estimated that the highest effective price seen in the market so far has been par, at most. Pitchbook

👉 Read More: Carlyle, Apollo, Coller Capital, Ares, Jefferies, Pitchbook

💰Fundraising News

Ares raised $12.7 billion for its Pathfinder Fund III, the largest global asset-based finance fund in the market. Ares Alternative Credit now manages ~$57.3 billion, including $33.1 billion dedicated to non-investment grade assets. More here

The Pathfinder family of funds have pledged to donate at least 5-10% of the carried interest profits from to global health and education charitable organisations. Based on performance to date, the Pathfinder funds have already accrued approximately $56.9 million in pledged charitable contributions. Read more about Promote Giving here

Hunter Point Capital, a New York-based manager, closed its inaugural vintages of its NAV Lending and Preferred Solutions strategies, with total commitments of $4.3 billion. The GP Financing Solutions platform offers NAV-based loans and preferred financing solutions to investment managers. To date, it has completed 13 transactions. More here

Man Group, a UK-based manager, announced a first close of its Man Opportunistic Credit Fund III. The fund is targeting a final close of $1.25 billion. The strategy focuses primarily on mid-market, off-the-run and other less competitive opportunities, combining steady-return asset pools with direct-to-company financings and bespoke transactions. More here

KKR has had a first close of $1 billion for its Opportunistic Real Estate Credit Fund III. The fund will invest opportunistically in real estate in the US and Western Europe. The fund will focus on experienced sponsor and will also invest in mezzanine loans, preferred equity and single-asset, single-borrower deals. More here

This newsletter is for educational and entertainment purposes only. It should not be taken as investment advice.

I don't actually get the calculation for secondaries. How does buying at 102 give me a discount of 3 points against an NAV of 97?

"For example, a deal that prices nominally above par — for example, 102 — may get three points of discount from the portfolio’s NAV (which may be marked at 97) and another four points from the two quarters of post-reference date cash flows that have accrued to the buyers’ benefit. This brings the indirect discount to a total of seven points, and an effective price of 95, on a deal that may have a headline price of 102."