Diameter: WTF Is Going On In Private Credit?

Fundraisings from Barings, Antares, PGIM and more....

👋 Hey, Nick here. A big welcome to the new subscribers from Lord Abbett, Chicago Atlantic, and Rithm. You’re now part of a select group of 3,011 subscribers. This is the 168th edition of my private credit newsletter.

If you’re reading this on Outlook, most of the graphs won’t show. I’d recommend you read it online

📕 Reads of the Week

Concentrating capital in narrow strategies, over-allocating to a single manager, or assuming that one source of yield will perform well in all environments has always been risky.

When those bets go wrong, the asset class becomes the scapegoat.

AI and Data Centers

Pimco: AI Credit Expansion: Assessing the Micro and Macro Risks (**Recommended Read**).

Blackstone is partnering with Google to create a new U.S.-based company that will offer efficient data center capacity, operations, networking, and a compute-as-a-service. Blackstone will initially commit $5 billion to ensure the first 500 MW of capacity goes online in 2027. More here

Market Updates

Private credit spreads in the spotlight.

Spreads in the US have widened by 50-100 bps since the start of the year, placing typical deal pricing around 525 bps.

The European market has barely moved. The average European direct lending spread for the last 12 months is 509 bps, 13 bps lower the full-year 2025 reading.

Pitchbook’s Global Private Market Fundraising Report. Link

Bank lending to UK businesses fell to the lowest level in nearly 30 years.

Total lending to private businesses returned to levels last seen in 1998

SME loans have almost halved as a % of GDP since 2011.

See the FT Article here and BCG Research here

KKR: 2021 and 2022 Vintages Reflect Weaker Underwriting; Other Vintages Are Better Positioned. Link

KKR: Beyond the Roar

The extension of credit is one of the oldest practices in civilization. The infrastructure has changed, the instruments have multiplied, and the participants have diversified, but the core function has endured: connecting capital with opportunity, and pricing risk along the way.

Every chapter of that evolution, from the acceptance of noninvestment grade debt in the 70s, to the popularization of LBOs in the 80s, to the expansion of direct lending in the 2010s, has followed a familiar arc:

Innovation opens the door, capital comes in, and the market eventually tests who built for permanence and who built to navigate hard moments.

The question is not whether credit as an asset class is sound. It is.

The question is which corners of the market were built to withstand the volatility that arrives when conditions change, and which were assembled during a period when confidence outpaced caution.

History does not punish optimism. It punishes the absence of preparation and discipline. Both conditions can exist in the same market, and that is the lens through which we are approaching this note.

Partnership Updates

Citi and HPS announced a €15 billion Private Capital Program. The Program will finance €15 billion of sub-investment grade debt opportunities in EMEA over the next five years. Citi will source businesses based in Continental Europe, the UK, and eventually the Middle East. More here

Manager Updates

Abry Private Debt acquired a $330 million private credit portfolio with Coller Capital. The portfolio is primarily senior secured loans across a variety of industries, including commercial and professional services, healthcare, and consumer discretionary. All underlying investments are backed by established sponsors. Abry will assume an active management role, working directly with sponsors, lenders, and management teams throughout its hold period. More here

Switzerland’s public sector pension fund Publica is preparing to allocate up to $1.1bn into private credit. The fund is looking for external managers for two separate direct lending mandates: one focused on Europe, worth up to €500 million, and another targeting the US market for up to $550 million. More here

Switzerland’s pension funds remain underallocated to alternatives, despite being allowed to allocate up to 15%. With current allocations still below 7%, there is considerable room for expansion.

Federal prosecutors are reportedly examining valuation practices at BlackRock TCP Capital Corp (TCPC). TCPC disclosed an unusual off-cycle update in January, warning that it expected to reduce the value of its portfolio by about 19%. The announcement triggered a sharp share price drop and was followed by multiple class-action lawsuits from investors alleging misleading disclosures and improper valuation of loan assets. Link

Bank SRTs

MUFG is exploring an SRT tied to $2 billion of credit exposure to private credit funds. The deal would shift potential losses on BDC credit lines to institutional investors, while MUFG keeps the underlying loans on its balance sheet. More here

JPMorgan is reportedly exploring, and SRT tied $4 billion of NAV loans spanning across North America, Europe, and the Middle East. Investors are expected to receive low-teens returns in exchange for absorbing first-loss exposure. More here

Yields aren’t a freebie.

Some borrowers will have a tougher time than during the low-rate era of 2009-2021. This creates opportunities for credit managers to demonstrate skill by avoiding the losers.

It also creates the pockets of dislocation pursued by intrepid investors, who can see through volatility to provide complex capital solutions when they’re needed most.

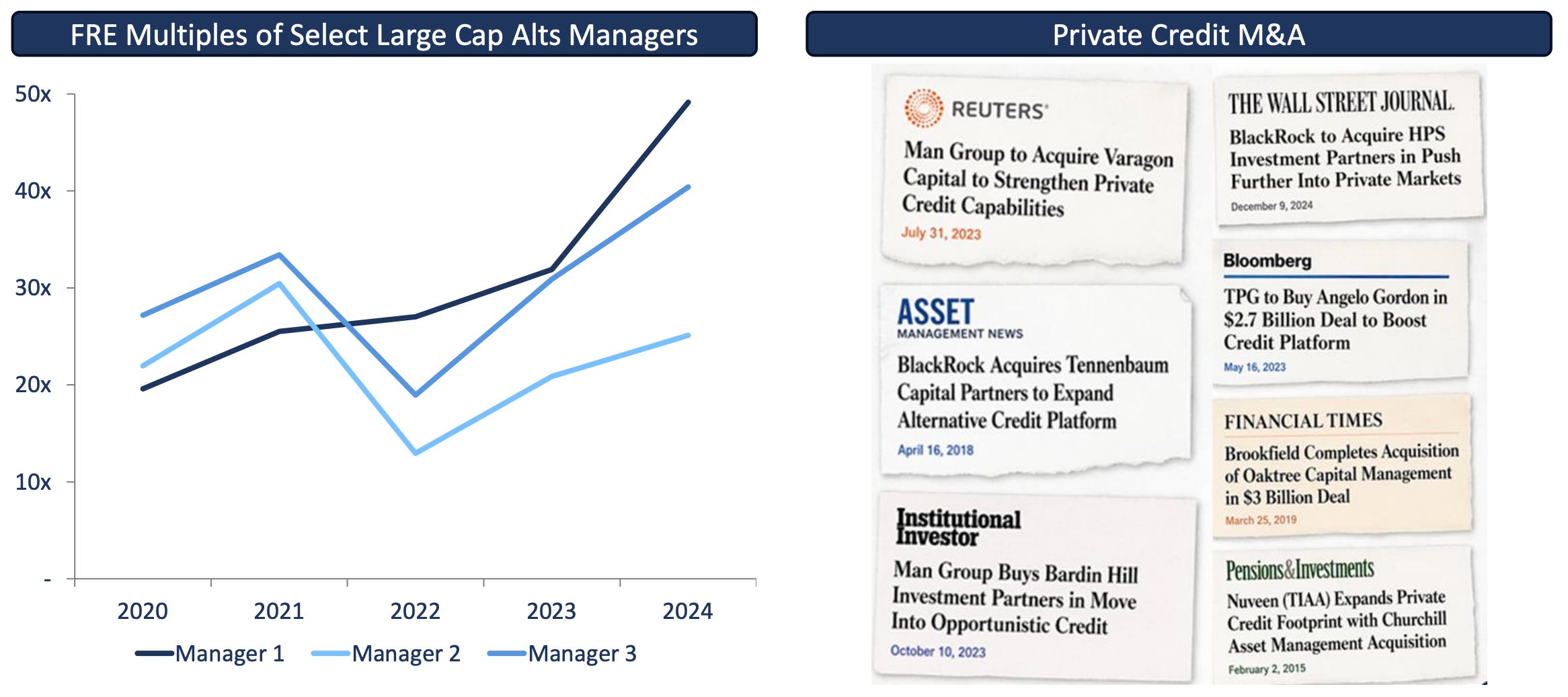

Diameter: WTF Is Going On In Private Credit?

Diameter published a 59 page deck summarising the state of private credit and where it sees opportunities. I’d recommend you read the whole report, below are a few of my favourites

Fees on private credit vehicles have exceeded those of traded credit

Public alternatives managers leaned into AUM and FRE growth; Private Credit became their engine

Private Credit M&A expanded amid FRE multiple expansion

HPS was acquired for ~30x forward FRE in July 2025

Industrial-scale origination and deployment drove PC platforms’ enterprise value

This has many overlaps with to Sixth Street’s recent “factory model” piece.

Where do Diameter opportunities?

👉 Read the full report here (Page 50+ for opportunities).

💰Fundraising News

Direct Lending

Barings raised $19 billion for its latest global direct lending vintage. The strategy focuses on upper-middle-market borrowers with roughly $15m–75m EBITDA across North America and Europe.

Antares Capital, a Chicago-based alternative credit manager, raised $8.5 billion for its third Senior Loan Fund. The fund invests in senior secured loans across U.S. and Canadian borrowers. More here

Stellus Capital Management, a Houston-based direct lender, closed its $1.5 billion Stellus Credit Fund IV. The fund provides senior secured loans to sponsored businesses in the United States and Canada. It has already invested in 44 portfolio companies. More here

Asia

Värde Partners launched its $1 billion Asia-focused private debt fund. The fund will invest across India, Australia, and Southeast Asia. The vehicle marks Varde's first Asia fund exclusively focused on private credit. More here and here

ASK Alternates, a Mumbai-based private credit manager backed by Blackstone, launched its second private credit fund with a ~$250 million target. The fund will invest in senior secured lending to high-quality Indian businesses. It will target a gross IRR of 14 to 16 percent, in line with the 15 percent gross IRR delivered by Fund I. More here

Granite Asia, a Singapore-based multi-asset investment manager, is raising final-close capital via DBS Private Bank for its inaugural closed-ended private credit fund. The fund held its first close at $350 million in 2025, with anchor commitments led by Temasek and Khazanah Nasional, and is targeting a final close at $500 million. The strategy targets returns of 16 to 20 percent per annum, with investor cash yields of approximately 8 to 10 percent annually. More here

Investment Grade

PGIM launched the PGIM Investment Grade Private Credit Fund, the first private credit collective investment trust designed for defined contribution retirement plans. The fund provides exposure to investment-grade private credit and is intended for use within target date funds, stable value funds, and other multimanager retirement structures. More here

Specialist

Shamrock Capital, a Los Angeles-based manager specializing in media, entertainment, and communications, closed its $813 million Shamrock Capital Content Fund IV. Consistent with its predecessor funds, Content IV will focus on acquiring premium, cash flow-generating content and media rights across the evolving global entertainment landscape. The strategy’s current pipeline spans music, film, television, sports, video games, and creator economy opportunities. More here

Didn’t make this week’s cut

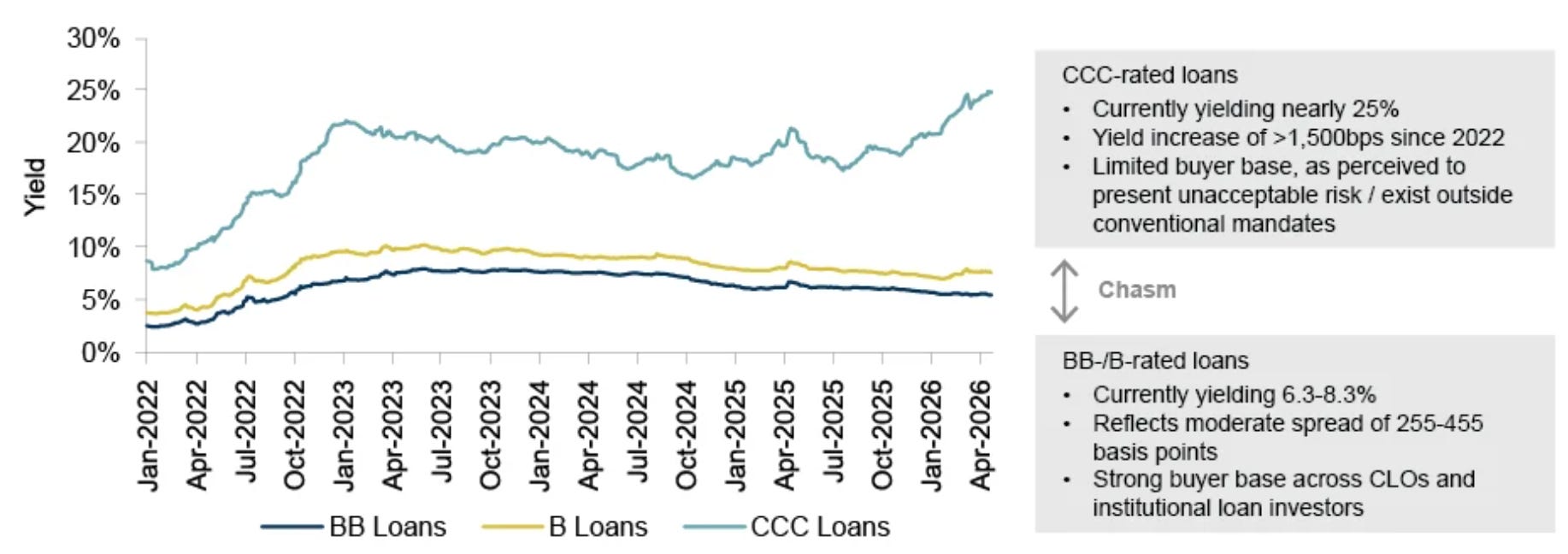

Dispersion Revisited

There’s been no let-up for CCC-rated loans, with spreads widening by over 300 bps so far this year.

In contrast, higher-rated credits have shown remarkable resilience: BB-rated loan spreads have marginally tightened this year, making for a yield of just over 6% – about a quarter of the level of CCCs. In short, the rating bands are a world apart, with the sort of aggressive bifurcation normally seen in a recession. So, what’s going on?

Market participants are expressing a clear view: the weakest credits cannot handle elevated interest rates and will struggle to refinance through mainstream channels. The fundamentals appear to validate this concern: leverage on CCC-rated loans has crept higher while other rating categories haven’t seen such increases.

Given the risk of default and the reality of poor recovery rates, buyers expect to be compensated in the form of an outsized spread. Meanwhile, higher-quality names continue to attract a broad buyer base, particularly from CLOs, thereby keeping spreads tight.

What if the universe of private credit is larger than you think?

Barings: What You Don’t Invest In Matters. Link

This newsletter is for educational and entertainment purposes only. It should not be taken as investment advice.

The CCC bifurcation is the best understand here. 300bps of widening on the weakest credits while BB tightens isnt a credit story, its the market quietly separating what can refinance at current rates from what cant.

The DOJ examining TCPCs valuation practices is the other part worth watching. The marks stayed flat while the portfolio deteriorated. The off cycle NAV cut of 19% was the tell. Adjusted EBITDA did the same work in 2005 that stated income did. The footnotes always get there eventually.