Howard Marks: Mistakes cause mispricings.

The bloom is off the rose, we’ll get much better buying opportunities in the months ahead

👋 Hey, Nick here. A big welcome to the new subscribers from Goldman Sachs, Mizuho | Greenhill, and US Bank. You’re now part of a select group of 2,733 subscribers. This is the 160th edition of my weekly newsletter.

If you’re reading this on Outlook, most of the graphs won’t show. I’d recommend you read it online

📕 Reads of the Week

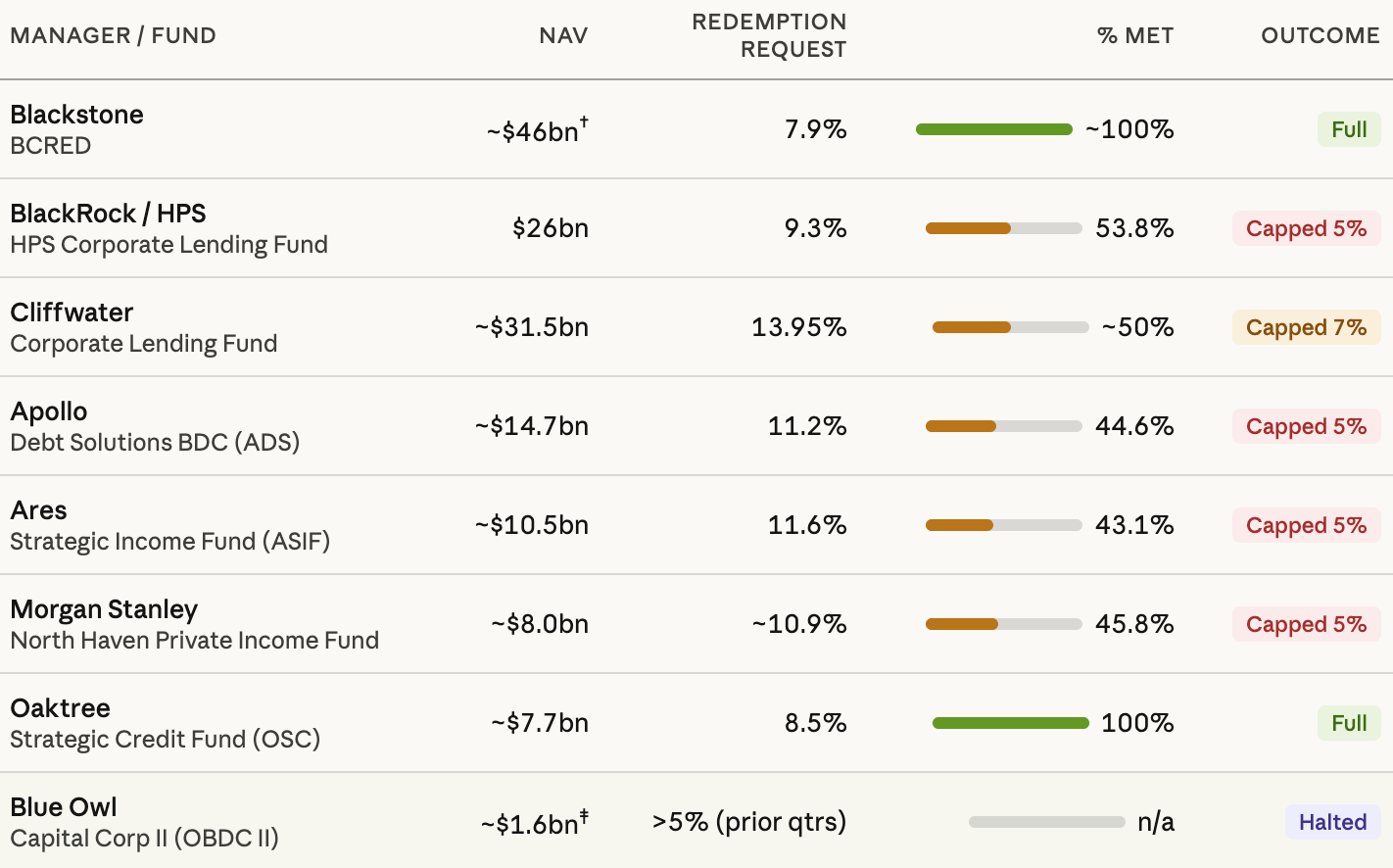

The retail channel is a little bit less than 20% of the assets in the direct lending.

Over 80 percent of the assets do not have this liquidation mechanism that could result in these fire sales and then downward spiral in prices.

Goldman Sachs: Private Credit Concerns in Context (Link)

Manager Updates

Partners Capital: Redemption pressure is generating opportunities within secondaries to acquire performing loans at material discounts. Link

Dell Family Office Hunts Private Credit ‘Gems’ Amid Turmoil. Link

CVC Credit Perspectives. Link

Carlyle and Andalusian Credit Company launch partnership to invest in middle-market loan assets and other cash-flow-producing private credit interests. Link

Market Updates

KKR: Thoughts From Japan Link

Pemberton: Separating Signal from Noise and Why European Private is Credit Different Link

Tikehau: A Search For Harmony. Link

BDC / Interval Fund Updates

JPMorgan launches Public and Private Credit interval fund with 7.5% quarterly repurchase capacity.😉 Link

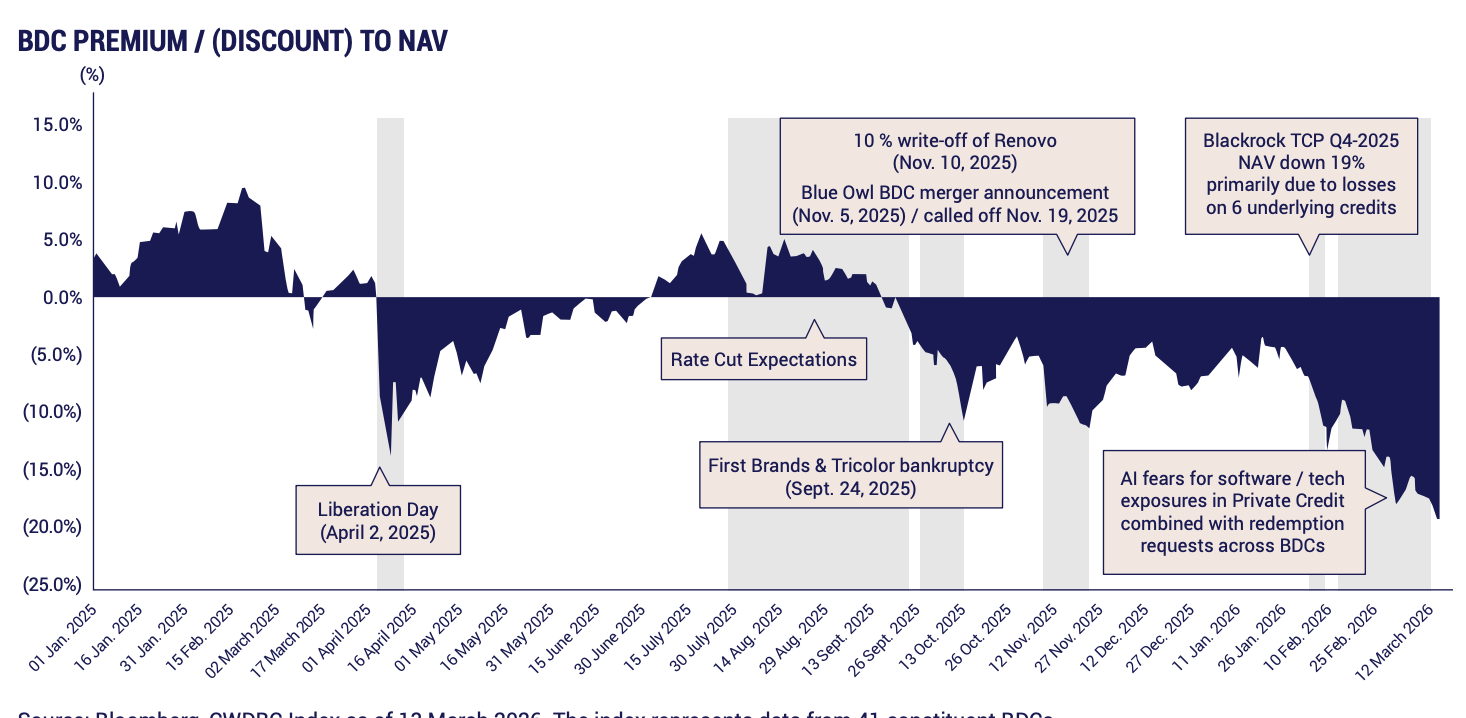

Moody's Ratings downgrades FS KKR Capital Corp.

PIK income was 14.7% of FSK's total investment, significantly higher than the peer median of 6.3%.

FSK's debt-to-equity leverage increased to 1.30x compared to 1.11x.

The stable outlook reflects FSK's sufficient liquidity position, well-laddered debt maturities, and low absolute leverage on a debt-to-equity basis.

They expect its asset quality to remain challenged, driving more volatile profitability than peers.

Tikehau: Liquidity and Gating. Link

Mistakes cause mispricings.

Howard Marks shares his reflections on themes from Oaktree’s recent client conference. I’d recommend listening to his comments on buying from sellers who are making mistakes (10:36)

Market efficiency means that every security is awarded a price, and if you buy it at that price, you get a fair risk-adjusted return. No more, no less…

We’re not happy with that. We want to get excess return, returns that are more than commensurate with risk. To do that, you have to buy assets, not at fair prices, but at unfair prices. We want to buy things for less than they’re worth. That requires cooperation for someone who’s willing to sell something for less than it’s worth.

And who volunteers for that job?

We want to buy from sellers who are making mistakes. And a lot of these in the history of Oaktree have also stemmed from people who bought companies and made mistakes. They overestimated the growth potential, overestimated the solidity of the earnings, overestimated the ability to survive or thrive in a negative economic environment, levered up too much, and eventually became distressed as a result.

What are some of the sources of the bargains we seek?

Complexity - People don’t understand something, and they’re scared by its complexity.

Difficult to source. - Some of these things are held deep in portfolios in the bowels of institutions, and we have to go find them and get somebody to sell them to us.

Supply, demand - There are a lot of people who want to sell something at a given point in time, fewer people want to buy it, that pushes the price down, hopefully to unreasonably low levels where we can pick it up.

Technical reasons - There was a rule for a while that if a bond was downgraded below investment grade, certain holders had to sell it. Now, they might not want to sell it if the price is unreasonably low, but the rules require them to do so. That’s technical.

In the last few months, the tide has been going out, especially in areas like private credit and we start to see which structures may have been unwise.We actually haven’t had many defaults yet, so we haven’t had a chance yet to see who made bad loans. That’s coming too.

We’re ready for shakiness in ‘26.

And I think that when the bloom is off the rose and people start thinking about the negatives and not just the positives, and when they start to reflect risk aversion and not just FOMO, I think we’ll get much better buying opportunities in the months ahead than we did in the months just passed.

HALO 🏭 🚄

Hard Assets, Low Obsolescence

Asset light is out. Hard assets are in. Factories, fiber and railroads are the new celebrities of the investing world. Like most inflections, the trend has even earned its own acronym. HALO (Hard Assets, Low Obsolescence)

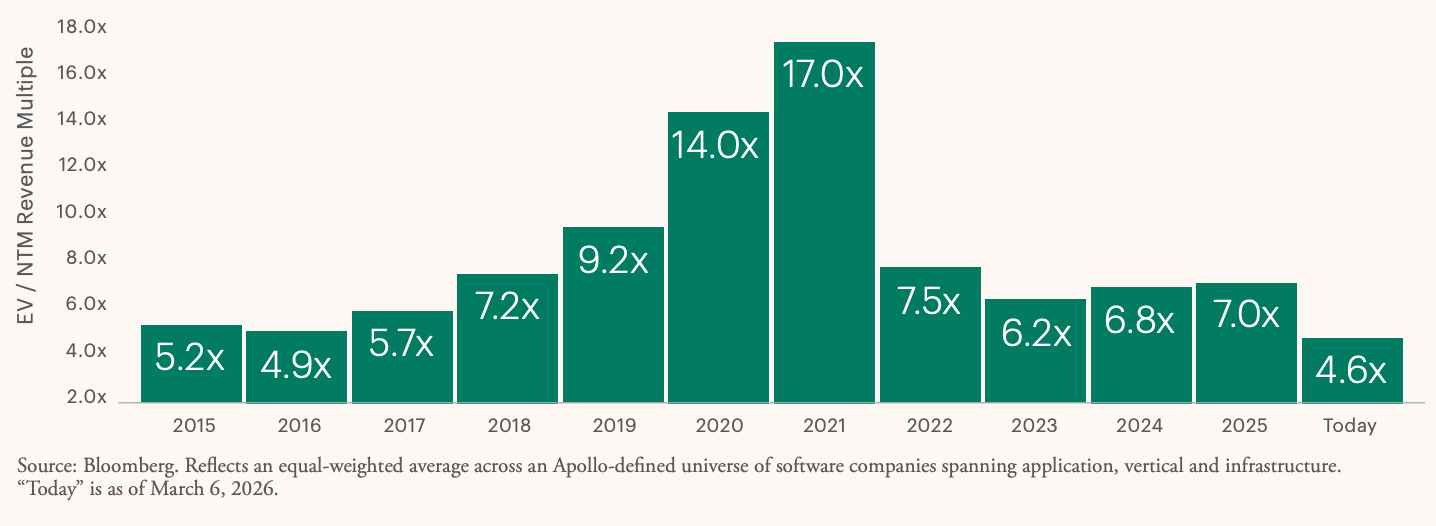

HALO owes its existence to the growing angst surrounding increasingly powerful AI models and their potential to disrupt large swaths of the economy. Enterprise SaaS companies, whose revenue multiples have collapsed by 38% over the past six months, have borne the brunt of these obsolescence fears. But the wave of disruption anxiety has not stopped there; it has spread to a range of labor-intensive professions, including accounting, insurance brokerage and wealth advisory

Enterprise SaaS companies have collapsed by 38% over the past six months

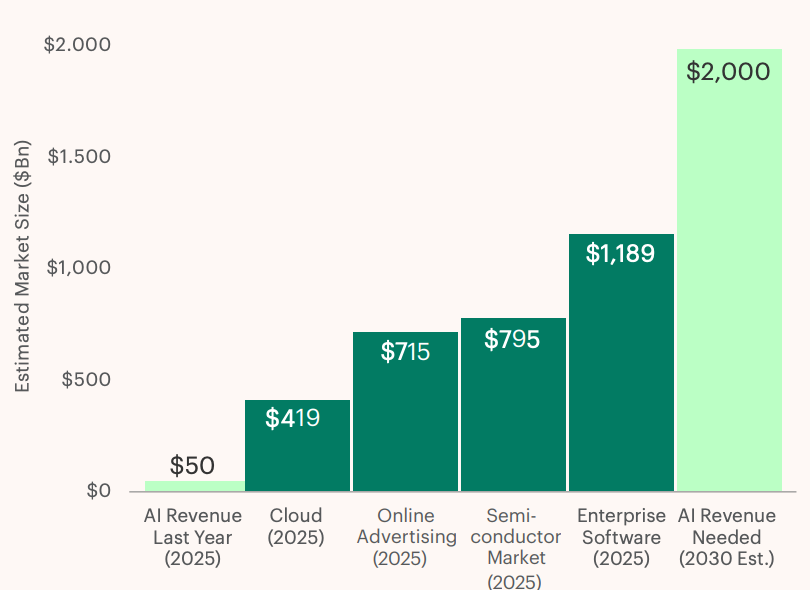

The market is currently expecting $4 trillion of digital infrastructure investment by 2030

For this investment to deliver an acceptable return, AI revenue must climb to $2 trillion by 2030.

This is a 40x increase vs 2025 AI Revenue.

Some of this will come from GPU-accelerated improvements to existing software workloads, like better advertising models and recommendation engines.

But the bulk will have to come from genuinely new AI-driven products and services

$2 trillion of revenue is equal to the total size of the global enterprise software and online advertising markets combined.

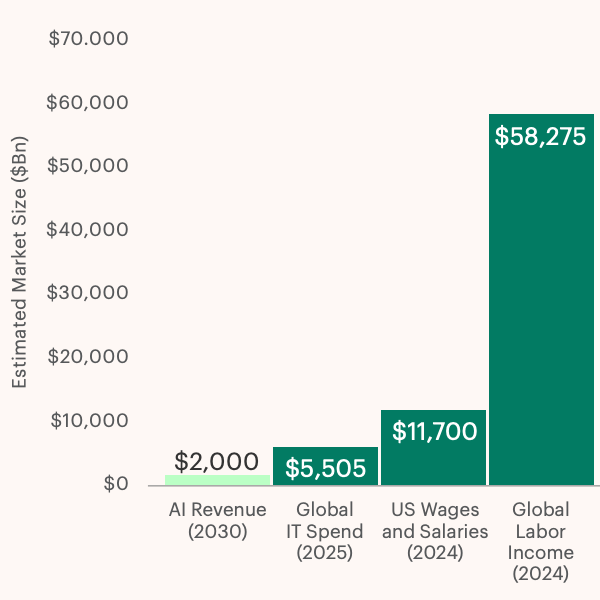

Admittedly, these industries do not have the ambition of AI which hopes to automate a large portion of the $60 trillion in global knowledge workforce compensation.

Through that lens, $2 trillion represents only ~3% penetration.

Balance sheet capacity is becoming a gating factor across the AI ecosystem

OpenAI finalized a $100 billion round, after previously raising a record-breaking $40 billion

Apollo is most focused on how this multi-trillion-dollar investment in infrastructure will be financed and who ultimately bears the balance sheet risk if revenue realization lags.

The faster AI-driven disruption converts into recurring revenue and free cash flow, the more self-funding the infrastructure buildout becomes.

💰Fundraising News

Pollen Street, a London-based manager, raised $2.1 billion for its Credit Fund IV. The asset-backed lender finances everything from building homes, funding SMEs, and vehicle financing. It provides predominantly senior secured loans to non-bank lenders, leasing businesses, and technology companies. More here and here

Treville Capital Management, a US-based manager, closed its $500 million Capital Solution fund. The fund invests across the capital structure, including senior secured loans, junior debt, and preferred equity in a wide variety of sectors. Link

SCOR Investment Partners, a French manager, raised $300 million for its Real Estate Loans V fund. The fund finances the renovation, restructuring, repositioning, or development of real estate across major European metropolitan areas. It invests through senior loans and targets an IRR of around 6%. Link

This newsletter is for educational and entertainment purposes only. It should not be taken as investment advice.

Didn't realise that FS KKR had such significant Software exposure, both directly and through Credit Opportunities Partners JV, LL. Just reviewed the portfolio. This potentially explains the PIK income.

Great Read! Question for you In an increasingly institutionalized market where amateur retail emotionality is often dampened by algorithmic trading and professional risk management, where is the most sustainable source of mistakes today? Is it still human psychology, or is it now found in structural/mandate-driven constraints (like forced selling due to credit rating downgrades)