KKR's Divergence Conundrum

Fundraisings from Trimontium, Altavair and Blackstone Credit & Insurance

👋 Hey, Nick here. A big welcome to the new subscribers from The Central Bank of China, Federated Hermes, and Thirdpath. You’re now part of a select group of 3,104 subscribers, reading the 172nd edition of my private credit newsletter.

If you’re reading this on Outlook, most of the graphs won’t show. I’d recommend you read it online

📕 Reads of the Week

Nobody’s abandoning private credit.

Institutions will continue to stay the course, and private credit will prove itself to be very resilient.

Manager Updates

Recommended Read: Cliffwater Corporate Lending Fund: The Machine Slows Down. [Read here] - Message me if you’re not a subscriber and I’ll gift you access.

GIC is divesting $2 billion of private credit holdings. GIC has previously sold down its legacy fund interests, including exposure to managers such as Blackstone Inc. and Apollo Global Management, as part of its broader portfolio management activities. Evercore has reportedly been appointed to advise on the transaction. [Read here]

Canyon Partners, a Dallas-based manager, launched Canyon ABF Partners. The joint venture is anchored by Daiichi Life Insurance and Korea Investment Holdings, which will provide a permanent balance sheet capital designed to facilitate $5+ billion of annual origination capacity. [Read here]

Brookfield provides Papa John’s with $725 million of preferred equity. The deal has an all-in yield of 12%, with 10% PIK and 2% cash. The preferred equity also includes a minimum multiple on invested capital of 1.6x. [Read here]

Market Updates

Much Ado About Nothing

You may have seen some noise about this Columbia study on private credit.

The paper’s key conclusions were:

Private-letter ratings systematically understate investment risk.

U.S Insurers would need to hold about $4.5 billion more capital if the ratings were aligned with the perceived impairment risk.

KBRA published its thoughts on the piece:

$4 billion is only 0.5% of the U.S. life insurance industry’s capital.

Non-investment grade only accounts for 10% of the total private letter rating portfolio. Why did the Columbia study apply the same extrapolations across the whole book?

A reminder that private credit’s scale comes with strings attached. The Australian Securities and Investments Commission has officially put private credit managers on notice. Link

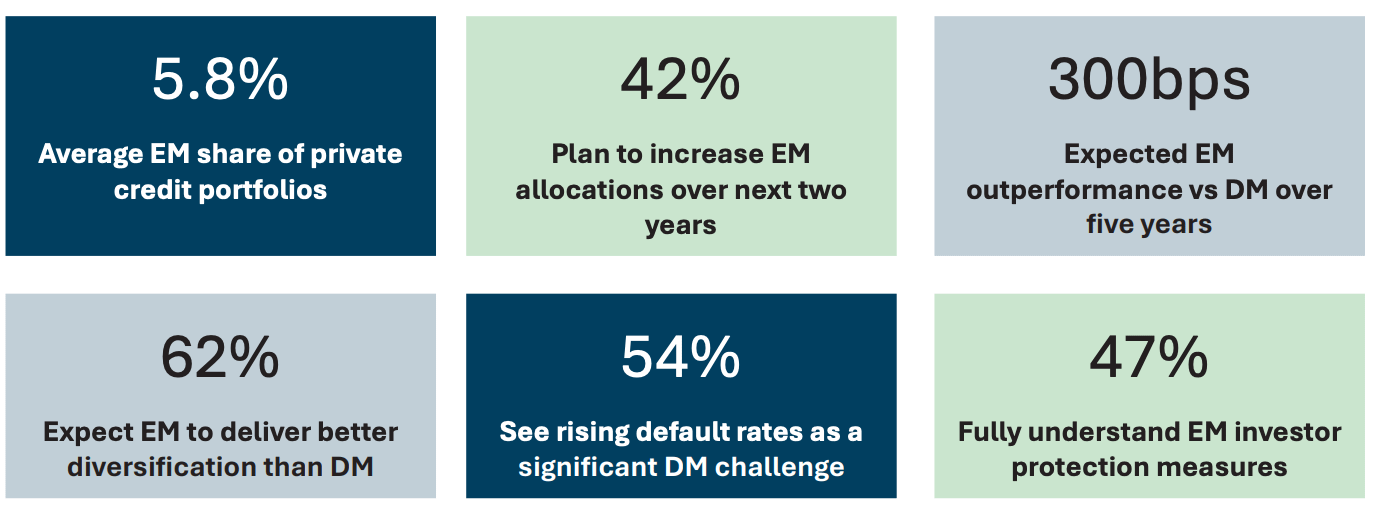

Gemcorp’s Emerging Market Survey: Key Numbers at a Glance. (Link)

BDC’s Q2 Redemptions: Week 3

Oaktree’s Strategic Credit fund was the only addition this week, receiving redemptions of 4.5%. For context, this was nearly half of Q1’s redemption requests of 8.5%.

Oaktree met the full redemption.

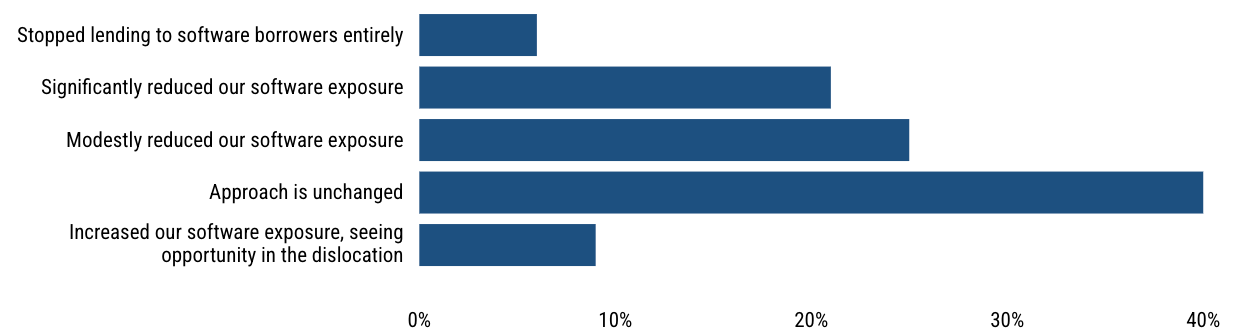

Software and AI Updates

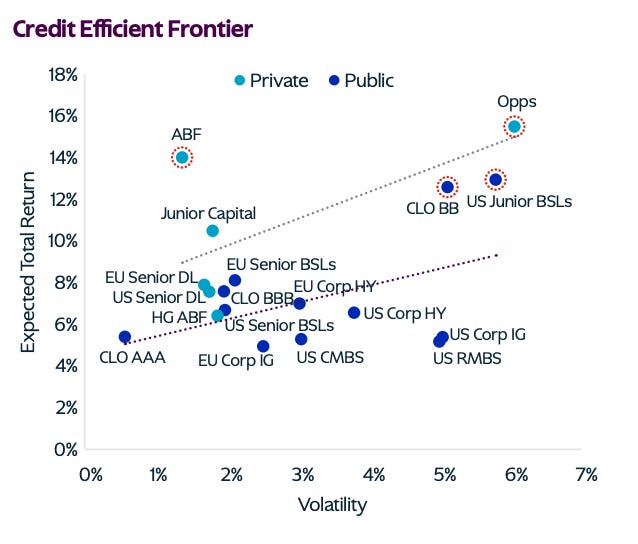

KKR’s Divergence Conundrum

The Divergence Conundrum is an investing landscape where certain segments of the economy and markets are starved for capital, while others are flush with attractive financing options.

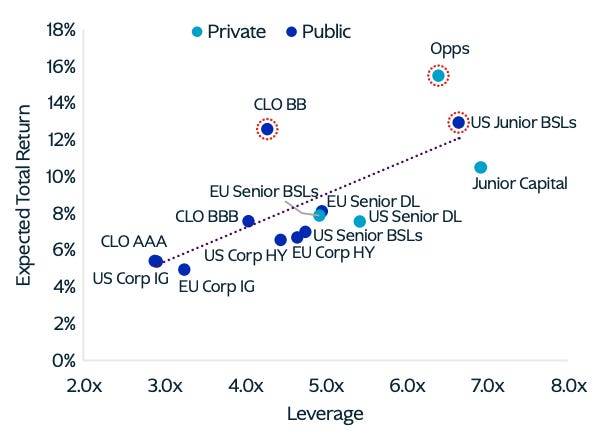

Where Is Relative Value Most Attractive Today in Credit?

The biggest shift in credit this year has not been spreads.

It has been dispersion driven by software-related credit concerns and redemption pressures in select areas of the private credit market.

The market has become less willing to reward aggressive underwriting, elevated leverage, and concentrated risk.

There are higher levels of defaults and lower levels of recoveries.

Defaults, including PIK and extensions, have been running around five percent since August 2024.

The corporate direct lending market will consolidate the same way that the liquid credit markets did in prior decades

Private Credit is in a period of price discovery.

Spreads continue to widen,

Original issue discount levels have increased,

Lenders are increasingly able to secure tighter structures and stronger covenants.

This creates a better entry point for new capital deployment.

Signals are important.

Structure, collateral, documentation, and sponsor behavior are increasingly becoming the real drivers of outcomes in credit.

Reaching for incremental yield is not rewarded.

Stay selective and focus on situations where expected returns are attractive relative to volatility, leverage, and potential loss.

There is growing gap between strong and weak credits.

Asset-Based Finance remains attractive given its diversified collateral pools, contractual cash flows, and expanding opportunity set as assets continue to migrate away from bank balance sheets.

Capital Solutions unlock value for businesses where customized financing structures providing meaningful risk mitigation and equity upside.

This is particularly relevant where IPO and M&A activity remains uneven and sponsor exit timelines have been extended.

Private Credit is increasingly moving towards bifurcation.

The distinction will not just be between good and bad credits, but between well-constructed and poorly constructed portfolios

💰Fundraising News

Trimontium, a London-based manager, announced its launch with $1.5 billion in assets under management. The opportunistic strategy will invest across corporate capital (across debt, hybrid, and equity), special situations, structured and asset-backed credit, and uncorrelated asset classes, including IP rights and royalties. It can invest in both European and North American markets. More here

Altavair, a US aviation lessor, raised $1.4 billion from KKR. The investment will primarily come from KKR’s Infrastructure and Asset-Based Finance strategies. KKR has committed more than $8 billion with Altavair since 2018. Over that time, they have acquired 188 commercial aircraft and engine assets through a variety of transactions, including lessor trades, airline-direct new and used sale leasebacks, passenger-to-freight conversions, and structured transactions. More here

Blackstone Credit & Insurance launched SablePointe, a platform supporting origination, underwriting, and portfolio management in asset-based lending. SablePointe will support BXCI as it sources, structures, and manages senior secured asset-based and first-out credit facilities for corporate borrowers. More here

This newsletter is for educational and entertainment purposes only. It should not be taken as investment advice.

great read as always!