Milken: Private Credit’s Dispersion Has Been Abnormally Compressed

+ Bonus from Neuberger. Why the BDC Sell-Off Tells an Incomplete Story

👋 Hey, Nick here. A big welcome to the new subscribers from Apollo, Golub and Pitchbook. You’re now part of a select group of 2,958 subscribers. This is the 166th edition of my private credit newsletter.

The Milken conference brings together the world’s best minds to tackle some of the most urgent challenges. This year’s speakers included David Beckham, John Legend and Peyton Manning. Civilisation is in safe hands.

Alongside the minor matters of global health, education and democracy, Milken also found time for the question troubling every private markets investor:

“How do I get my money back?

Joking aside, there is a surprising amount of great content from Milken this year. I’ve pulled together a summary of my top quotes below with timestamps included for anyone who would rather not spend several hours watching private markets panels.

If you’re reading this on Outlook, most of the graphs won’t show. I’d recommend you read it online

📕 Reads of the Week

“Over the last 25 years, there’s only been six years where the distributions in private equity have been lower than 20% of NAV.

It was 2001, 2002, 2009, ‘23, ‘24, ‘25.

So this is the longest recovery back to liquidity private equity has ever seen.”

Yann Robard (Dawson Partners), Navigating Liquidity Challenges in Private Equity panel (05:46)

Market Updates

Apollo: Europe is undergoing a structural shift in how companies access capital. Link

Blackrock: Putting Private Credit Concerns in Perspective

Powell: We don’t see any risk of contagion. Link

FSB: Vulnerabilities in Private Credit. Link

ILPA’s Guidance on Continuation Funds. Link (or if you’re the FT “Conflict Vehicles”)

👉 Read Pitchbook’s report

Manager Updates

Michael Milken: What percent of your assets that you manage are redeemable on a quarterly basis?

Bruce Flatt: Probably less than 1 percent.

Larry Fink: It’s certainly less than 1 percent [for BlackRock]

Blue Owl made more than 10x on its SpaceX Investment. Link

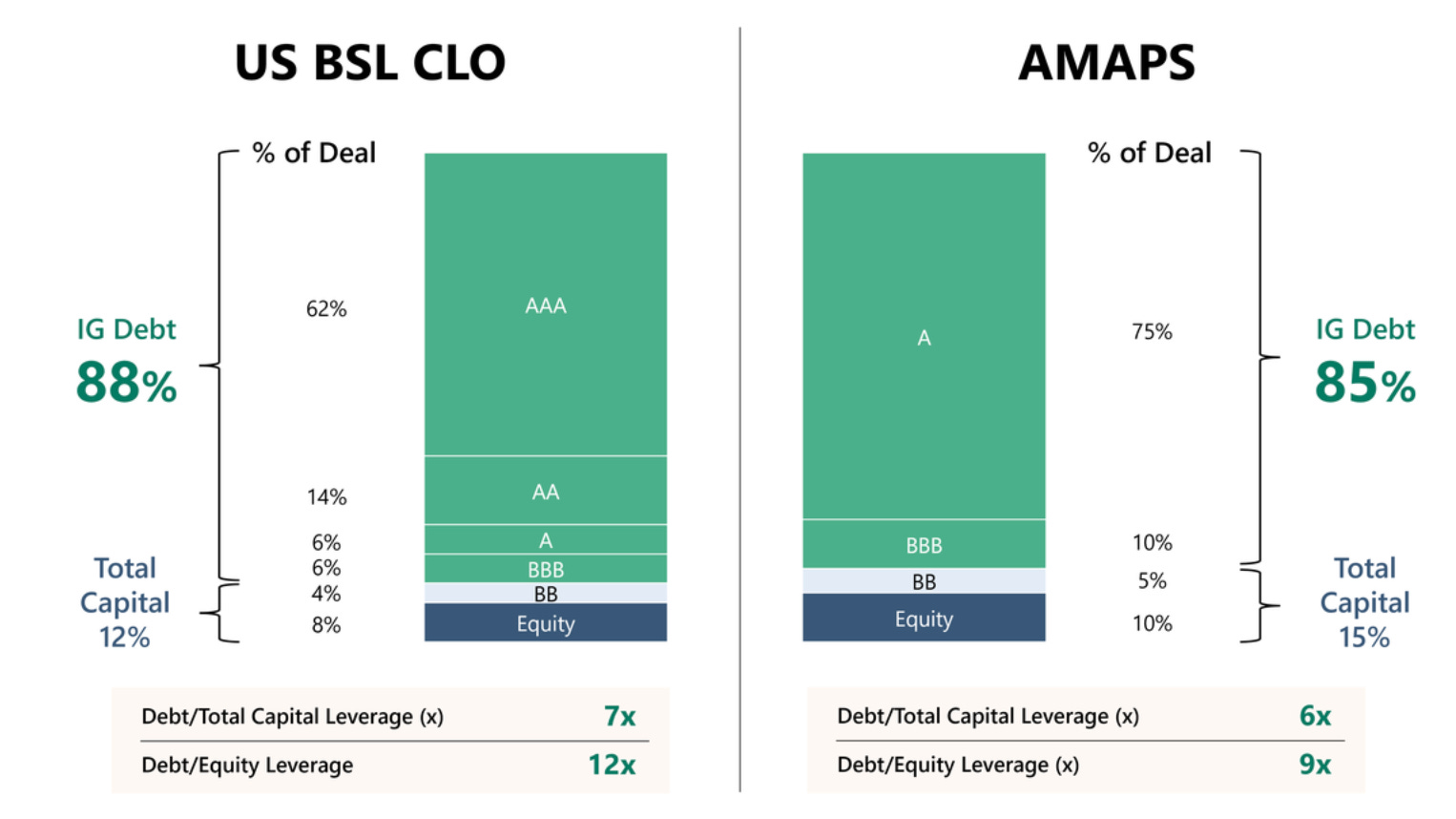

Apollo launches its Multi-Asset Prime Securities,

A structured credit product enabling access to more diversified and higher-credit-quality assets that are risk-managed every day.

In comparison to US BSL CLOs, the vehicle has a thicker equity tranche and is approximately 85% investment-grade rated by leading agencies, with underlying collateral that is more diverse and significantly higher rated. It was structured with investors in mind.

BDC / Interval Fund Updates

LibreMax Capital, a New York-based asset-backed manager, launched its first interval fund with $885 million of commitments. The fund invests in credit backed by consumer, housing, and commercial receivables.

Public BDCs are less crowded than the headlines suggest.

Milken Conference 2026

Below are my highlights from the Milken Conference last week. The link below the quote takes you directly to the video.

You’ll need to register for a free account but the amount of content is worth it.

Private credit dispersion has been abnormally compressed, not abnormally wide

“When you look back the last 10 years, the difference between a top quartile manager and a bottom quartile manager in private credit has only been about 250 basis points. So there’s been no dispersion. When you look at a typical or most other typical asset classes in credit, that’s normally about 500 basis points.”

Lee Kruter (GoldenTree Asset Management), Credit Outlook panel (04:05)

The retail money story is the real risk

“Most asset managers want to see a lot of this retirement money come into the market because it increases AUMs, it increases fees, it’s good for public company growth. I’m concerned about it... when all that money comes in, private credit, which should be an alpha product, becomes a beta product. It becomes no different than syndicated loan and fixed-income dollars... institutional investors all over the world are concerned about this. Not private credit, not about defaults, not about underwriting. They’re concerned about retail money coming into the funds that they invest with, and they do not want to see retail money invested side by side with them in institutional capital accounts because they’re concerned about deterioration.”

Ted Koenig (Monroe Capital), Private Credit Institutional Portfolio panel (29:30)

The 2022 vintage software loans never delevered

“If you look at a subset of broadly syndicated loans and software that were around in the end of 2022 and still around now, well, guess what’s happened? They never de-levered. The leverage is roughly the same as it was back then because the growth didn’t materialize in the way that they were hoping to, and if you bought them with a 40% LTV then, and equity valuations have come down, well, now you’re looking at least at 70 to 75% LTV on average.”

Brad Rogoff (Barclays), Banks Private Credit and the Future of Risk panel (42:00)

1,000 PE deals are stuck and many of them no one wants

“There were 1,000 transactions done in the PE community between 2015 and 2022 of $500 million or greater. Very few have exited. Some will find strategics, not that many. They’re all going to have to get sold. And a lot of them, nobody wants. Because the other filter for exits today, who is the buyer? Fidelity, a corporate, a CV. They only want the best.”

Jonathan Sokoloff (Leonard Green), Navigating Liquidity Challenges in Private Equity panel (09:20_

Asset-based finance is harder than direct lending, and the tourists do not realise that

“I think it’s a lot harder than private credit in the direct lending side. You need a lot of experience working with these non-bank originators, knowing how to look at the data, making sure you’re verifying your collateral... I think there’s a false sense of security sometimes that people can have when they see diversification and asset coverage on these deals... As people start to get attracted to this space, I think you’re going to see some tourists come in that probably don’t have that level of expertise.”

Jack (Fortress), ABF/ABL/Specialty Finance panel (24:08)

The scale gap, OpenAI round versus German growth funding

“The largest funding round agreed on for an OpenAI is $122 billion, right? The total collective growth funding in Germany last year was €8.4 billion.”

Hendrik Brandis (Earlybird Venture Capital), The European Opportunity panel (40:15)

“If you can earn north of 12, nothing else matters.

So don’t try to earn 35. It’s good if you earn 35. But don’t try to earn 35.

arn 12 every year for very long periods of time.”

Bruce Flatt (Brookfield), Conversation with Larry Fink and Bruce Flatt (19:40)

Neuberger: Why the BDC Sell-Off Tells an Incomplete Story

Neuberger published a great piece on BDCs. Below are my highlights.

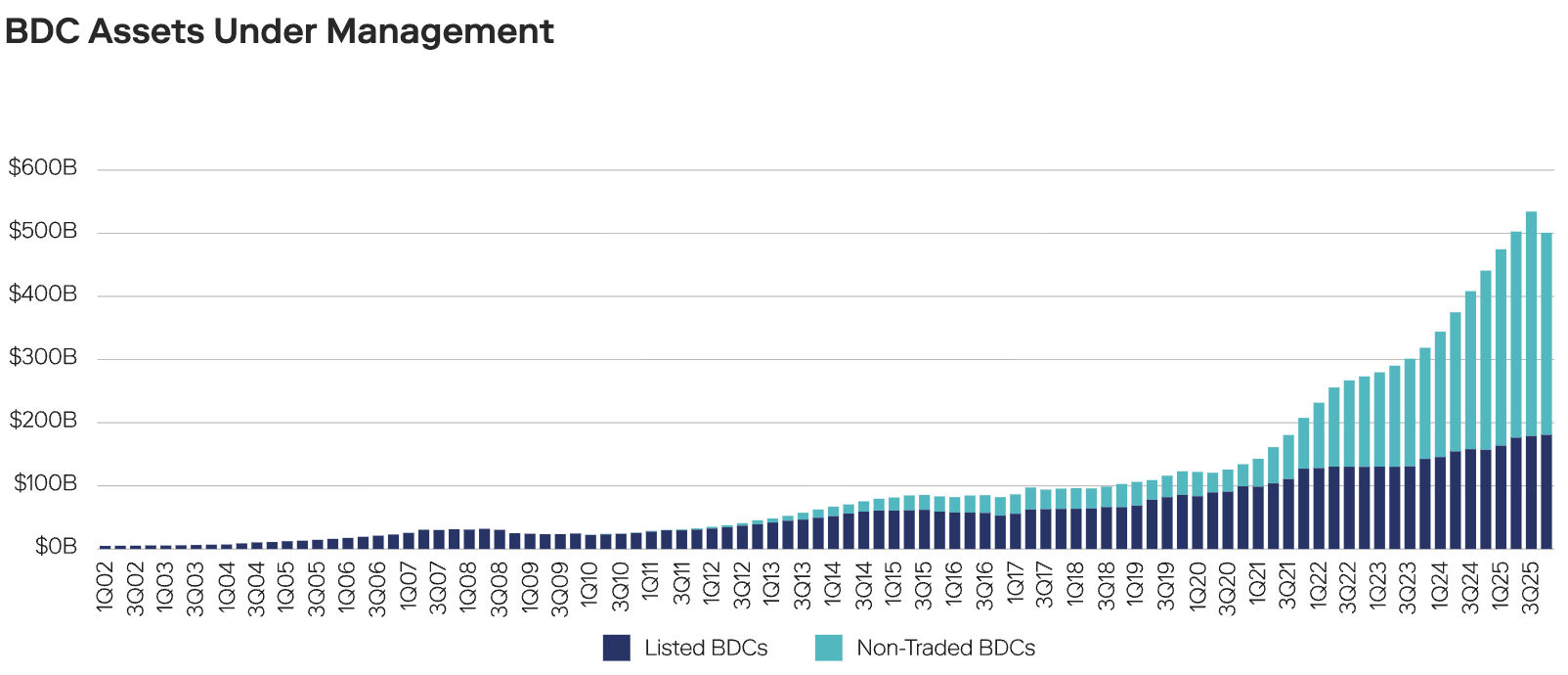

While BDC Assets Have Grown, They Remain a Small Part of the Private Credit Universe

Some investors may be missing the nuance of the private credit market, especially as the entire BDC universe, listed and non-traded combined, amounts to only about $500 billion.

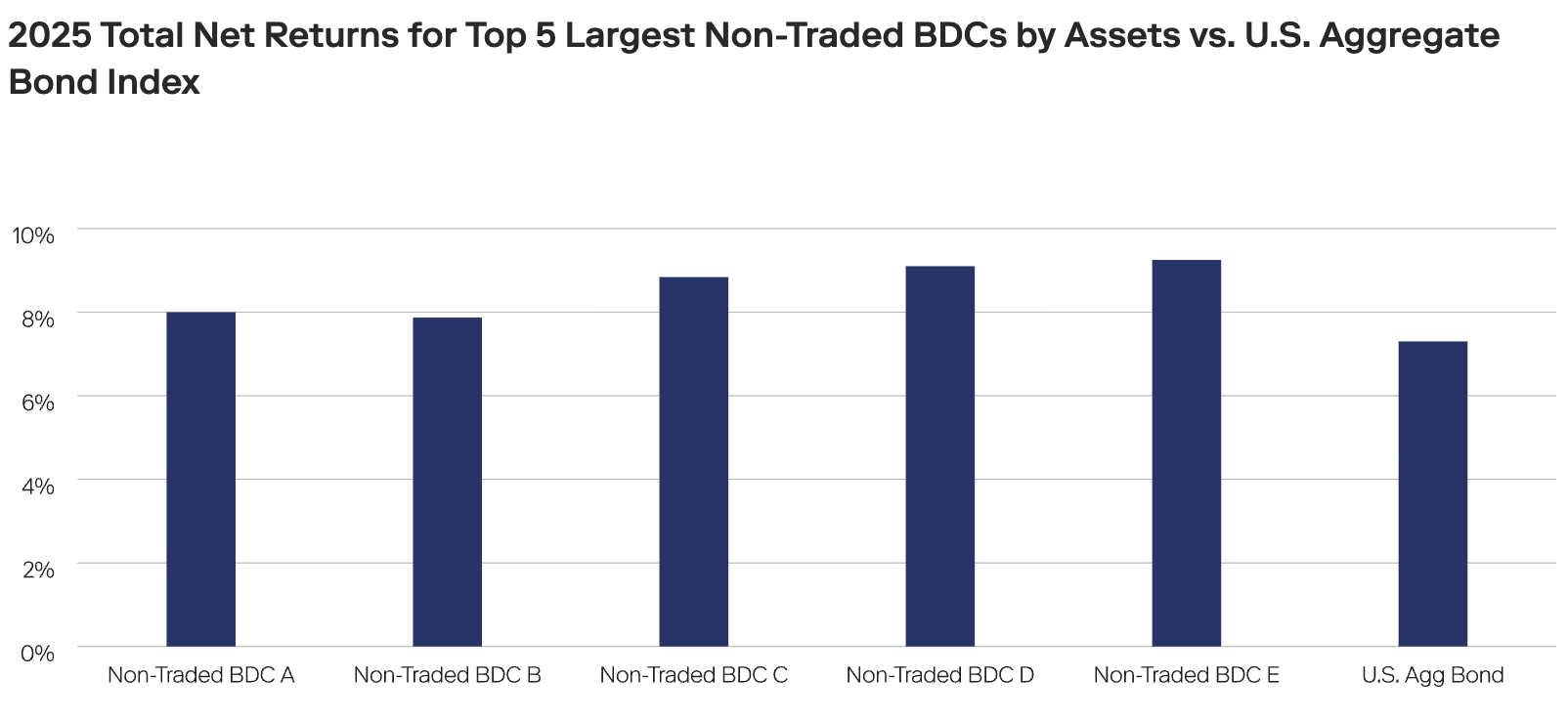

Non-Traded BDCs: Redemptions Don’t Appear to Reflect Performance

Many of the larger BDC vehicles produced high single-digit returns last year, which compares favorably to a range of fixed income alternatives. Redemptions reflect other factors, including investor liquidity needs and a broader reassessment of portfolio positioning, rather than dissatisfaction with how the underlying assets have performed.

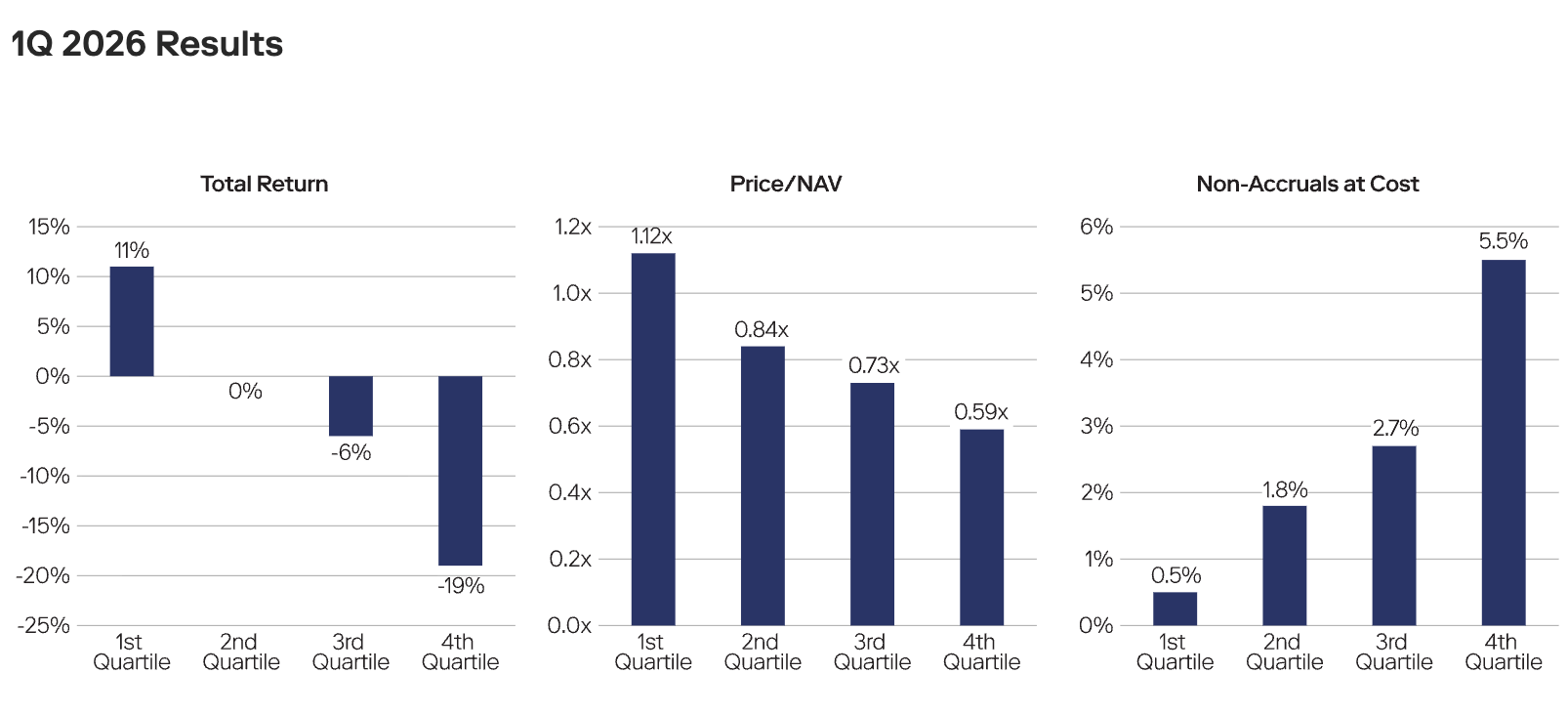

Listed BDCs Have Shown Wide Performance Dispersion Overall

💰Fundraising News

Apollo closed its $6.5 billion Hybrid Value Fund III. The fund sits between traditional debt and equity, investing mainly in structured equity, preferred securities, and convertibles, and providing capital solutions for growth, acquisitions, shareholder liquidity, and balance sheet optimisation. Link

Infranity, a Paris-based infrastructure investor, raised $2.7 billion for its Enhanced Return Debt Fund. Fifty percent of the fund’s capital will be directed towards climate solutions, with a focus on renewable energy and low carbon energy transition projects, as well as essential digital and social infrastructure. ERDF provides senior secured sub-investment-grade loans. The Article 8 fund targets an 8.5-9 percent gross IRR. More here

S3 Capital, a New York-based private construction lender, closed its $1.3 billion Credit Fund III. The fund targets first-lien construction lending, primarily financing multifamily residential developments in supply-constrained US markets, and is expected to support approximately $4.3 billion of loan originations. More here

Flexpoint Ford, a Chicago-based financial services investor, raised $1.1 billion for its Asset Opportunity Fund III and Insurance Opportunity Fund I. More here

Audax Private Debt, a New York-based manager, closed its $1 billion private credit continuation vehicle led and structured by Pantheon. The vehicle relates to Audax’s 2018-vintage direct lending fund. More here

LibreMax Capital, a New York-based asset-backed manager, launched its first interval fund with $885 million of commitments. The fund invests in private asset-backed finance and traded structured credit backed by consumer, housing and commercial receivables, and offers daily subscriptions with quarterly liquidity through repurchases.

Corbin Capital Partners, a New York-based alternative asset manager, closed its first dedicated litigation finance fund with $342 million of commitments. The fund will finance commercial litigation, including business disputes, antitrust, mass torts, bankruptcy-related litigation, and intellectual property claims. More here

This newsletter is for educational and entertainment purposes only. It should not be taken as investment advice.