Partners Group: Separating Headlines from Reality

Fundraisings from Bridgepoint, Pemberton, Oaktree and AHL Ventures.

👋 Hey, Nick here. A big welcome to the new subscribers from S3 Capital, Aperture Investors and BlackRock. You’re now part of a select group of 3,043 subscribers. This is the 169th edition of my private credit newsletter.

If you’re reading this on Outlook, most of the graphs won’t show. I’d recommend you read it online

📕 Reads of the Week

Market Updates

Chicago Fed: Private equity-backed life insurers are fueling private credit.

While life insurers have long provided this form of private credit, private placements lending increased from $386 billion in 2014 to $849 billion in 2024.

In relative terms, private placements accounted for 14 percent of life insurers’ general account assets in 2024, up from 10 percent in 2014

Life Insurance PE-owned life insurers more than doubled their annuity market share from 8.5% to 18% and their indexed annuity market share from 16% to 33%.

PGIM: Headlines vs. Health. Link

Carlyle: Q2 Global Private Markets Quarterly. Link

PWC: Private Credit Survey. Link

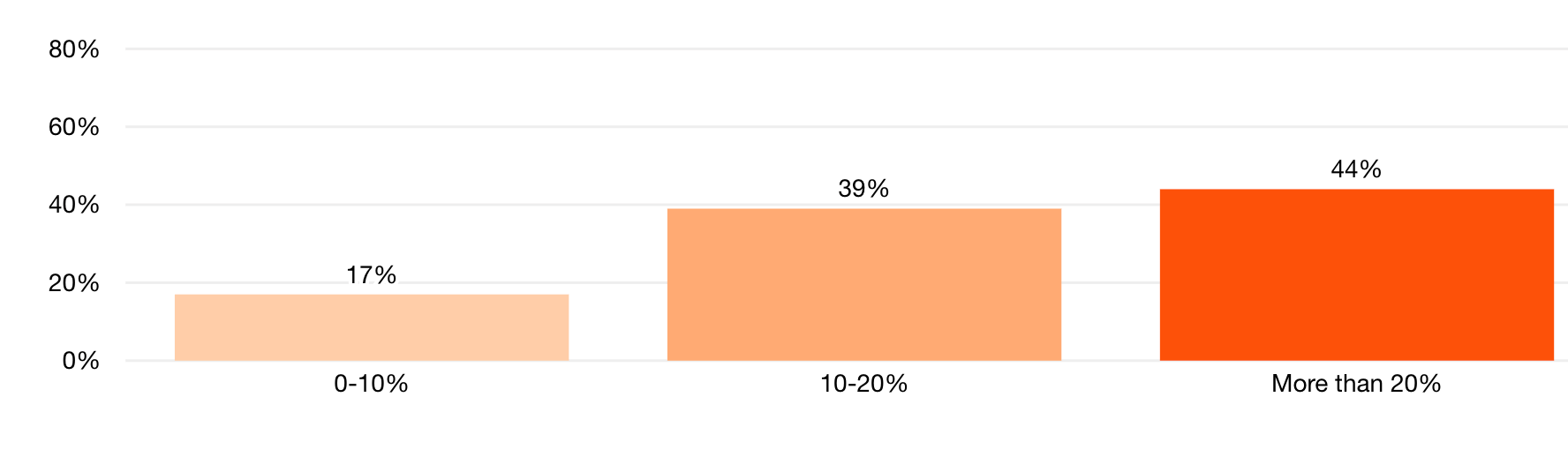

How much do you expect your allocation to private credit to change?

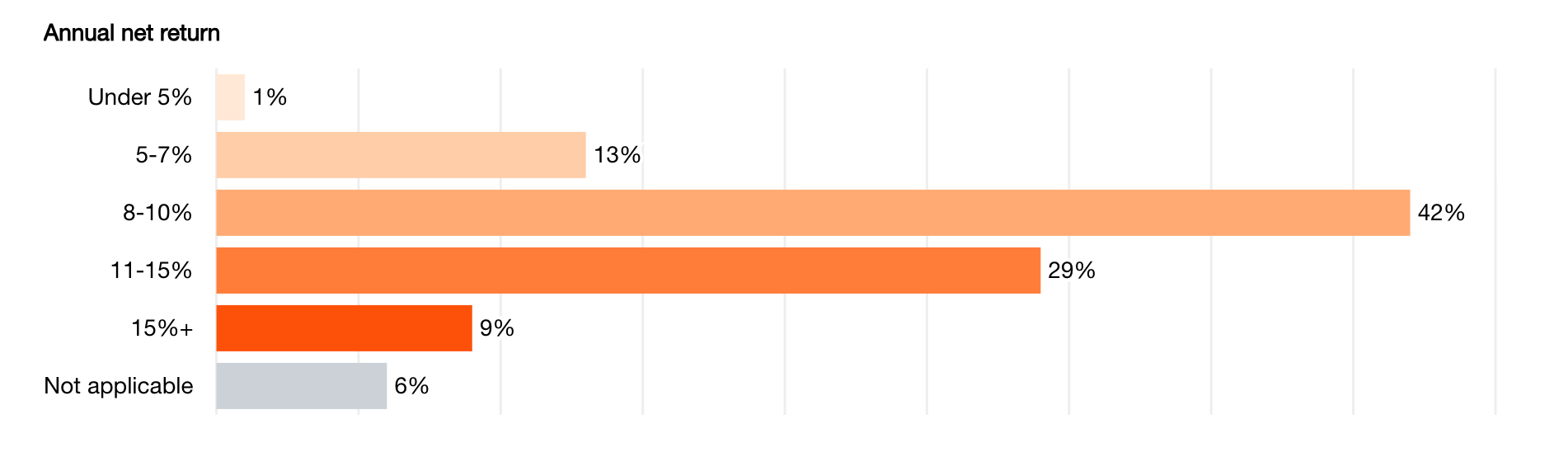

What IRR are you targeting on an unlevered basis?

BDC Redemptions: It’s the Boulders, Not the Pebbles

Jon Gray spoke about BDC redemptions a few weeks ago:

“Contrary to this popular idea that it is small investors leading the charge, it is actually a smaller number of large investors who are double the size, on average, of the typical account in these vehicles… It is the bigger boulders, as opposed to the pebbles, where you get more movement in terms of redemptions”

This week we saw a clear example of this:

Bloomberg reported that Vista Credit was enforcing its 5% quarterly withdrawal limit after Partners Capital redeemed 30% of its shares. Partners Capital is a significant shareholder in the vehicle owning about 18% of the fund at year-end.

The Swiss pension investor reportedly entered the $1.9bn BDC late last year and received bonus shares as part of a promotional allocation. It subsequently moved to redeem those bonus shares shortly after issuance, a step that surprised the fund, according to the source.

This is the point Jon Gray was making.

The liquidity risk in these vehicles may not come from thousands of small investors changing their minds. It may come from a much smaller number of large shareholders whose decisions are big enough to move the whole vehicle.

In other words, it’s the boulders, not the pebbles.

Data Centers and AI

Apollo and Blackstone are structuring a $36 billion package financing AI for Anthropic, in one of the largest transactions of its kind:

The financing is designed to enable Anthropic to acquire Google’s tensor processing units (TPUs), which will then be leased back to the Anthropic for use across its expanding compute footprint.

Broadcom is expected to provide a form of residual value guarantee on the underlying hardware.

The financing will be divided into multiple tranches with Apollo and Blackstone syndicating portions of the debt to other institutional investors while retaining meaningful stakes themselves.

Blue Owl: Inside a Data Center. Link

Brookfield: Opportunity in a constrained market. Link

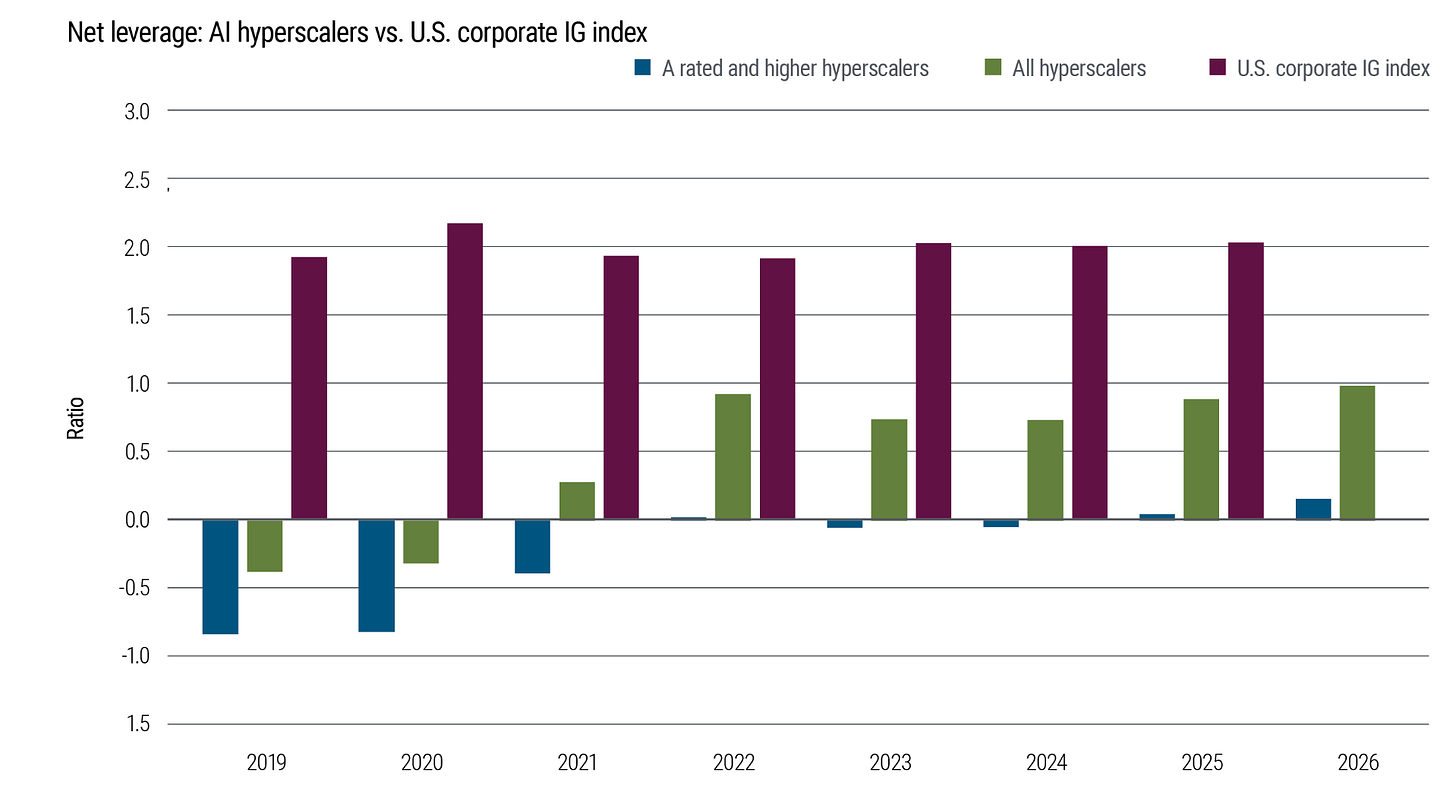

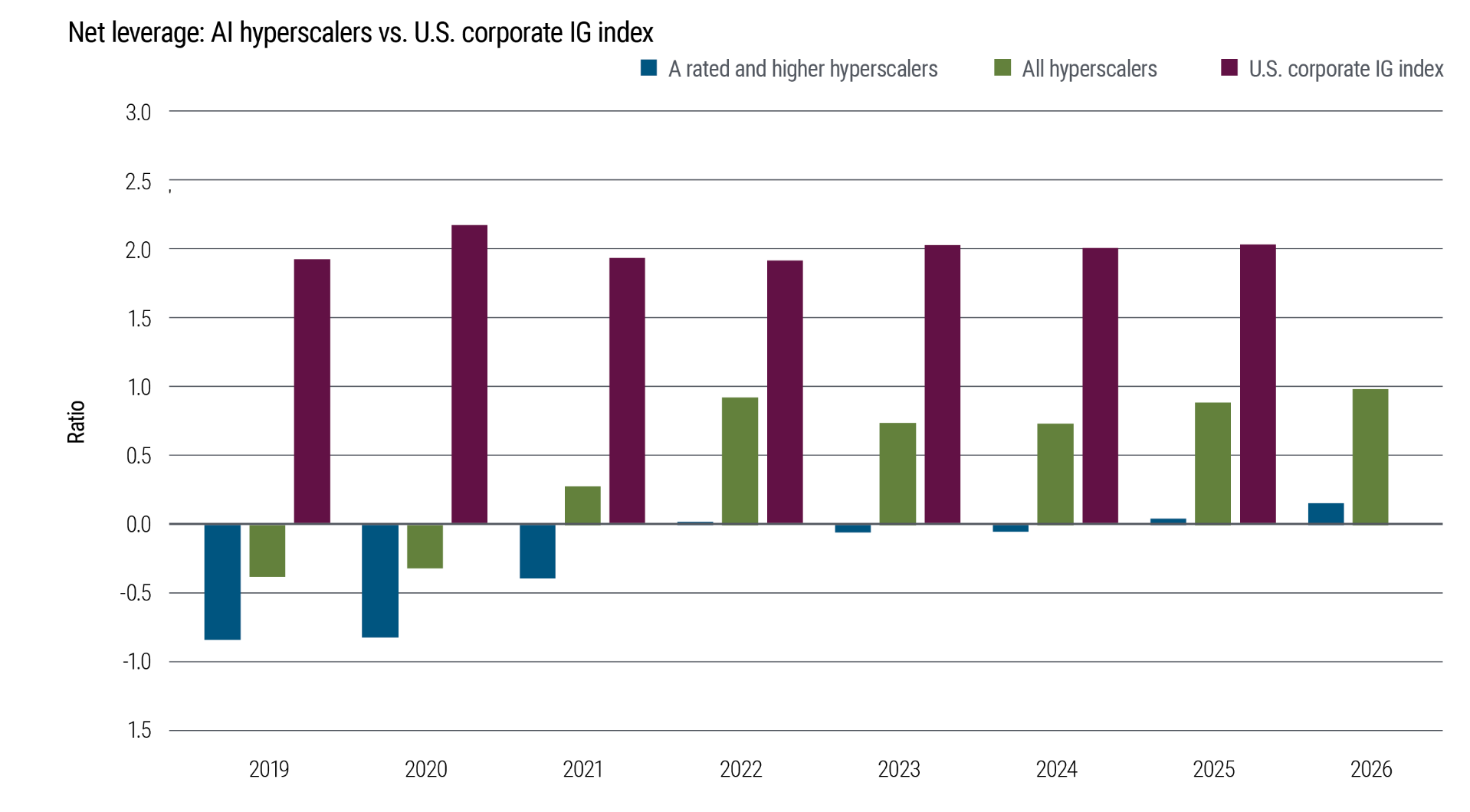

PIMCO: A-rated and higher hyperscalers have plenty of debt capacity. Link

BDC Updates

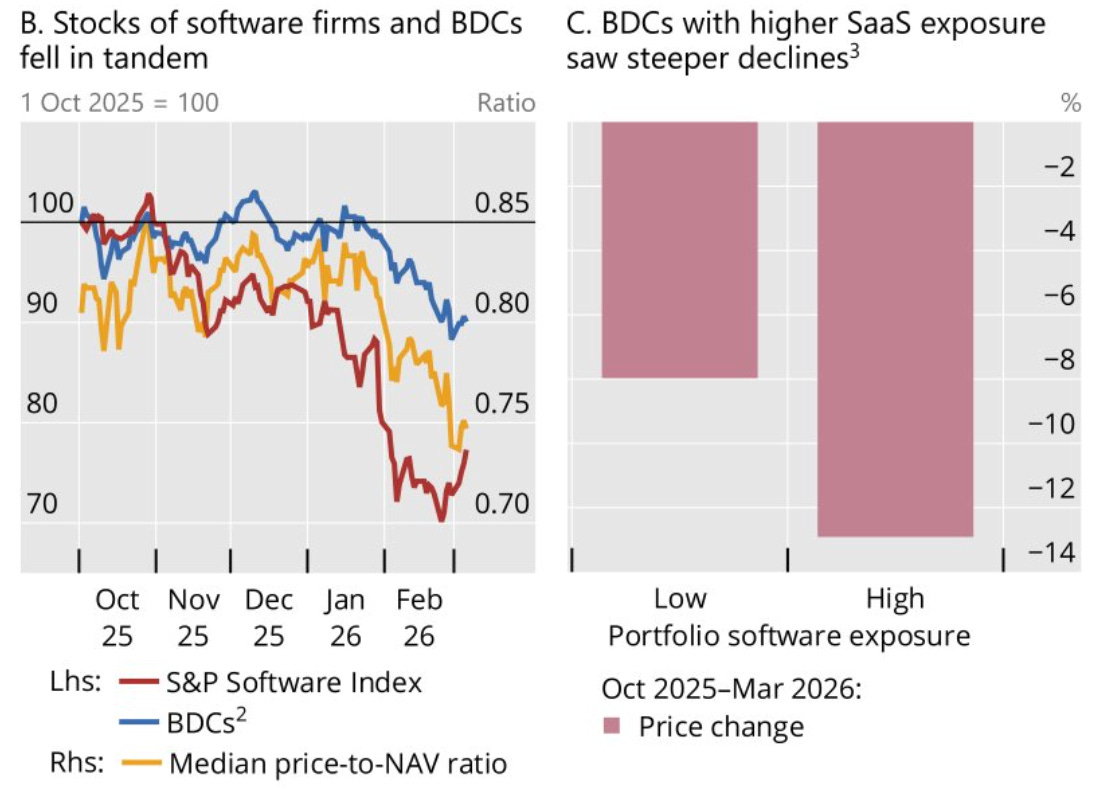

BDCs with higher SaaS exposure have underperformed their peers. Link

Partnership Updates

TD Bank, the 10th-largest commercial bank in the US by assets, is looking to partner with private credit managers. Link

Investec, the UK-based bank, and Sequoia Investment Management Company, a global private credit manager dedicated to infrastructure, partnered to finance UK and European energy and infrastructure. Link

Restructuring

Ares and MetLife disagree over the restructuring of Eagle Football debt. Link

Blackstone and KKR to assume control of the dental group Affordable Care. Affordable Care was valued at $2.7bn when Harvest Partners acquired its stake in 2021. Link

🏌 Jon Gray Interviews Tommy Fleetwood. Link

Partners Group: Separating Headlines from Reality

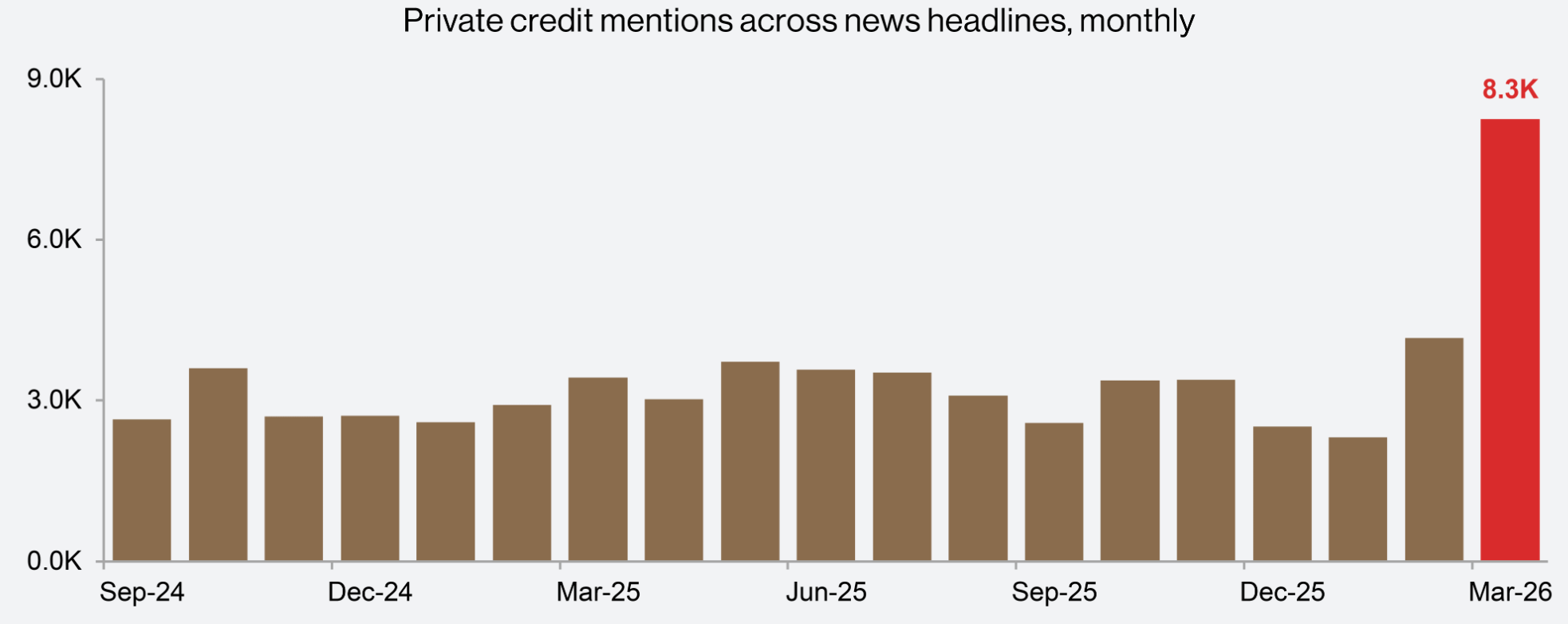

Private Credit Headlines Have Surged

While headlines warrant attention, they often overstate the near-term implications and underappreciate the underlying resilience in both current fundamentals and the macro backdrop.

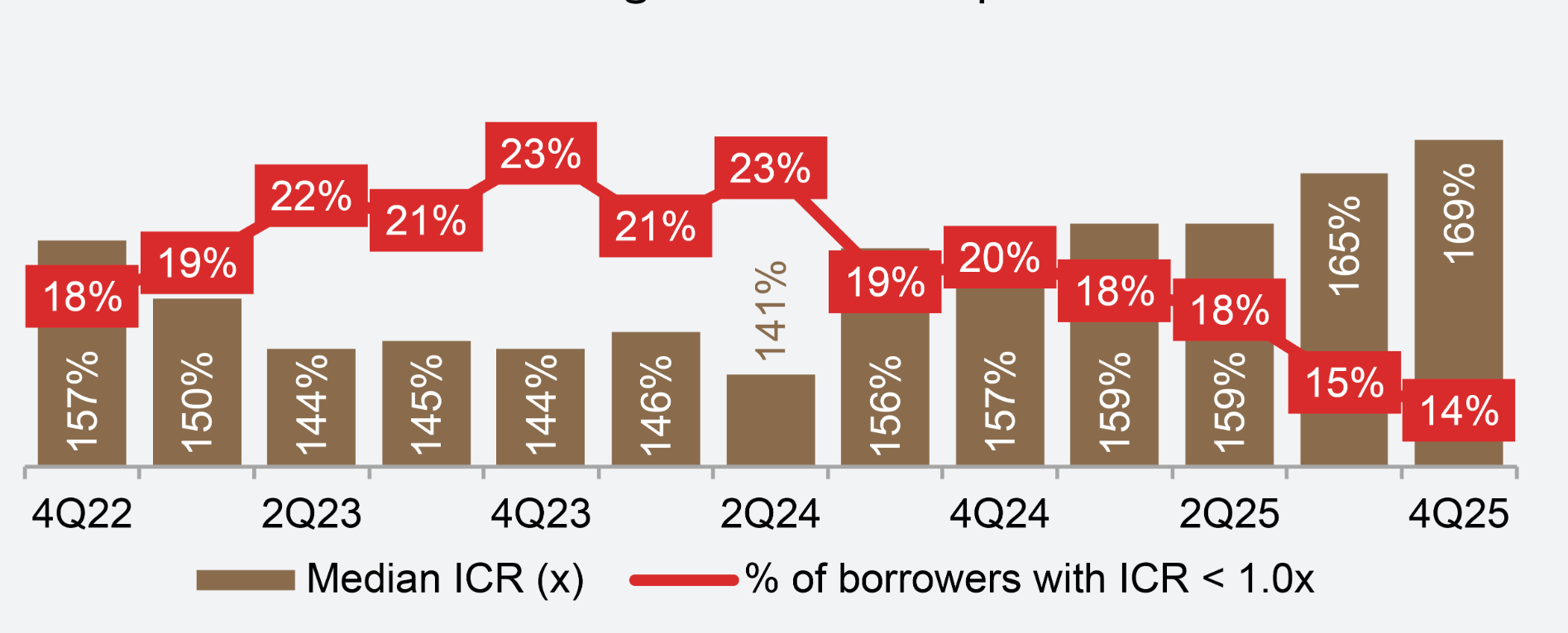

Coverage Ratios Show Resilient Fundamentals

Interest coverage ratios have improved from mid-2024 lows, supported by lower policy rates and healthy EBITDA growth. Sub 1.0x borrowers have declined materially, falling to 14% in Q4 2025 from 21-23% throughout 2023 and early 2024.

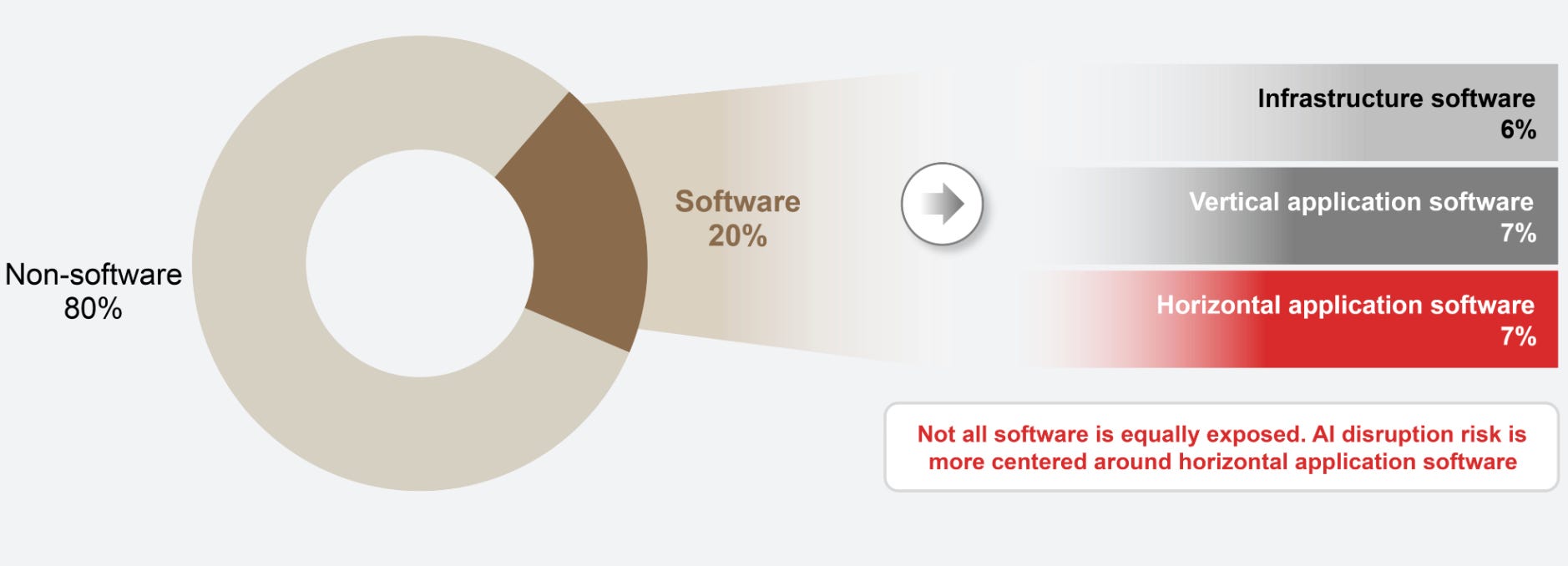

Not All Software Is Equal

Incumbents with strong moats, proprietary data, AI-enabled workflows, and exposure to regulated or mission-critical end markets are better positioned to sustain value and drive efficiency gains. These are typically found in infrastructure and vertical application software.

By contrast, more vulnerable software tends to be rules-based, repetitive, and often tied to functions like customer service or project management. This exposure largely sits within horizontal application software, which accounts for around 35% of total software exposure within the U.S. direct lending market.

This real at-risk exposure is just 7%, well below the 20% headline figure.

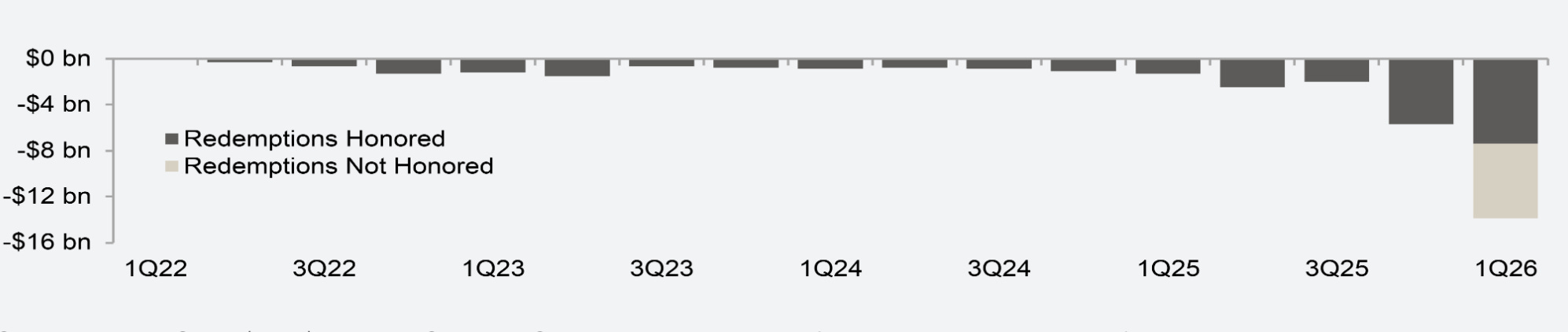

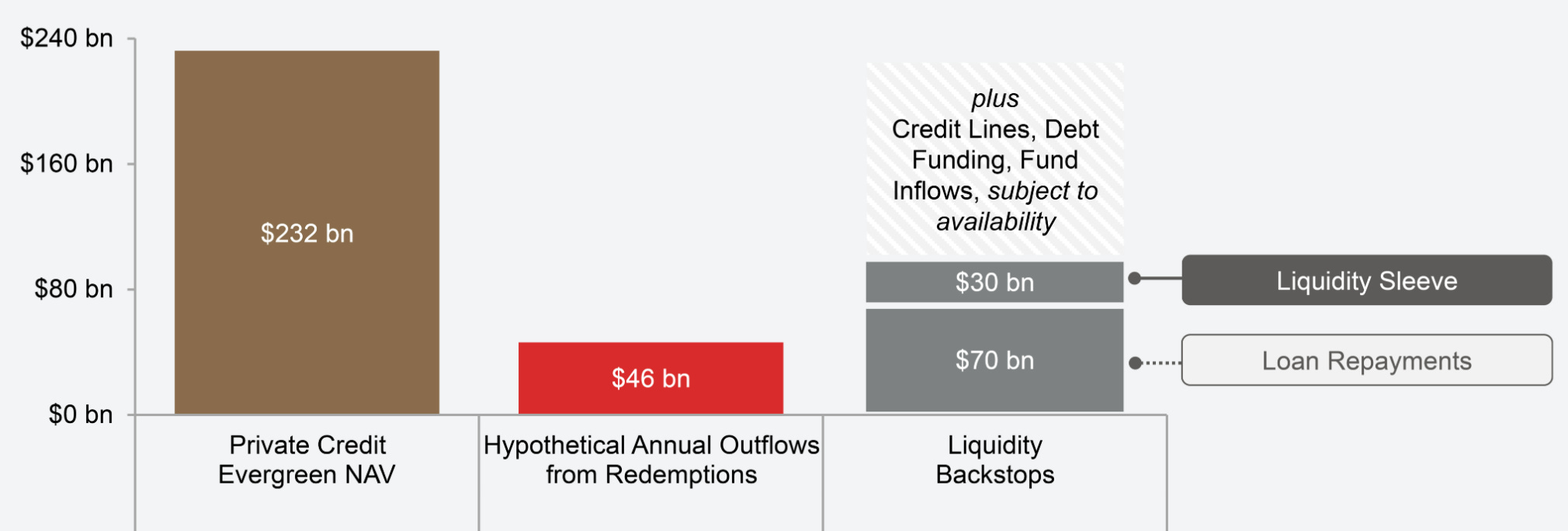

Q1 Redemptions were five times above the prior four-quarter average

Redemption caps are a feature, not a flaw.

Most vehicles can meet redemptions at stated limits for at least the next 4-5 quarters, supported by multiple levers, including loan turnover of around 25-30% annually, liquidity sleeves of 10-15% in cash and liquid credit, and access to debt and bank credit lines.

The more important story is one of transition.

For much of the past decade, the dominant strategy was straightforward: build a diversified portfolio, apply leverage, and collect spread. That approach worked well in a benign default environment.

Partners Group thinks this will be harder to replicate going forward:

Private credit is now entering a new normal defined by greater bifurcation and wider dispersion of returns.

In a more differentiated market, selectivity becomes the primary driver of returns.

It is against this backdrop that we assess the current private credit fundamentals, separate headlines from reality, and offer a path forward for earning returns in private credit.

As an example:

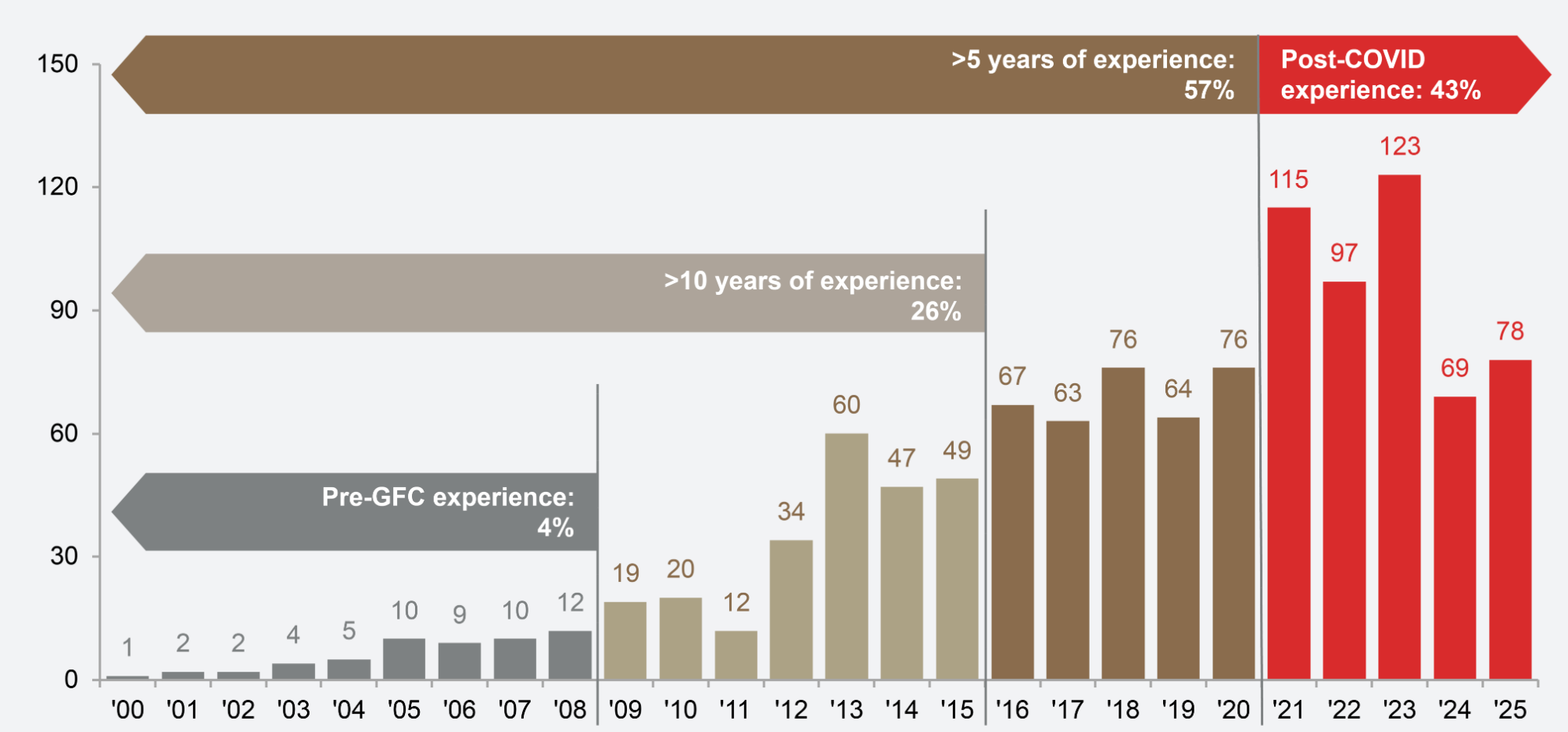

Two thirds of managers have less than 10 years experience

With nearly half of direct lending managers formed post-COVID and close to 70% established within the past decade, many have yet to be tested through a full cycle – suggesting differentiation across managers is likely to increase further.

💰Fundraising News

Bridgepoint, the London-based manager, is closing its $5.8 billion European direct lending fund IV. The fund finances sponsored European middle-market businesses. The fund is nearly 50% larger than its predecessor fund, which closed at €3.4 billion. Link

Pemberton, a London-based private credit manager, closed its $4 billion Strategic Capital IV fund. Launched in 2017, the opportunistic strategy invests in performing companies across Europe. More here

Oaktree partnered with Pantheon to scale its European Direct Lending with a target to deploy up to $1.2 billion. Pantheon will provide additional capital alongside Oaktree’s existing portfolio of seeded investments, supporting a strategy focused on senior secured, first-lien loans to corporates across Europe and the UK. More here

AHL Ventures, a Kenyan-based manager, announced a first close of $30.5 million for its debut institutional credit fund. The fund lends to African businesses, with a focus on financial inclusion, climate-related businesses, and agriculture. It can invest across the capital, providing senior secured, mezzanine and bridge loans. AHL continues to raise additional capital toward a targeted final close in Q1 2027. More here

This newsletter is for educational and entertainment purposes only. It should not be taken as investment advice.