Sixth Street: Investors in our industry have two choices, the “what” and the “when”.

This newsletter is for educational and entertainment purposes only. It should not be taken as investment advice.

👋 Hey, Nick here. A big welcome to the new subscribers from KV Capital, TMT Capital, and Moody’s. You’re now part of a select group of 2,711 subscribers. This is the 159th edition of my weekly newsletter.

If you’re reading this on Outlook, most of the graphs won’t show. I’d recommend you read it online

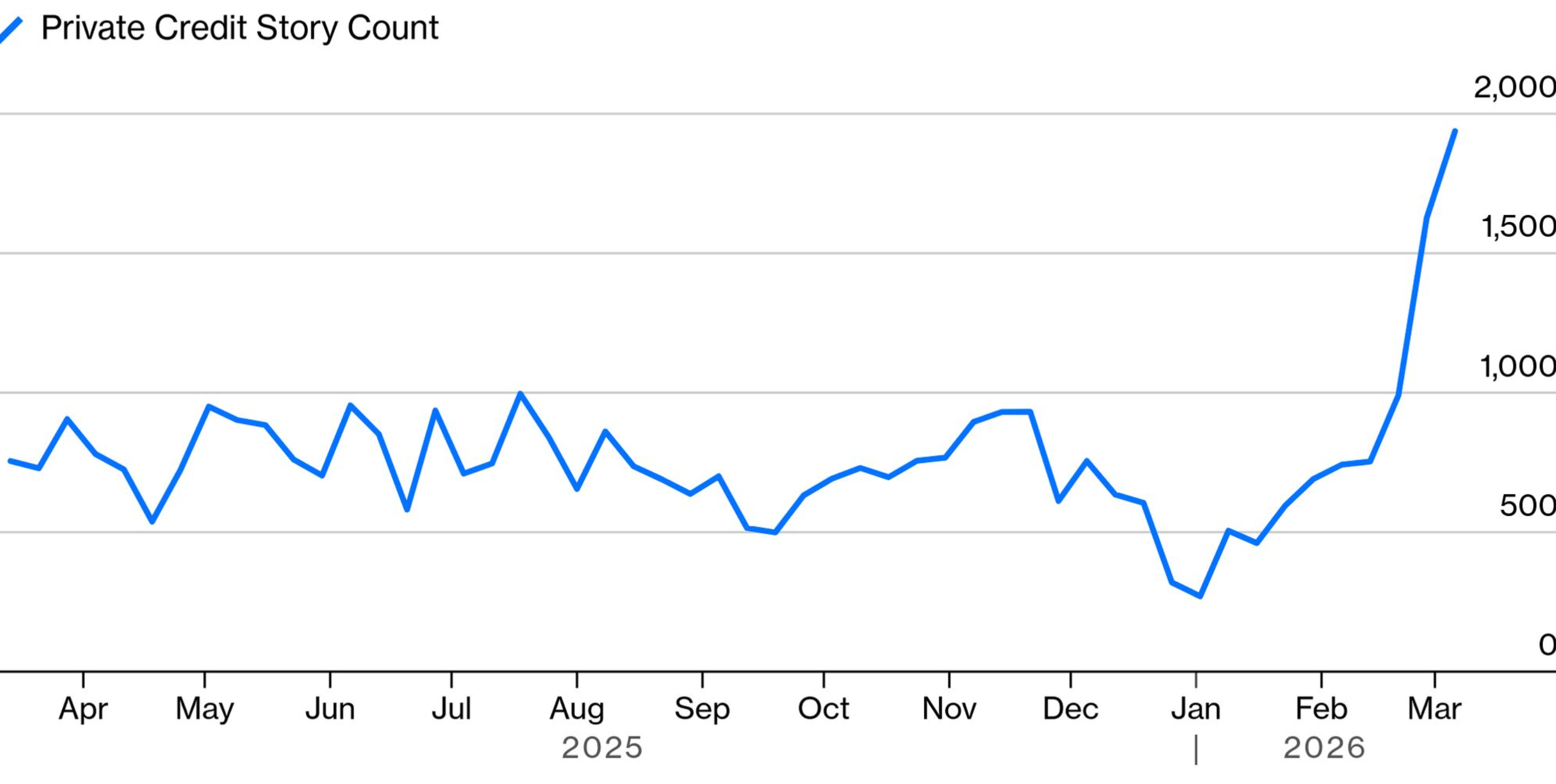

Private credit coverage surged to its highest level in March

What’s frustrated me most is how relentlessly clickbait the coverage has become, even when the underlying data has been broadly sound.

The pattern is always the same. A dramatic headline, a rush of commentary, and a far less dramatic reality underneath.

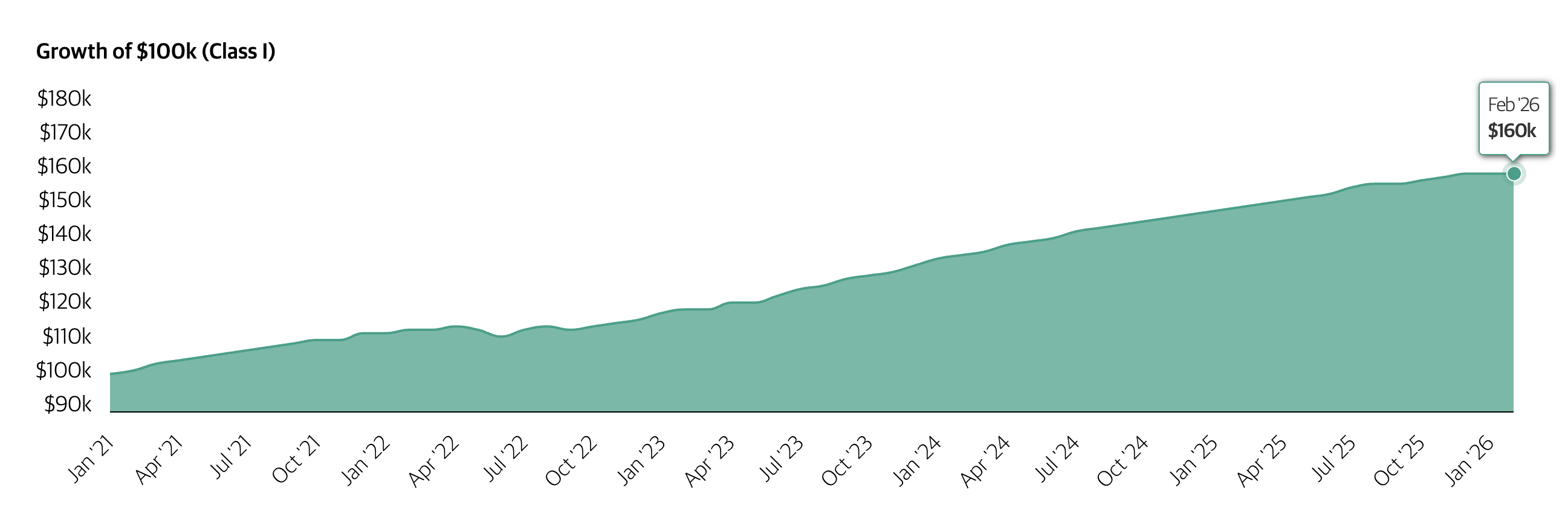

Exhibit 1: BCRED’s monthly loss

Flagship Blackstone credit fund posts first monthly loss since 2022

Financial Times | 2 days ago

Blackstone Private Credit Fund Has First Monthly Loss Since 2022

Bloomberg | 2 days ago

A lot of people sent me this story. But behind the headline, BCRED’s monthly total return was down just 0.4% last month.

I will repeat that, all of this noise was about a 0.4% decline.

Put differently, if you invested $100,000 in January 2021, you would still have roughly $160,000 today, despite this drop.

Exhibit 2: Cliffwater’s Negative Outlook

Cliffwater Private Credit Fund’s Outlook Cut to Negative by S&P

Bloomberg | 4 days ago

Press coverage also focused heavily on the negative outlook for Cliffwater’s BDC, particularly the redemptions.

We affirmed the 'A' rating on the fund because it maintains good asset quality, low leverage compared with peers, and satisfactory liquidity despite the wave of investor redemptions in the first quarter.

The nonaccrual loan rate has barely ticked up from last year and is well below 100 basis points.

Exhibit 3: Bank of America Shorts European Private Credit

BofA pitches bets against European private credit

Financial Times | 3 days ago

The media also seized on Bank of America’s call on European private credit.

But the very next day, BofA withdrew the recommendation and apologized for “factual inaccuracies”.

What has struck me most in all of this is the number of smart, informed people who have been drawn into debating these stories.

Private credit’s biggest danger may not be that the asset class is collapsing. It may be that enough people start to believe it is

📕 Reads of the Week

Market Updates

Covenant Lite: What software investors can learn from the 2014 energy collapse. Link ***Recommended***

Pimco analyses private credit’s illiquidity premium. The absence of continuous, mark‑to‑market pricing in private assets should not be viewed as a structural flaw. Rather, it reflects a distinct risk profile, one for which investors must be explicitly and adequately compensated. Link

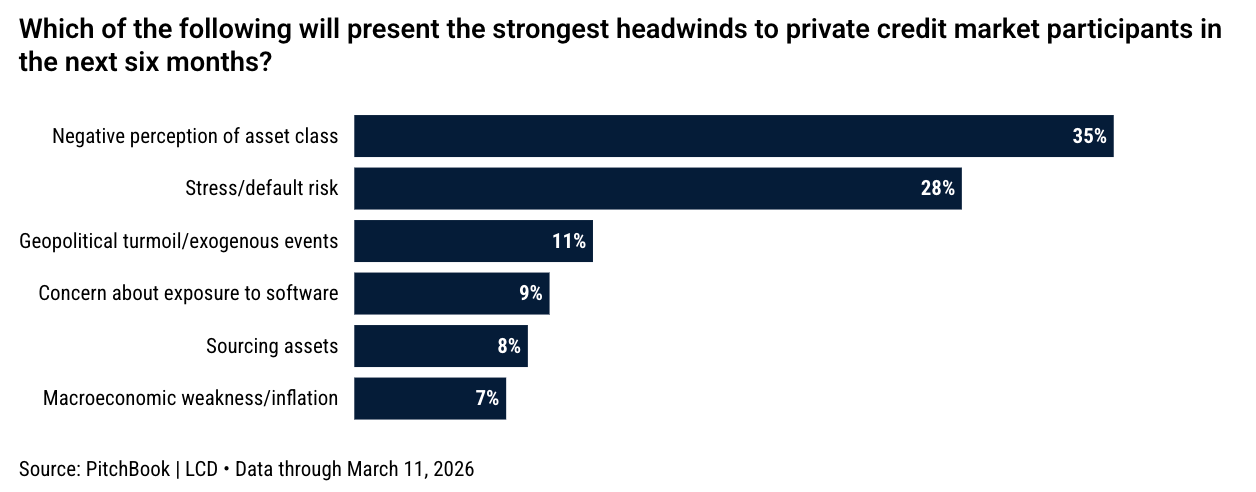

LCD’s Q1 Global Private Credit Survey. Link

Ultimately, convergence of public and private debt is the direction of travel. This will give LPs even more comfort as they increasingly access a broader opportunity set in private credit but still want portfolio flexibility and lower volatility

Manager Updates

Emerging managers to watch in 2026. Link

Franklin Templeton launched a new target-date fund for 401(k) investors that includes a private market allocation. The fund allocates between 2% and 8% to private markets along the glide path. The private credit allocation will be implemented through the Franklin BSP Lending Fund. Link

JPMorgan and Goldman provide hedge funds with tools to short private credit. Link

BDC / Interval Fund Updates

Oak Hill Advisors is launching a new interval fund, OFLEX, designed to deploy capital across public and private credit markets. The fund will target a spectrum of credit opportunities, including direct lending, asset-backed finance, collateralised loan obligations, public credit, and special situations. Link

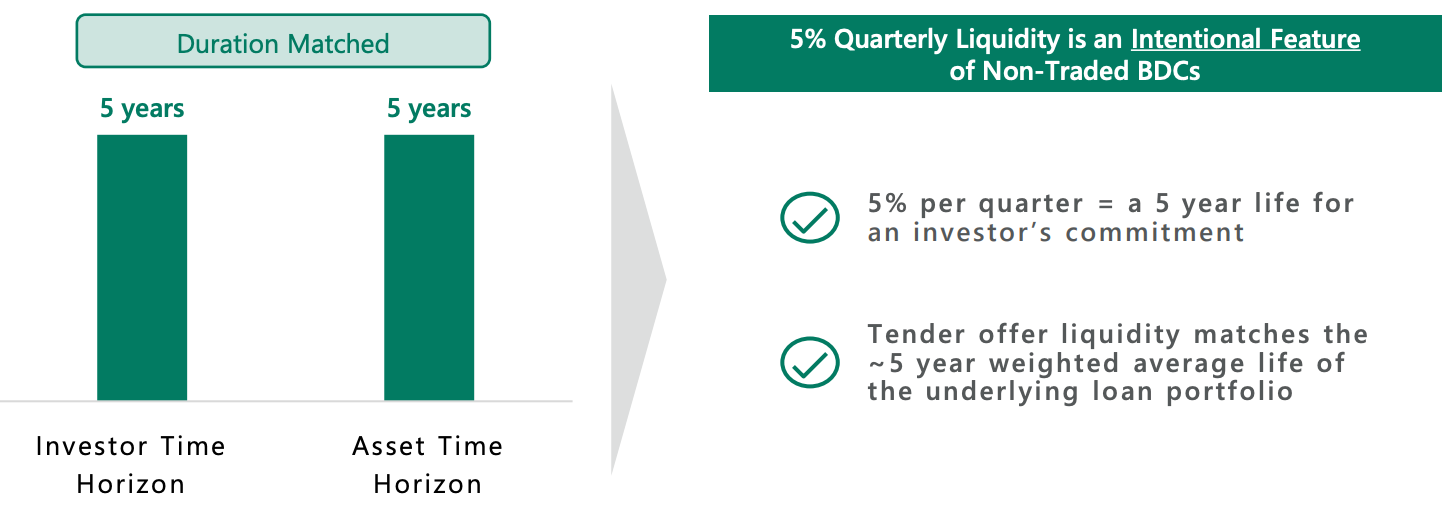

Apollo Debt Solutions received redemption requests for 11.2% of shares. The fund will pay out the quarterly 5% repurchase cap. Link

The ADS portfolio is ~100% first lien – the highest of its peers, with limited PIK income (approximately 2.5%), average position sizes of 0.2% and weighted average loan-to-value of 41%.

ADS has $5.3 billion of immediately available liquidity,15 representing ~7 quarters of coverage versus estimated first quarter 2026 redemptions

Sixth Street: Investors in our industry have two choices, the “what” and the “when”.

If you want a blunt view of what is happening in private credit, Sixth Street’s letter is worth a read. Below are my highlights.

During periods of elevated volatility, it can sometimes be difficult to separate factual conclusions from emotions like exuberance and fear. But as investors, our job is to be aware of and discern the differences between the two.

From redemptions in the perpetual non-traded sector to the AI hype cycle to whatever comes next, our focus remains on the fundamentals. AI is a world-changing technology, but sentiment is leaving little room for nuance.

The current market discourse is conflating equity valuation volatility with fundamental credit risk.

Beneath what is grabbing today’s fearful headlines is the fact that over the past few years exuberance outran facts regarding BDC unit economics. The lack of disciplined risk management on the liability side of the business, specifically the shift towards gathering client funds intended to be immediately deployed rather than patiently invested, has led to structural underearning and looser protections on assets across the sector.

The result is what we see today: a BDC sector going through an intense yet warranted reset.

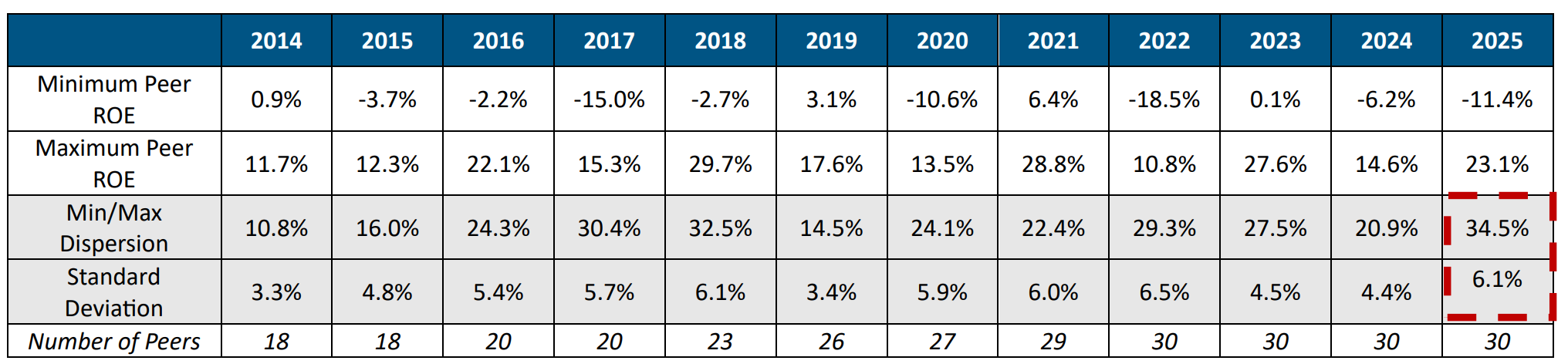

The dispersion between the minimum and maximum ROE is the widest we have seen.

Zooming out across the broader BDC sector, we believe most of the issues the industry is facing today result from structural risk management failures pertaining to liquidity and capital frameworks. Over the past several years, new vehicles designed with incentives that sacrificed robust capital and liquidity guardrails in favor of short-term asset gathering were introduced and proliferated, targeted at a largely retail client base with which the industry has shallower relationships compared to the institutional investors that initially funded the sector.

Investors in our industry have two choices, the “what” and the “when”.

Vehicles built on perpetual retail flows are vastly limited in both choices as retail capital ebbs and flows. You are limited on the “when”, because dollars that come in need to be put to work right away, and the “what” is therefore determined in large part by what is on the menu at that time. In addition, there is wrong way risk as it relates to flows. Flow levels tend to be the largest when risk premiums are at all time tights. You only have to look at 2024 and the Q1 2025 collapse in private market spreads. During “risk off” periods, when risk premiums are attractive, both capital and liquidity leave the system. This is wrong-way risk for both the capital and manager (as there is a promise and an expectation of liquidity, even if the fine print includes redemption gating provisions). These risks are borne by all shareholders.

Dividend cuts have nothing to do with credit losses

When you combine base rates of approximately 350 basis points today with new investment spreads that have dipped below 500 basis points, the resulting ROEs, even before accounting for credit losses, fall below both the industry’s current estimated cost of capital and the returns that were promised to investors.

To be clear, the dividend cuts that have started to proliferate across the BDC sector over the past few quarters have nothing to do with credit losses. The loss rates for private credit have been relatively stable. But the math will tell you the sector cannot fund current dividends at the spreads at which it has been deploying capital.

Given the overwhelming bulk of BDC assets are floating rate in nature, movement in dividend levels over time – both up and down – should not be surprising on its own. Post-COVID, as we moved into a pronounced rate rise cycle, asset level returns increased, leading to higher payout levels through increased dividends. Similarly, as we have seen reference rates decline from the peak last seen in mid-2023, the notion of lowering dividend levels should be in part a logical and expected outcome.

But it has been the combination of lower reference rates (largely a non-controllable factor for BDC managers absent negotiating for high floors), together with a deployment objective that prioritized capital out the door rather than return on equity, that has led to returns across the sector falling below the equity cost of capital threshold.

Due to a combination of headline-driven fear and weaker performance math, investor trust in direct lending has been damaged.

Liquidity is being taken wherever it can be found, leading public BDCs to trade down and perpetual non-traded BDCs to wrestle with whether to exercise gating provisions

“Crises don’t happen because of credit issues, they happen because of liquidity issues.”

Sixth Street’s co-founder and CEO Alan Waxman.

History tells us that once trust cracks and liquidity is impaired, that cycle is difficult to quickly reverse.

If you believe in efficient markets, public BDCs trading at significant discounts versus similar private counterparts is an arbitrage that will resolve over time. Capital will be reallocated, and the public BDC sector should benefit as the liquidity-taking abates and discounts normalize.

The rebalancing of the ecosystem will take time to fully materialize, but it should ultimately result in the widening of new origination spreads and a healthy recalibration of the supply-demand dynamic for private capital.

In periods of significant redemptions, inflows tend to decline significantly.

As we witnessed during the redemption cycle that impacted non-traded REITs in 2022, flows are typically correlated in the sense that in periods of significant redemptions, inflows tend to decline significantly.

That is what we are now seeing in the non-traded BDC market. Utilizing liquidity for redemption activity (e.g., holding a liquidity sleeve in broadly syndicated loans) will, by definition, drive lower returns for non-traded vehicles; lower returns will result in increased capital flows to better relative return opportunities in other sectors of the market. We do not believe this environment will reverse in one quarter. If the non-traded REIT segment is any guide, this capital flow dynamic will last multiple years.

While some may believe today’s volatility is only a minor episode to be weathered, we believe there is going to be an honest reckoning for the sector resulting in a healthier and more resilient direct lending industry

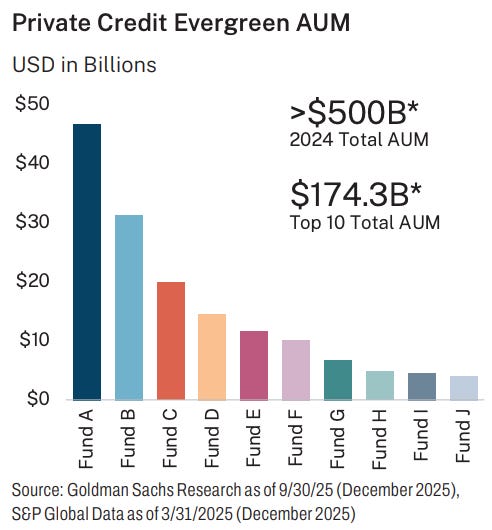

Hamilton Lane: Evergreen’s will dominate private credit

👉 Hamilton Lane: Evergreen’s will Dominate

The evergreen world has gone from, effectively, $0 to $500 billion in the last decade. And the top managers are vacuuming up impressive sums: The largest evergreen fund’s NAV exceeds the combined NAV of the five largest closed-end funds raised in 2024.

The credit fundraising market will increasingly be dominated by evergreen vehicles.

Will larger institutions embrace that form of investment for their credit portfolios?

They already are.

The growth in the size of the private credit market, together with the growth of the evergreen channels, will result in a small group of very large managers.

If you are not a major player in that space now or in the very near future, you will not have a meaningful private credit franchise. You might have a meaningful niche strategy or place in the market, but scale will increasingly matter in the credit space.

👉 Hamilton Lane: Evergreen’s will Dominate

💰Fundraising News

Goldman Sachs Asset Management is planning to raise $13 billion for its latest mezzanine debt fund, GS Mezzanine Partners IX. The fund invests in sponsored companies across North America and Europe. The fund will target net returns of 11%–13% using leverage, or 8%–9% on an unleveraged basis. More here

Orion Resource Partners, a New York-based manager, closed its $2.2 billion Mine Finance Fund IV. The fund finances the construction and acquisition of strategic metals and critical mineral assets. The fund is already 61% committed across a portfolio of projects, spanning North and South America, Europe, Australasia, and Africa. More here

Lone Star, a US-based manager, closed its $1 billion Residential Mortgage Fund IV. The fund invests in newly originated, performing U.S. non-agency mortgage loans. Non-agency borrowers generally include self-employed individuals and small business owners who do not have access to traditional agency and government-backed mortgages, despite often having strong credit profiles. With leverage, the fund is able to invest in over $10 billion of mortgage loans. More here

EOS Investors, a US-based real estate firm, announced a first close of $150 million for its inaugural hotel credit strategy. The strategy will focus on senior whole loans, mezzanine financing, and structured debt opportunities in the hospitality sector. More here

Walton Global, a US real estate manager, launched its U.S. Land Income & Growth Fund for offshore investors. The hybrid strategy provides senior secured loans to large national U.S. homebuilders. At the same time, the fund acquires pre-development residential land in U.S. metropolitan areas characterized by population growth, housing undersupply, and sustained homebuilder demand. More here

This newsletter is for educational and entertainment purposes only. It should not be taken as investment advice.