Sona's Honest Assessment of Private Credit

Sona steps back from the noise to address the issues it believes matter most

👋 Hey, Nick here. A big welcome to the new subscribers from Canada Life, Castlelake and Avenue Capital. You’re now part of a select group of 2,879 subscribers. This is the 164th edition of my private credit newsletter.

If you’re reading this on Outlook, most of the graphs won’t show. I’d recommend you read it online

📕 Reads of the Week

Market Updates

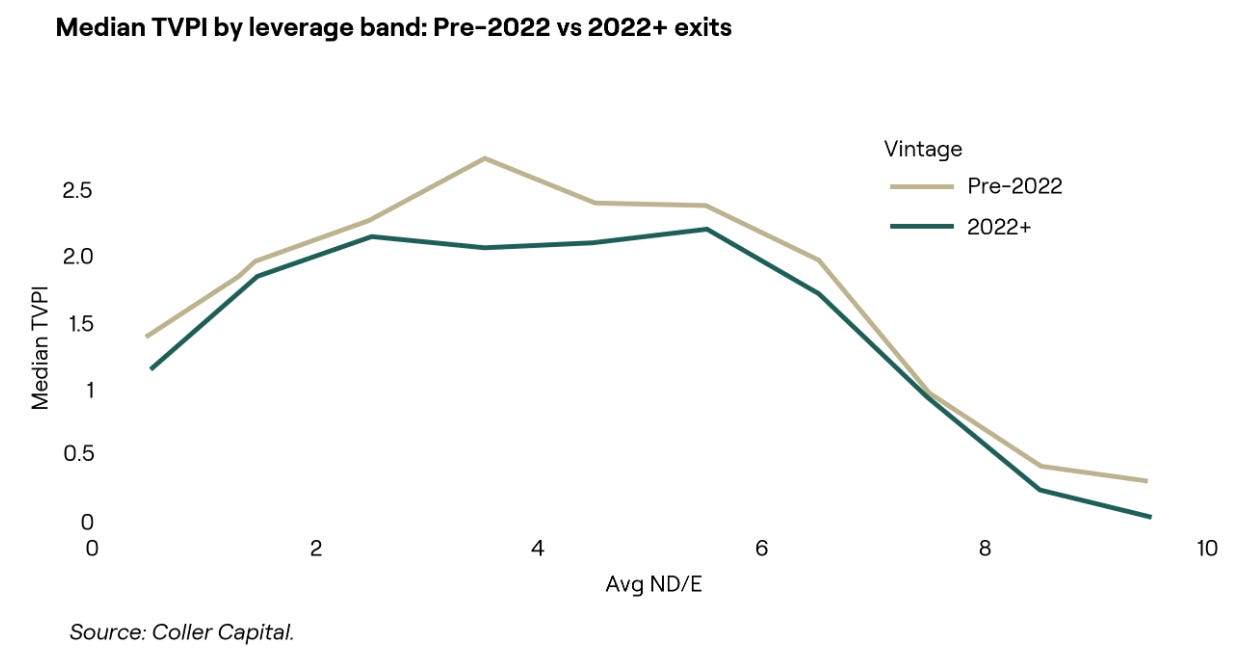

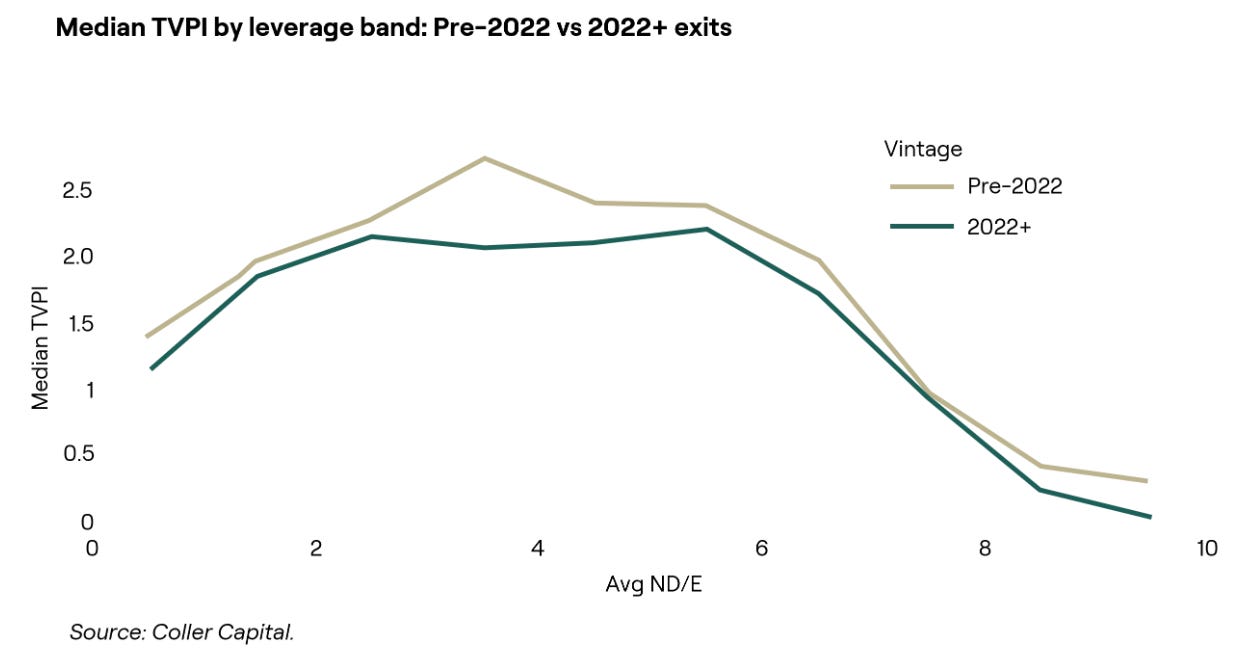

Coller Capital: Why Debt Levels Matter for Secondary Underwriting.

Coller analysed 1,789 PE exits to find out.

Loss rates rise to more than 30% when leverage increases more than 6x.

FT: Private credit won’t spark the next financial crisis. Link

Goldman Sachs: Taking the long term view on private credit. Link

Pemberton: Insights into European Private Credit. Link

Ares: Secondaries Take the Spotlight. Link

Scott Humber, a Partner at Ares Management.

Partnership Updates

KKR and Capital Group are launching a public–private credit fund in Asia later this year. Link

MUFG is looking for partners to share risk. The bank is aiming to limit funding through its own balance sheet so as not to bear the risk of financing deals as a wave of leveraged buyouts sweeps Japanese firms. Link

Manager Updates

The Big Picture: Outlook from the Co-CEOs at Oaktree Conference 2026. Link

Saba Capital to raise $1 billion to buy souring private credit funds. Link

Pimco has lent more than $10 billion to state-backed and government borrowers in the Gulf, since the conflict began on Feb. 28. Link

Lenders taking the keys on Medallia. Link

BDC / Interval Fund Updates

Private credit BDCs trade at the deepest NAV discounts in over five years. The median listed BDC traded at a discount of 26% to NAV, the steepest gap since October 2020. Link

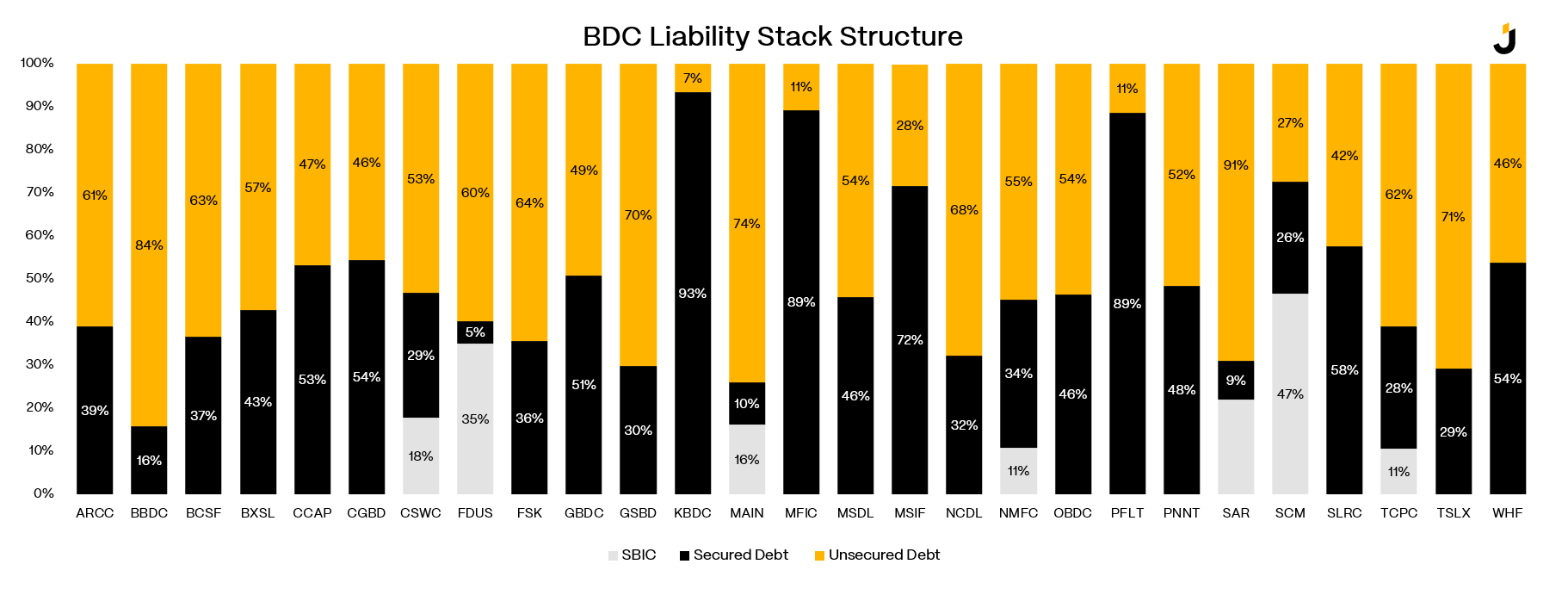

JunkBondInvestor.Not all BDC debt is created equal.

Sona AM: An Honest Assessment

Sona Asset Management’s honest assessment of private credit is well worth a read. I’ve pulled out a few of my favourite lines below.

👉 Read The Full Assessment Here.

Public scrutiny of private credit is now in full force and has almost certainly never been greater. Negative headlines are dominating the narrative: heavy exposure to software companies, redemptions and gating, criticism of portfolio marks, and banks marking down collateral posted by private credit firms.

SEMI-LIQUID STRUCTURES EXIST FOR A REASON

The creation of semi-liquid private credit structures was an innovation which expanded the market. There is no ambiguity as investors allocate to these vehicles with full knowledge of the terms - both on the way in and, critically, on the way out.

None of this makes the current moment comfortable for managers. Each redemption cap risks reinforcing a negative sentiment spiral at a time when the industry is already under scrutiny.

There are also legitimate questions surrounding the handful of managers who have chosen to honour redemptions above the standard 5% threshold - arguably rewarding first-mover behaviour.

Private credit is illiquid. That is known, priced, and agreed upon at the point of commitment. Sudden, large-scale withdrawals would compromise a fund's stability and potentially require premature liquidation of illiquid assets at a loss. Redemption gates are designed to prevent exactly that. They exist to protect the investors who stay just as much as they manage the investors who redeem.

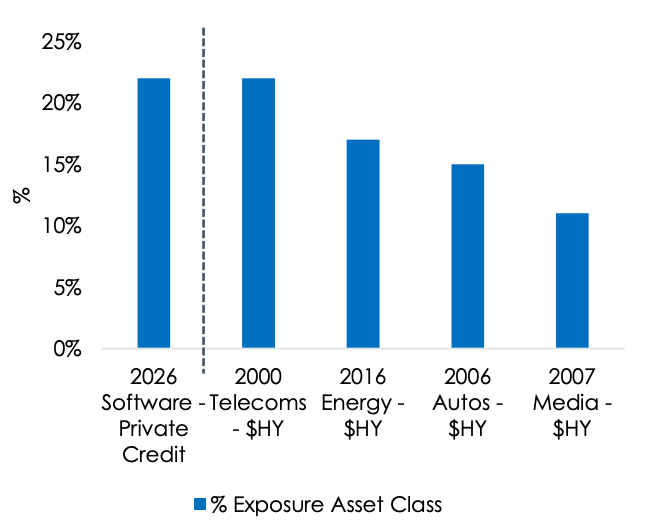

AI AND PRIVATE CREDIT - LIMITED UPDSIDE, REAL DOWNSIDE

Private credit has a serious concentration problem in precisely the sectors AI is targeting most aggressively. Software is the clearest example.

These businesses were seen as predictable cash flow machines, and lenders piled in accordingly. Valuations reflected that enthusiasm, with median deal multiples reaching more than 15x annualised recurring revenue in 2026, layered with substantial debt. Those multiples have since collapsed to around 5x.

Estimates put average software exposure north of 20% of assets, with some funds potentially approaching 40%.

Credit investing is inherently asymmetric. Like equities, the worst outcome is a total loss. Unlike equities, the best outcome is par – investors get their money back plus coupon income. There is no participation in the upside

AN INDUSTRY BUILT TO ORIGINATE, NOT MANAGE.

The private credit industry was designed to originate. Its fee structures, staffing models, GP incentives, and fundraising narratives are all oriented around deployment. The implicit assumption embedded in the business model is that the most important decisions are made at origination and that if underwriting is done correctly, monitoring and management can be largely mechanical.

We believe this assumption is wrong. As a result, many private credit portfolios are not constructed; rather, they emerge as the accumulation of individual deployments.

A genuine portfolio management culture requires continuous reassessment of underlying assumptions. It means regularly asking whether the thesis on which an investment was underwritten remains valid; whether the competitive position of the borrower has changed; and whether covenant levels still reflect the underlying risk. It requires the willingness to mark assets to economic reality, to initiate difficult conversations with sponsors, and - crucially – the willingness and ability to walk away from an investment when circumstances call for it. This doesn’t apply to all managers.

However, there is clear evidence that portfolio management standards have deteriorated in parts of the market.

Why would a well-managed portfolio manager tolerate 40–50% exposure to a single sector – software – that was already showing signs of strain and emerging AI-driven competitive pressure? The answer often lies in incentive structures: managers who deployed capital most aggressively were rewarded with the highest fees and the largest subsequent fundraises.

This contrasts with public markets, where we would argue there is far greater discipline in recognising and exiting a flawed underwriting decision. As the lines between public and private credit increasingly blur, the managers who succeed will be those able not only to originate investments, but also to construct portfolios and actively manage risk - including exiting bad positions when necessary. Experience, or the lack of it, reinforces this problem.

Private credit has long been perceived as operating in a “golden age”, but cycles eventually turn. Managing a concentrated, illiquid portfolio through a credit cycle requires a fundamentally different skill set. The industry has scaled its origination infrastructure dramatically, and portfolio management capabilities, in many cases, have not kept pace.

A FLOOD OF CAPITAL HAS COMPRESSED SPREADS

The most transformative structural development in private credit over the past five years has been the influx of insurance capital, and the implications for the risk-return profile of the asset class have been profound.

According to Barclays, US life insurers’ overall general account investments are $6.1tn. They estimate that the sector’s allocation to private letter ratings – the best proxy for private credit – is about 10% (this includes some rated middle market CLOs and other similar exposures in the alternatives bucket).

Notably, they suggest that private credit assets in the US life insurance industry grew 21% in 2025, about twice the rate of growth of the overall general account.

The problem is not that insurers invest in private credit. Rather, it’s the capital dynamics they introduce. Insurance capital faces permanent deployment pressure - a liability structure that must continuously generate matching assets. This dynamic closely resembles the GP deployment incentive problem described earlier but operates at a scale that dwarfs any individual fund.

The result has been persistent spread compression precisely at a point in the cycle when spreads should be widening to reflect higher risk. Insurance capital has lowered the cost of private credit financing for borrowers at a time when credit quality, documentation standards, and macro uncertainty all point to the need for a greater risk premium.

👉 Read Sona’s Assessment here.

💰Fundraising News

Carlyle reportedly raisied $1.5 billion for its Asset-Backed Income Fund. More here

Ashmore, the London-based specialist emerging markets manager, is working with the European Bank for Reconstruction and Development to develop a $500 million private debt strategy. More here

Founders First Capital Partners, a US early-stage lender, announced a first close of $12 million for Change Catalyst Fund II. The fund invests in growing service-based businesses, generally with $1–10 million in revenue with commercial and government customers. While operating nationally, the fund emphasizes key regions of excellence including California, Illinois, Minnesota, Pennsylvania, New Jersey, New York, and the Washington, D.C. metro area. More here

This newsletter is for educational and entertainment purposes only. It should not be taken as investment advice.