TCW: Looking Beyond Cockroaches and Canaries

A Clearer View of Private Credit

👋 Hey, Nick here. A big welcome to the new subscribers from MEAG, Goldman Sachs, and J.P. Morgan. You’re now part of a select group of 2,497 subscribers. This is the 155th edition of my weekly newsletter.

One favour to ask: if you like this, please share it with a friend. If someone forwarded this to you, you can subscribe here.

If you’re reading this on Outlook, most of the graphs won’t show. I’d recommend you read it online

📕 Reads of the Week

Market Updates

Market Financial Solutions, a UK mortgage provider with more than £2 billion of debt, enters administration. Banks account for the vast majority of the exposure. No prizes for guessing who the coverage is privately crediting. Link

European Lower Mid-Market Premium to Upper Mid-Market

The European Lower Mid-Market premium to Upper Mid-Market Falls Below 60 bps.

Manager Updates

Calpers Unfazed by Software Stress in Private Credit. Link

Anyone asking Bloomberg News what AI means for Bloomberg Terminal Subscriptions?

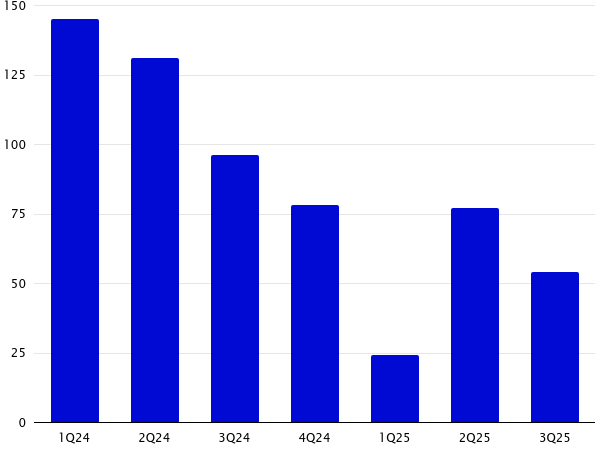

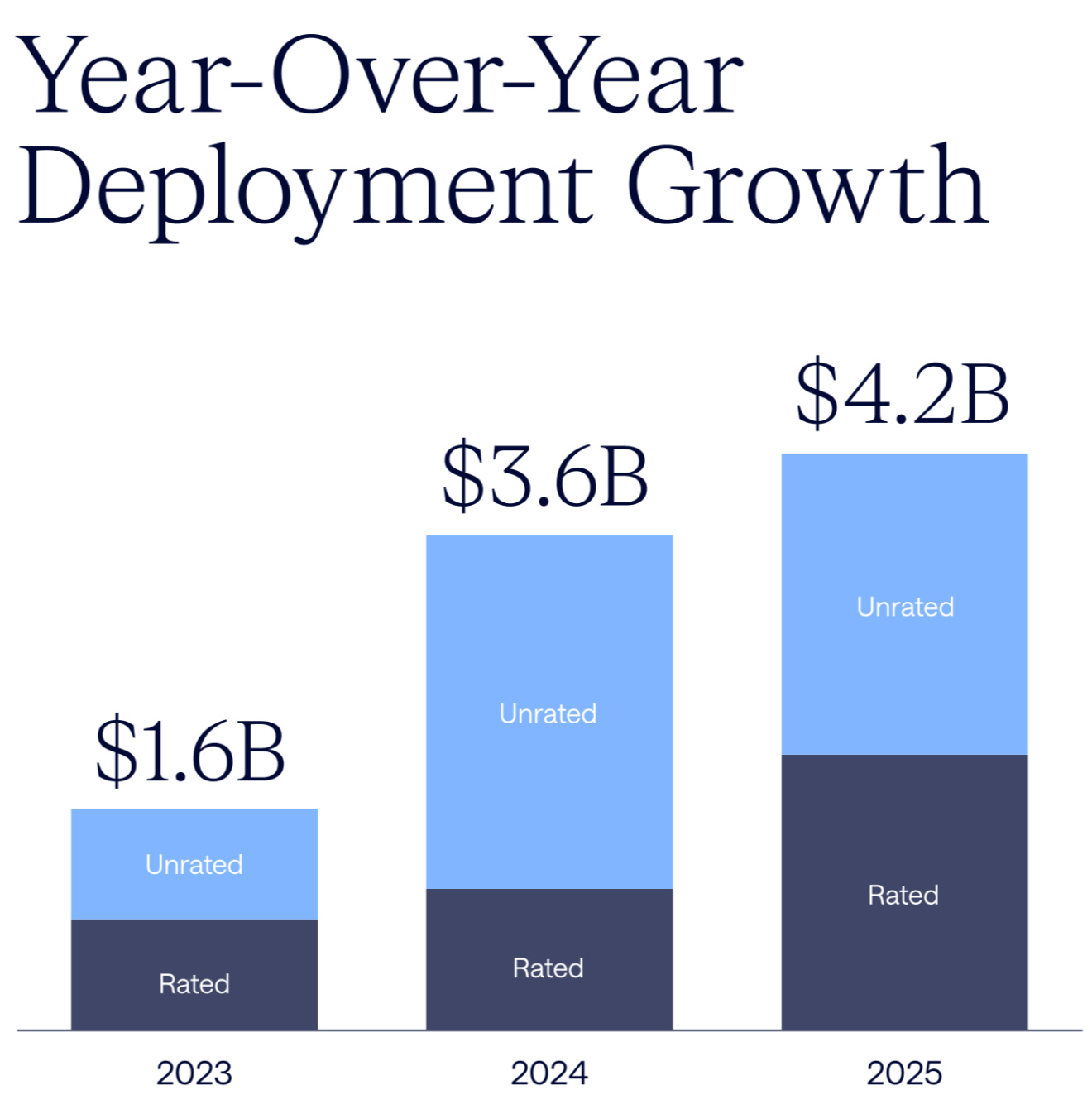

Ares Alternative Credit's Fund Finance 2025 Year Review. Link

Deployment has more than doubled since 2023.

BDC Updates

“The problem is the right asset with the wrong structure. There’s a silver lining: you can still use this structure, but don’t promise outperforming returns, don’t use so much leverage, and get back to basics of underwriting.”

BlackRock Private Debt Fund Slumps After Slashing Dividend. Link

Apollo’s MidCap Financial cut its dividend and marked down the value of its assets. Link

New Mountain Finance agreed to sell $477 million of assets to a third party at 94% of fair value for the purposes of increasing portfolio diversification and reducing PIK income. Link

FS KKR Capital Q4 FY2025 earnings call transcript. Some fairly spicy questions on fees. Link

For investors concerned about the uncertainty of technology obsolescence risk, enterprise value destruction for the software industry, and the burgeoning threat of artificial intelligence, SLR Investment Corp.'s portfolio, with its lack of software exposure, can be viewed as a safe haven

Michael Gross, CEO of SLR Investment Corp, Speaking at his Q4 earnings

Partnership Updates

BNP and Apollo Global are expected to announce a European private credit partnership with both firms jointly arranging loans for corporate and private equity-backed borrowers across the region.More here

Looking Beyond Cockroaches and Canaries

TCW published a great piece on how it thinks about the current state of private credit. Below are my extracts.

Whenever someone says, “private credit did X,” the questions should be:

Which part of private credit?

Who in private credit actually made this investment?

Jamie Dimon talked about cockroaches, others about canaries. While we believe there’s truth in these comments, they don’t completely capture what’s happening.

The core issue isn’t that these specific companies failed. The message is that aggressive, careless underwriting has been creeping into the market for the past seven or eight years. During that time, we had near zero base rates, expanding enterprise value multiples, abundant capital, and no recessions. This environment fostered, and hid, a lot of bad lender behavior: looser documentation, shortcuts in diligence, increasingly more borrower friendly terms.

Now that rates are normalizing and economic volatility is back, we expect this aggressive behavior will be exposed.

By no means is this the end of private credit. These events are reminders that many lenders haven’t been as prudent as they should have been. We expect to see more mistakes.

A Glimpse From Software

When the biggest part of the market is built on the idea that growth is durable and recurring revenue solves most problems, even a small reset can reveal where lenders leaned too much on the narrative and not enough reliance on conservative lending assumptions.

That doesn’t make software a “problem sector,” any more than First Brands or Tricolor made their respective industries a problem. It just reminds us that when a large corner of the market is priced with little to no margin of error, the surprises tend to show up in bunches – not because everything is connected, but because the overall behavior behind these loans was similar.

Dispersion Is Coming – Principal Preservation Matters Again

For most of the post Global Financial Crisis (GFC) era, private credit managers all looked pretty similar and pretty good. Defaults were rare, recoveries were decent, and the environment frankly didn’t test whether lenders knew what they were doing. That period is over.

Lincoln International’s estimate that there was $24 billion in foreclosed debt in 2025, nearly 2x the previous three years combined, shows lenders are finally taking remedies on underperforming companies.

That’s not a sign of crisis. In our view, it’s a sign of a maturing market – and of a long overdue differentiation between strong and weak underwriting. It’s a return to focusing on the single most important differentiator in credit investing: principal preservation. Not deployment. Not AUM growth. Not headline yields. We have said it many times: lending money isn’t hard – getting repaid can be hard. The managers who understood that during the very good times are the ones who will stand out now in this less certain environment.

The Vintage Problem – And Why 2021-2022 Is Showing Up Now

A lot of the pain emerging today traces back to the 2021-2022 post-COVID environment.

Low rates, unsustainable and elevated enterprise value multiples, fierce competition, and enormous pressure to put capital to work.

Many lenders stretched. Some ignored valuation discipline. Others leaned into borrower friendly terms because of the pressure to win the deal. These mistakes cannot be fixed after the fact. You can’t retrofit discipline. Adding restructuring help to the staff now feels a bit late.

We expect the next several years could look “vintage sensitive,” even though we do not believe private credit should be considered a vintage driven asset class.

Figure 1. Global Dry Powder by Asset Class

Source: Pitchbook

Deals Matter More Than Capital Inflows

People often say today’s tight spreads and weaker structures are because too much dry powder and fresh capital has moved into private credit. While we understand the sentiment, we don’t think that’s the root cause. Private equity has significantly more dry powder than private credit, (see Figure 1). They’re simply not deploying it. The real issue is too few deals in the market, (see Figure 2).

Figure 2. Private Equity Platform M&A Activity

Source: Lincoln VOG Proprietary Private Market Database

Until sponsors start actively buying companies again, lenders will be competing for a limited set of transactions – and when competition heats up, underwriting standards slip. But over time, we believe the market deals with this.

Managers without discipline don’t survive stress.

Howard Marks’ Key Questions on AI

Howard Marks Revisited AI. Below are the key Q&As.

Is the technology a fad or an illusion?

I say with conviction that it’s a very real thing, with the potential to vastly alter the business world and change much of life as we know it.

Is the application of the technology a distant dream?

Clearly, the technology is already in demand and being applied on a large scale. Since AI seems amorphous and little understood, I think its potential is more likely to be underestimated today than exaggerated.

Are the people building AI infrastructure behaving unwisely?

In every example of sweeping technological innovation, the headlong rush to build infrastructure has vastly accelerated the adoption of the innovation and caused a lot of capital to be “malinvested” and destroyed. There’s no reason to assume this time will be different.

Will the investment in AI infrastructure produce an adequate return?

Since we don’t have full knowledge of AI’s business potential or its impact on profitability, this question can’t be answered. There’s certainly great enthusiasm for AI businesses. We’ll know in 10 years whether the resulting profits justified it.

Are the valuations assigned to AI businesses irrational?

The so-called hyperscalers, for whom AI is one important part of a great business, may be overvalued or undervalued, but it’s unlikely that today’s prices for enormously profitable companies like Microsoft, Amazon, and Google are going to turn out to have been ruinously excessive. Established pure AI plays like OpenAI and Anthropic have yet to be listed publicly; we’ll see what kind of valuations their IPOs result in. Finally, the startups to which multi-billion-dollar valuations are being assigned – some of which have yet to describe their strategies or announce products – can only be viewed as lottery tickets. Most people who participate in lotteries end up with worthless tickets, but the few winners get very rich.

💰Fundraising News

Arcmont Asset Management, a London-based manager, closed its $1.8 billion Capital Solutions Fund II. The opportunities fund invests in more complex credits, junior capital, and market dislocations. Since launch, the strategy has invested nearly €2 billion in more than 50 transactions. Capital Solutions II is currently c. 55% committed with a portfolio of more than 20 investments. More here

5C Investment Partners, a New York-based manager, announced a partnership with Qatar Investment Authority. 5C provides direct financing to high-quality companies in the upper middle-market. The new investment will help the expansion of 5C’s existing direct lending platform and drive the development of new investment strategies. 5C has grown its platform to $3 billion of investable capital since launching in 2024. More here

Appendix / Cut

Brookfield says software loans are not systemic. Link

Stepstone on recent trends in corporate direct lending 2H25. Link

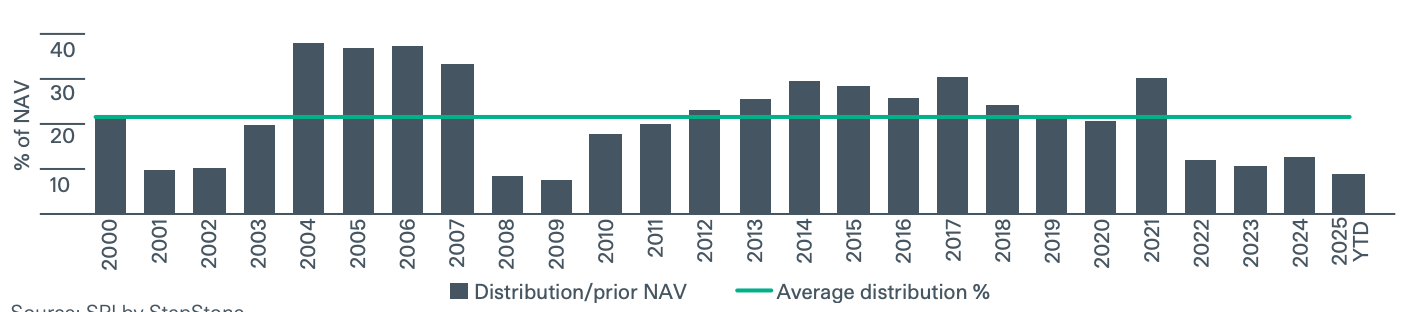

PE Distributions vs 20-year Average

Now that returns in private credit are 8 or 8.5%, the returns on the public credit side seem to be 6 or 6.5%. So that relative value still holds.

That’s the right way to evaluate it. Are you being paid sufficiently for the illiquidity that you are assuming?

That’s demonstrably yes.

Mike Patterson, HPS Founding Partner and Co-President

This newsletter is for educational and entertainment purposes only. It should not be taken as investment advice.

What’s the source of that first chart on Europe DL? When I click on invesco link it takes me to cliffwater