Three Nonconventional Takes on the Private Credit’s “Crowded Market”

Fundraisings from Crestline, Schroders, Arena, Beach Point, BluePeak and more.

“It’s becoming a very crowded market…

You may end up investing in private credit, thinking it’s a credit piece, but when issues come by, you realise it’s more of an equity story…

We’re focused on fewer managers and to go with scale.”

Mohammed Al Sowaidi, Head of the Qatar Investment Authority.

Watch the full interview here

👋 Hey, Nick here. It’s easy to jump to the conclusion that the flood of capital over the last 4 years has led to a demand/supply imbalance and therefore private credit has lost its “Golden Moment”.

Time to look for a new job.

But this problem isn’t new or unique, and before you think about changing industries, it’s worse in other asset classes. Public Equity, Private Equity & VC are easy examples.

You should also realise that you’re deployment issue is likely to be a lot smaller than the scaled managers. Recall that some of the leading managers are hoping to double AUM over the next 5 years. Apollo ~$ 500 B+ growth, Brookfield ~$ 250 B+ growth, Blue Owl ~$ 250 B+ growth.

Despite, or maybe because of, these insane ambitions, they’re approaching this problem with a slightly different perspective. Scroll down to learn more.

A special welcome to the new subscribers from The Middle Market and Evergreen Cap. It’s great to have you. Reach out and say hi. This is the 115th edition of my weekly newsletter. You can read my previous articles here and subscribe here

📕 Reads of the Week

With Intelligence’s Emerging Managers to Watch. Link

KBRA Calls Out Fitch’s Integrity. “In seeking relevance to increase its market share in private credit, Fitch appears to have undercut two foundational principles for any rating agency—integrity and analytical rigor. Read the FT report here and KBRA’s statement here

Brookfield: The Universe Keeps Expanding. Link

SEC Moves to Expand Retail Access to Private Markets. Link

The NBA Doesn’t Like Debt. Link

KKR Investor Update. Link

HSBC is reorganizing its capital markets and corporate advisory to enhance its private credit offering. Link

🎧 HPS: Current Credit Market Trends

Proskauer: Three Risks to Monitor in Private Credit. Link

🏦 Partnerships of the Week

Natixis Seeks Partners for $1.5 Billion Private Credit Fund Link

SEB launched a new private debt fund in partnership with Capital Four, a Danish credit manager. The fund will focus on middle-market businesses in Northern Europe. The fund is an ELTIF allowing both professional and non-professional investors to invest. More here

📊Three Nonconventional Takes on the Private Credit’s “Crowded Market”

The charts below are from Configure Partners’ Quarterly Update. As regular readers will know, I share these because they offer an honest and insightful perspective on private credit. You should read the full report here.

Credit Yields Are Being Driven By Base Rates

Although average spreads have returned to early 2022 lows, all-in borrowing costs have risen from ~7.5% to ~11.2% (~370 bps increase), due to higher base rates.

Spreads continued to compress, especially for higher-quality deals. Over the past year, average spreads tightened by ~100 bps.

Configure’s Q1 Private Credit Lender Survey reported an average approved spread of 532 bps. However, Configure’s dataset shows ~640 bps due to a higher proportion of refinancings and more challenging credits.

Conventional View

Private Credit Has a Problem: Too Much Money. Source

Non-Conventional View:

[Jon, last year, you referred to it being a gold moment for private credit. What is your assessment today? Are we still in that golden moment?]

Jon Gray - Blackstone: “The golden moment part was related to the fact that base rates were very elevated, spreads were quite elevated, you could earn equity-like returns, mid-teens returns, owning credit, senior credit. And some of that, of course, goes away as the Fed eased, 10-year has come down, spreads have tightened. And so the returns you can earn are not as high on an absolute basis.

But this really is more of a golden era when you think about the durable spread difference relative to liquid fixed income. And there, you continue to see a meaningful premium, and you can see it in our performance in the quarter. You can see it in our various BDCs that are out there that you’re still able, because of this farm-to-table model, basically bringing the investors right up to the borrowers, you capture that incremental spread. That’s not going away.

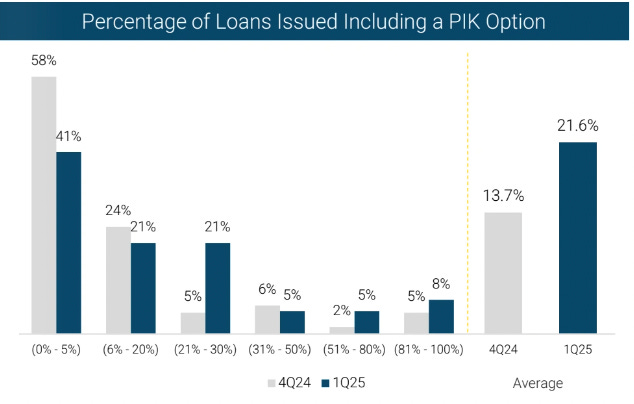

PIK Adoption Jumps

Configure’s Q1 Private Credit Lender Survey shows that more than 1 in 5 loans included a PIK option.

This is nearly double Q4 2024.

Conventional View:

Barclays: “In our view, the suppression in private credit default rates in recent quarters is largely attributable to PIK toggles. PIK has been a great tool for issuers seeking to preserve margins and cash balances during this period of elevated base rates, but we believe that private credit’s structural advantage of PIK inclusion may be at its inflection point. Given negative net capital distributions for the past several years, lenders with skewed cash-pay/PIK proportions may feel greater pressure from LPs to sell down portfolios in order to manufacture distributions.” Source

Non-Conventional View:

Blue Owl: “There's 2 kinds of PIK.

There's the PIK by design because it's an extremely durable, low-LTV cap structure with a huge equity check and a really great business. And it's about giving the company, by design, the ability to invest in its own growth, i.e., software companies…

PIK by design is, actually from our point of view, usually an extremely good sign. We do that in our strongest credits. Those tend to be our "lowest loan-to-value" and biggest businesses.

And then there's PIK not by design. PIK because you had to go from cash pay to PIK is a bad thing. There's no other way to describe that. Watch migration -- from non-PIK to PIK, not helpful. We have some of those. We always will. That's part of it with 400 companies.

Don't use the blunt instrument of PIK as a share of a portfolio. That's meaningless. And point of fact, PIK as a share of a portfolio is higher in our software business. And saying this the right way: Isn't everyone who's invested in software credits today, thrilled that that's where they are? Take a look at what's happening. Supply chain, don't have one. Exposure to China, don't have any. I mean, think about the things that are now a risk for most companies in the world, not a risk for our software businesses. Our tech portfolio is exactly where you want to be, and yet it does have a higher-percentage PIK by design.”

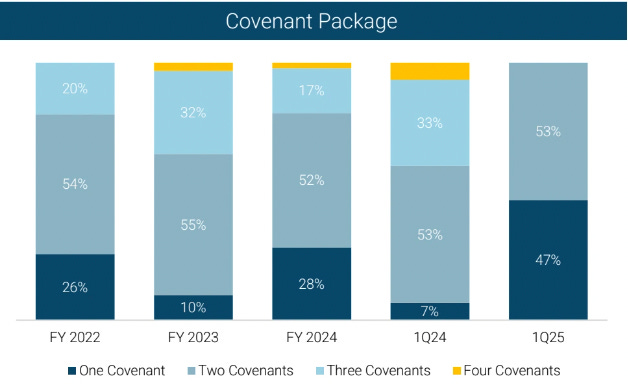

Covenants are Paying the Price

The use of one-covenant structures surged nearly 7x year-over-year, rising from just 7% in Q1 2024 to 47% in Q1 2025.

Whilst two-covenant deals remain the norm, one-covenant structures are increasingly offered to high-quality borrowers.

Conventional View

S&P Global: “Loose Maintenance Covenants Permeate Private Credit” Source

Non-Conventional View

Apollo: “We are in the business of excess return per unit of risk. Therefore, we are able to grow only as fast as we are able to originate good assets that offer those risk/reward characteristics. Thus, our relentless focus on origination as much as we possibly can across the board and in most of the asset classes

It's about how many assets I can originate that are worthy of inclusion because they offer good risk/rewards. It's a really weird dynamic over 40 years because for 40 years we've gone from a small group of firms doing alternatives to now a fewer number of sizable firms doing private markets. We've always been measured by or limited by our capital base. We're now, in my opinion, limited by our capacity to find good assets

💰Fundraising News

Crestline Investors, a Texas-based alternative manager, closed its $3.5 billion Direct Lending Fund IV. The fund finances sponsor and non-sponsor backed companies across North America. It lends across the middle market but has a focus on the lower and core segments. Crestline’s direct lending strategy, launched in 2014, has closed over 150 transactions with more than $5.9 billion of capital invested. To date, CDLIV has completed 46 transactions. More here

Schroders Capital, a London-based alternative manager, raised $2.2 billion for its Junior Infrastructure Debt Europe III fund. The strategy focuses on the infrastructure mid-market across a range of sectors, such as data centres, energy companies and renewables. It targets predominantly brownfield assets in core European countries. The fund is already c. 50% deployed, delivering a gross return in excess of 8%. More here

Crestline Investors, a Texis-based alternative manager, closed its $1.7 billion Portfolio Finance Sentry Fund. The NAV financing fund lends to private equity and private asset funds seeking liquidity to acquire new assets, grow existing assets, and optimize fund and portfolio capital structures. The Sentry series will target larger, more diversified transactions with high-quality sponsors. The fund has closed nine transactions across diversified sectors, including real estate, buyout, and opportunistic credit, with activity spanning North America and Europe. More here

Arena Investors, a New York-based asset manager, closed its $1.1 billion Special Opportunities Fund III. The fund will. Arena's flagship strategy has a 10-year track record of originating and managing portfolios of uncorrelated corporate, real estate, and structured finance investments. Fund II closed in August 2022 with $930 million. More here

Elham Credit Partners, a Singapore-based credit manager, is expected to raise ~$700 million for the first close of its inaugural private credit fund. Elham’s strategy will focus on performing credit investments in profitable, mid- to large-cap companies across key regional markets such as Australia, India, and Japan. Elham is reportedly targeting a final fund size between $900 million and $1.1 billion. More here

Beach Point Capital Management, a California-based manager, raised $750 million for its BPC Opportunities Fund V. The fund is Beach Point’s largest Opportunities Fund since the strategy was established in 2010. It will invest across the full range of middle market opportunistic private credit, including investing in complex businesses, highly structured transactions, and temporary market or company dislocations. Beach Point invested more than $5 billion through this strategy in sectors including opportunistic direct lending, capital solutions, asset-backed, and special situations. More here

Beach Point Capital Management, a California-based manager, raised $545 million for its BPC Real Estate Debt Fund. The fund is Beach Point’s first dedicated real estate fund, and invests across the United States’ middle market. The fund’s strategy spans directly across originating loans, seeking to opportunistically purchase debt at compelling discounts to intrinsic value, and special situations that may provide additional equity upside. More here

Allianz Global Investors raised $455 million for its Core Private Markets Fund. The strategy provides well-informed and professional clients the opportunity to invest alongside Allianz in infrastructure (equity and debt), private debt, and private equity. It aims is to offer a portfolio across geographies, segments, vintage years, and sectors, aiming to generate attractive high single-digit returns with comparatively low volatility. More here

BluePeak Private Capital, an African alternative manager, announced a first close of $80 million for its Private Capital Fund II. The impact-driven fund lends to middle-market companies across Africa. It will invest in strategic and defensive sectors that are driving the continent’s growth, including manufacturing, pharmaceuticals, logistics, and financial services. More here

Hamilton Lane launched its first private credit interval fund. More here

Learn more

This newsletter is for educational or entertainment purposes only. It should not be taken as investment advice.

Great read! Do more of these