Three Takes on Blue Owl's OBDC II

Fundraisings from Fortress, Ares, Tikehau, CAPZA and more...

👋 Hey, Nick here. A big welcome to the new subscribers from Curasset Capital, Ares, and The Financial Times. This is the 154th edition of my weekly newsletter. If someone forwarded this to you, you can subscribe here and read my previous articles here.

If you’re reading this on Outlook, most of the graphs won’t show. I’d recommend you read it online

📕 Reads of the Week

Market Updates

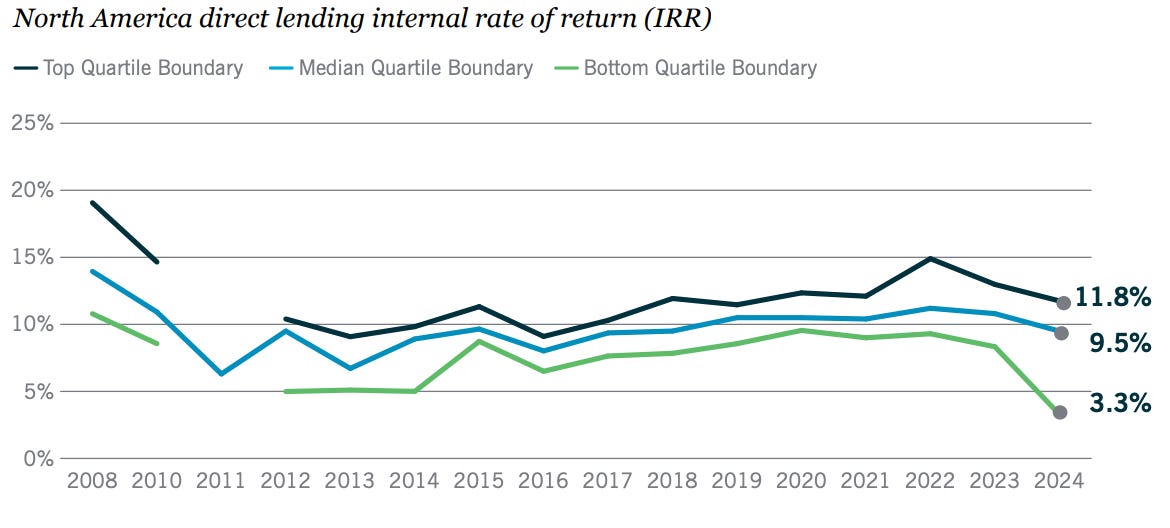

Private Credit Dispersion is widening

Current default rates remain modest, Proskauer’s lastest index reported a 1.84% default rate, consistent with the second quarter’s 1.76%, but stress typically manifests with a lag.

Return dispersion has elevated and Nuveen expects it to widen further as performance issues surface among managers that:

Competed aggressively for deals in crowded markets

Relaxed leverage, documentation or structural protections during peak deployment periods

Drifted from core strategies in pursuit of scale

European Recapitalisation Surged nearly 4x in 2025

In total, €5.5bn of European direct lending deals were recapitalisation-related, materially higher than the previous record of €2.6bn in 2024.

Pitchbook recently reported that the median hold time for private equity owned companies has risen to 3.8 years, the highest level since 2011.

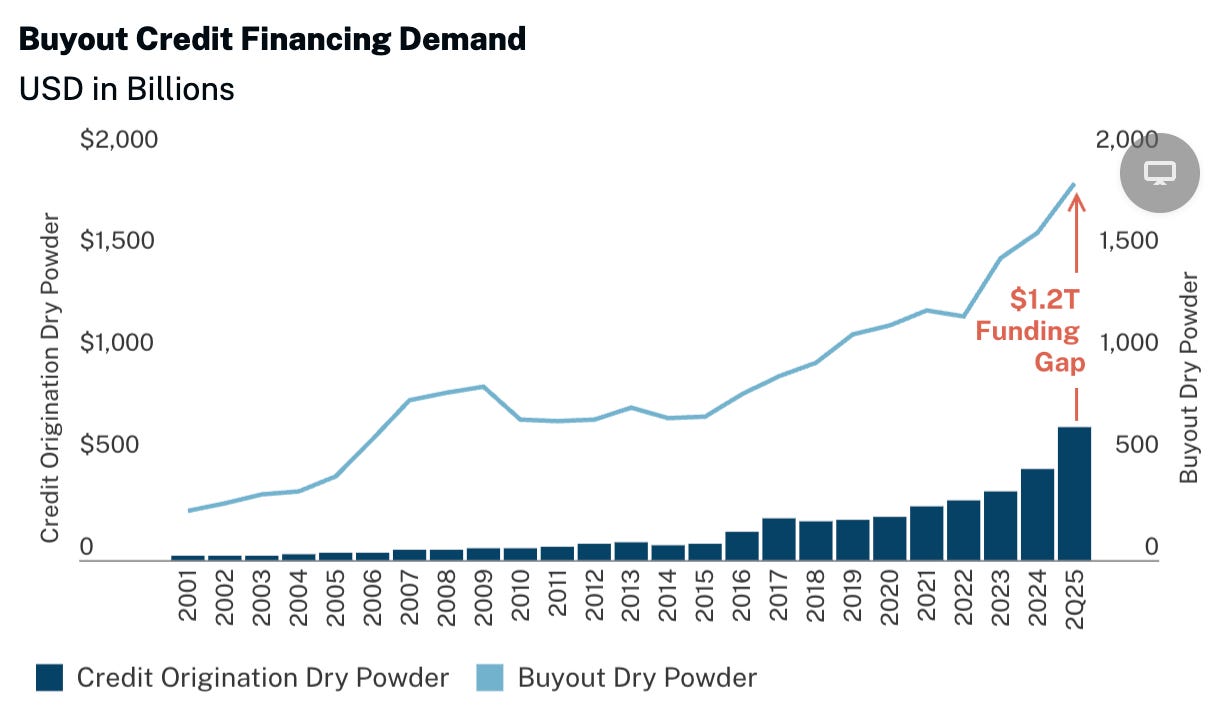

The $1.2T Funding Gap Driving Private Credit Growth

Hamilton Lane compared private equity dry powder againsts private credit dry powder.

Based on their analysis private credit has $1.2 Trillion less dry powder.

If you assume 50% LTVs, the implied funding gap is at least $1.2 trillion

In practice, many of these companies may use less leverage or access BSLs and other liquid credit markets.

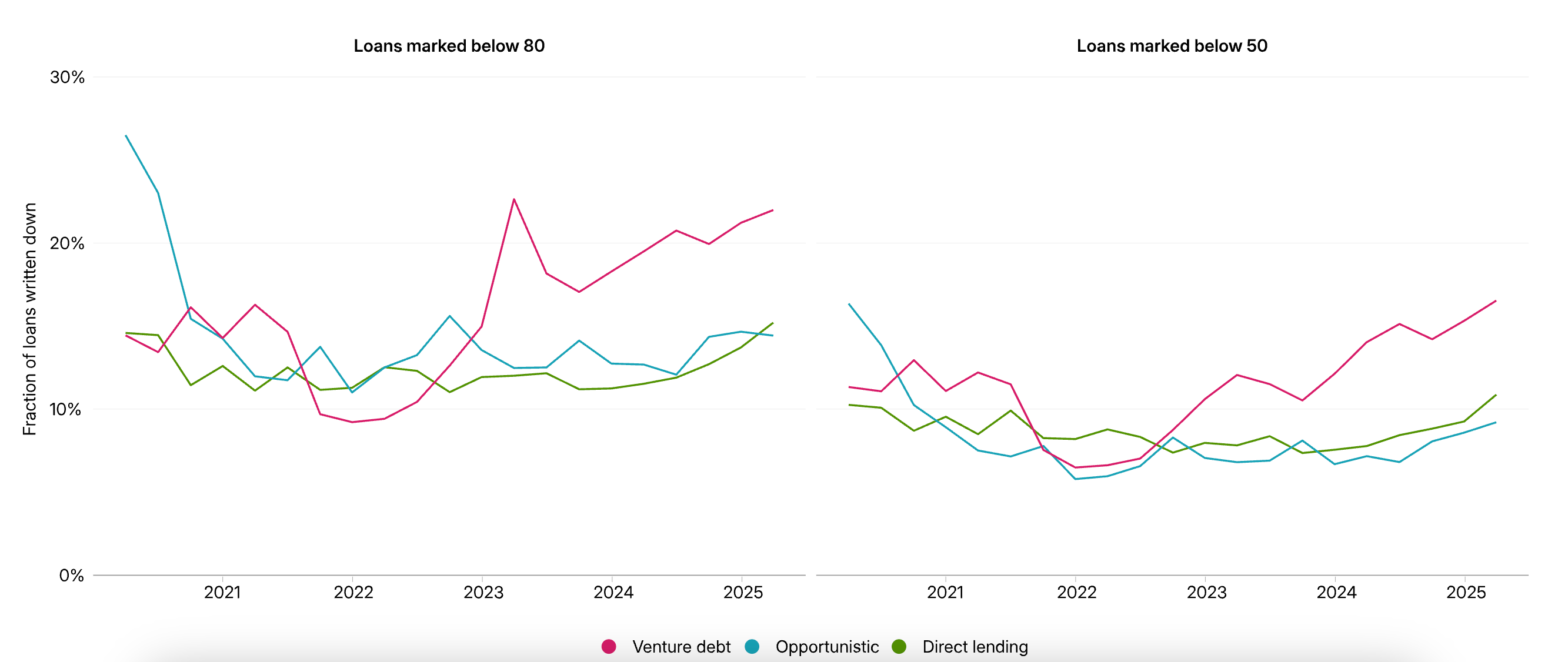

Venture-debt loan deterioration has accelerated sharply since 2022

Given venture debt’s sector composition, IT exposure would seem a natural explanation for the rise in distress. IT represents nearly 40% of the net asset value in venture debt, compared with 19% for direct lending and 7% for opportunistic funds.

However, it’s health-care borrowers that have largely driven the recent venture-debt write-downs, while technology loans have exhibited below-average rates of distress.

Manager Updates

Bank of America is committing $25 billion to private credit. Link

Apollo: How Is Liquidity Evolving in Private Investment-Grade Credit? Link

Ares’ 7 Priorities for 2026. Link

KKR: Ctrl + Alt + Credit. Link

Partnership Updates

CVC has partnered with AIG to manage up to $2 billion in insurance-focused private credit mandates. More here

Three Takes on Blue Owl’s OBDC II

You’ve probably read a lot about Blue Owl this week. Instead of adding to the noise, below are three of the top articles I’ve read.

CovenantLite: Blue Owl on the Ropes. Link

Using OBDC’s roughly 1.19x debt-to-equity leverage, a 23% discount implies about a 10.5% gross markdown on the portfolio

In other words, if you take OBDC’s discount literally as a pure credit-loss forecast, the market is pricing something like a GFC-level (or worse) loss cycle.

So Is the Discount Overdone?

The short answer is a cautious yes, but only if you treat OBDC’s discount as a pure forecast of credit losses.

OBDC is not in active distress.

Leyla Kunimoto’s deepdive into understanding 🦉 OBDC II’s asset sale and structural shanges. Link

Everything sold was rated 1 or 2, these are the best quality assets in the portfolio. After backing out the ~$538M in fair value that just walked out the door (the $600M headline includes unfunded commitments), OBDC II’s remaining portfolio shrinks to roughly $1.18 billion. The problem children are still in the portfolio…

If we add up non-accruals and the impaired second-lien names, you’re looking at roughly ~15% of the remaining portfolio. That’s up from ~10% before the sale.

Cliffwater: Blue Owl’s problems are not investment-related but instead caused by its BDC’s obsolete structure. Link

Blue Owl has now done the right thing.. Returning 30% of investor capital that otherwise would have taken well over one year.

Full liquidity for OBDC II investors will likely come over the next year

We view the Blue Owl sale transaction as a sign of strength in the private debt market and not, as the Wall Street Journal characterized it, as a warning sign.

Headlines cherry-picking loan defaults are also running contrary to actual private loan performance. OBDC II historically delivered strong loan performance since its March 2017 inception. Its underlying loan portfolio has returned an annualized 9.11% through September 30, 2025, compared to 9.19% for the Cliffwater Direct Lending Index (“CDLI”) covering the same period.

👉 Read Cliffwater’s analysis here

Saba Capital and Cox Capital Partners

Saba Capital Management today disclosed that they provided notice to Blue Owl Capital Corporation II of their intention to commence a tender offer to purchase a portion of outstanding shares of OBDC II in cash…

The offer price is expected to be at a 20-35% discount to the most recent estimated net asset value

👉 Read Saba Capital’s press release here

Contrary to what has been reported, we are not halting investor liquidity in OBDC II. In fact, we are accelerating the return of capital…

Instead of resuming a 5% quarterly tender—under which only tendering investors would receive a partial return of capital—we are distributing an amount six times greater and returning capital to all shareholders within the next 45 days.

I still have a few outstanding questions: 1) What is OBDC II’s fund end date / why accelerate the run-off now? 2) Has anyone forecasted the fund’s cashflows over the next few years? What does this loan portfolio look like? 3) Why didn’t Blue Owl just pay the 5% quarterly redemption over the next 6 quarter?

If you know the answers to any of these please comment below / send me a message.

💰Fundraising News

Fortress is adding an unleveraged sleeve to its latest private credit vehicle as it looks to broaden appeal among insurance companies. The new structure will sit alongside the leveraged version of Fortress Lending Fund V, which is targeting total commitments of at least $3 billion. While the leveraged sleeve will invest in a mix of direct corporate lending and asset-based finance, the unleveraged option will focus primarily on direct corporate loans. Fortress is targeting net internal rates of return of around 11% to 14% for the leveraged sleeve and approximately 8% to 9% for the unleveraged version. More here

Ares and Coller Capital closed a continuation vehicle for Ares U.S. Direct Lending’s 2018-vintage fund with more than $1.3 billion in total commitments. The continuation vehicle comprises a diversified portfolio of first-lien, floating-rate loans to U.S. middle-market companies backed by leading private equity sponsors. More here

CAPZA, a French investment manager, announced a first close of $1.7 billion for its Private Debt 7. The fund provides financing to SMEs and mid caps primarily in France, Germany, the Benelux, Spain and Italy through unitranche and subordinated debt. This seventh vintage is part of the broader offering of BNP Paribas Asset Management Alts, which currently manages approximately €135bn in private debt and alternative credit assets. More here

Tikehau Capital, a French alternative asset manager, announced a final close of $1 billion for its second vintage private debt secondaries fund. Launched in 2019, the fund invests in secondary transactions across North America and Europe. The fund has deployed approximately 50% of its committed capital. More here

Brigade Capital, a New York-based manager, raised $1 billion for its first dedicated private credit fund. The opportunity fund less efficient segments of the market including lending to lower-to-middle market and non-sponsor borrowers. More here

Keppel, a Singapore-based manager, has raised $561 million for its third private credit fund. Keppel’s private credit strategy finances companies with defensive infrastructure-like operating businesses across a wide range of real asset sectors, including renewable energy, transportation, telecommunications,and logistics in Asia Pacific. The fund targets low- to mid-teens returns. More here

Patria Investments, a Latin America-focused manager, is launching the next vintage of its Latin America private credit strategy. The fund focuses on senior secured, US dollar-denominated loans structured with robust collateral, covenants, and cash-flow protections for mid-market and family-owned borrowers.The prior fund has already deployed more than 70% of capital into 14 transactions, generating a gross unlevered IRR of 15.6% with an average duration of 2.5 years.

Star Mountain, a U.S. lower middle-market manager, closed its second $286 million SBIC fund. The fund will make debt and equity investments in established service-oriented U.S. small and medium-sized businesses. More here

Janus Henderson and Victory Park Capital (“VPC”) today announced the launch of the Privacore VPC Asset Backed Credit Fund. The firm’s first interval fund aims to provide exposure to private asset-backed credit. More here

This newsletter is for educational and entertainment purposes only. It should not be taken as investment advice.