Upper middle market defaults are doubling every quarter

Fundraising from Silver Rock, Primary Wave, Apollo, Stepstone and more...

👋 Hey, Nick here. A big welcome to the new subscribers from Petition, Resolution Life, and Nippon Life. You’re now part of a select group of 2,924 subscribers. This is the 165th edition of my private credit newsletter.

If you’re reading this on Outlook, most of the graphs won’t show. I’d recommend you read it online

📕 Reads of the Week

Market Updates

KBRA: Q1 2026 Middle Market Report *** (Subject Piece) ***

Upper middle market defaults are doubling every quarter.

A record count of companies received a downgrade of two or more levels.

The decline in sales growth in the Financial Services sector was the highest among all sectors.

Roll-up strategies continue to experience stress, amplified by elevated leverage.

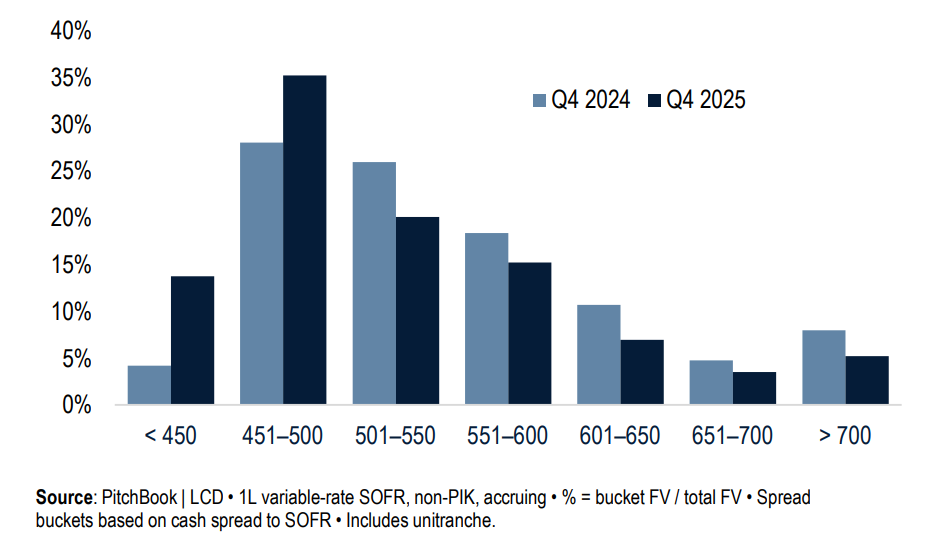

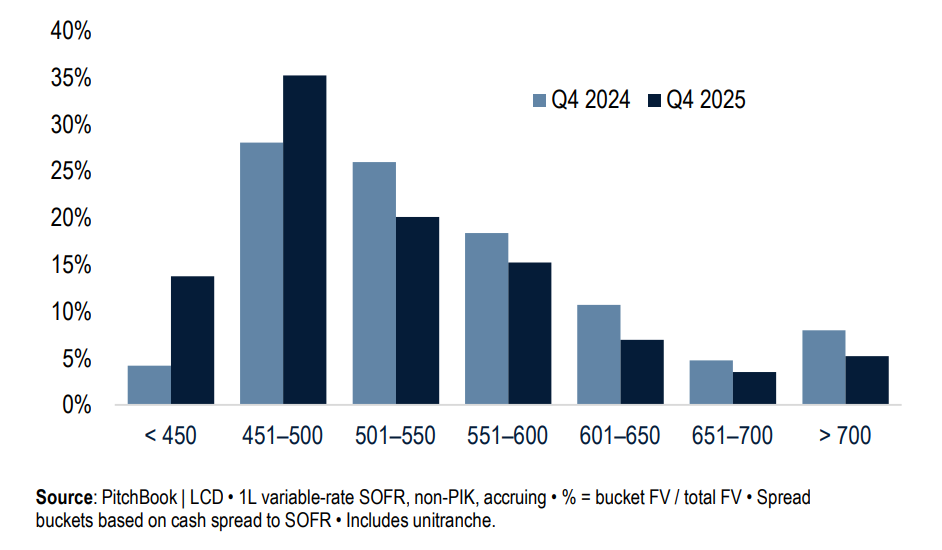

Peek under the Hood: An Analysis of Private Credit Loans in Top Public BDCs.

The all-in yield on first-lien debt, Sofr-referenced loans across ten BDCs, was 9.2% in Q4 2025, down 100 basis YoY.

KKRs Wealth - Private Market Survey

1,000 individual investors with $500K+ in investable assets, To get a clearer view into how individual investors are thinking about private markets,

Fewer than 1 out of 10 investors correctly identified that, 93% of U.S. companies with $50M+ in revenue are privately held.

Cliffwater: Ten Misconceptions About Private Credit. Link

Jim Zelter and Eric Needleman challenge outdated views of private credit.

Manager Updates

Q1 Results Takeaways

Jon Gray’s Three Takeaways from Blackstone. Link

Earnings increased 25% YoY

They have a pipeline of 12 companies preparing for IPOs

AI infrastructure will drive future investment trends

Mike Arougheti’s Takeaways from Ares. Link

Record fundraising, up 46% YoY

Three of Ares’ largest private credit funds recorded are in the market or will be in the market in the next 12 months

Total management fees exceeded $1 billion, up 22% YoY

Howard Marks calms down Andrew Ross Sorkin. Link

BlackRock on Healthcare Growth Debt and Venture Debt.

Lazard buys Campbell Lutyens for $575m. Link

Brown University sells half its position in Blue Owl Capital Inc. Link

BDC / Interval Fund Updates

Saba Announces New BDC Strategy to Address Retail Investor Liquidity Needs

The strategy targets entry points at discounts of 30-40% or greater to NAV,

Saba believes the question is not whether this space will experience significant stress, but when.

Invesco: Navigating BDCs’ Growing Pains. Link

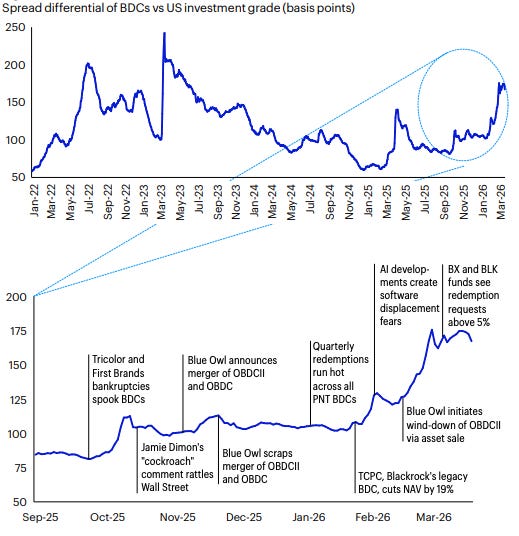

Timeline of Spread Differential of BDCs vs US IG

Partnership Updates

ICEA LION, an East African provider of insurance and pensions, is looking to invest in pan-African private credit funds. It has a preference for managers that have strong relationships with DFIs, and are ideally on at least their second or third fund. Link

Goldman Sachs on Private Credit

Goldman Sachs’ latest newsletter asks a lot of loaded questions. Hidden amongst the filler are a few genuinely interesting points. Below are my highlights.

Redemptions Gates shouldn’t be surprised. But “should” is one of the most interesting words in the English language.

Howard Marks: “It’s absolutely true that investors participating in a fund that limits redemptions shouldn’t be surprised when full liquidity isn’t available. But “should” is one of the most interesting words in the English language. If people shouldn’t expect liquidity, why are they disappointed when they don't have it? The answer is either that they weren’t adequately informed, or they were well informed but didn’t understand or take cognizance of the terms. The risk of either of these is highest for retail investors, raising the question of whether these vehicles are suitable for the retail base.”

Software Loans won’t Jeopardize the financial system

Howard Marks: If the first-lien lender lost half their money in such a case, that wouldn’t be too bad in a diversified portfolio. If a quarter of the investments are in software and they all incur such losses, then the lender would lose half their money in a quarter of their investments, or 12.5% of the portfolio. And even if they’re levered 1:1, that would amount to a 25% loss, which still isn’t existential. There's an old saying that in times of crisis, all correlations go to one. In other words, everybody panics and sees all outcomes as equally probable and equally bad. But losing a quarter of your capital because the software industry loses most of its value isn’t abysmal. It's just bad for the fund’s investors. And it doesn't jeopardize the financial system

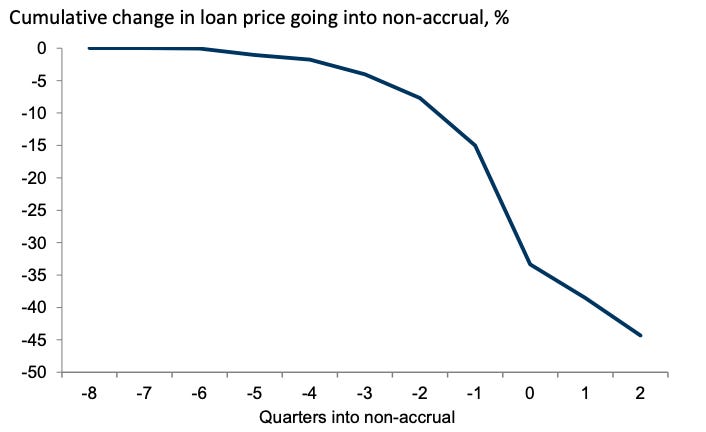

Loan valuations tend to adjust with a lag going into credit distress

Default incentives

Howard Marks: “And it’s important to note that in private credit, what constitutes a default—or even whether lenders will report defaults—is unclear. Lenders have an incentive to grant the borrower an extension rather than report a default, and nobody may be enforcing the reporting of defaults. Particularly for that reason, I wouldn’t put much stock in estimated default rates.”

Three Misunderstood Facts about BDCs

First, so-called “redemption gates” aren’t actually gates. Before non-traded BDCs existed, investors could either have daily liquidity in a traded BDC or illiquidity in a 10-12 year private commingled fund. The innovation of non-traded BDCs was to allow investors to own illiquid assets while providing a structured path to liquidity of 5% of net asset value per quarter or 20% per year, with the structure self-amortizing so investors could be made whole without forced asset liquidations. The 5%/20% limits weren’t pulled out of thin air but rather designed to track the weighted average life of the underlying loan portfolio. So, meeting the contractual 5%/20% is exactly what these structures were designed to do.

Second, no “asset-liability mismatch” or “run on the bank” dynamic exists in non-traded BDCs. Unlike a bank with shortterm deposits and long-term assets, these funds align liquidity with the five-year amortization profile of their loans. They also typically hold 20-30% of assets in liquid securities like loans, bonds, or high-grade investments that can be sold to generate cash, and managers can draw on loan facilities to meet redemption requests. Those features exist precisely to avoid having to liquidate private assets below their intrinsic value.

Third, scale matters. The non-traded BDC market is ~$300bn, representing less than 10% of the nearly $4tn private credit market. Even if every non-traded BDC met its maximum redemption limit, that would amount to ~$5bn of loan sales out of their tradable bucket every quarter, which is small relative to the ~$85bn of loans that trade quarterly in the syndicated loan market. More broadly, adequate dry powder exists in the market to resolve private credit portfolios in an orderly fashion without any disruption to pricing.

Michael Arougheti

Private credit defaults are not actually comparable to public credit

Amanda Lynam: “Some people compare defaults in private credit to defaults in public credit, but they are not actually comparable. Maintenance covenants—periodic financial metrics borrowers must meet—are much more common in private credit than in the broadly syndicated leveraged loan market. Because of that, a covenant breach in private credit can be classified as a covenant default, which counts in the default statistics. By contrast, roughly 92% of the broadly syndicated leveraged loan market is “covenant-lite”, meaning the loans don’t have regular maintenance covenants. Consequently, the first sign of default is often a distressed exchange or a missed payment, which can quickly translate into a monetary loss.”

Direct lending will be okay, but it might take a credit cycle to get there.

Howard Marks: “Only after investors have experienced a full cycle in which it swings from being too easy to borrow money to being too hard are they likely to really achieve the understanding of both the positives and the negatives that enables them to make better investment decisions the next time around. That’s ultimately a healthier investment environment, and it may be what lies ahead for direct lending and private credit more broadly. But learning that lesson isn’t always pleasant.”

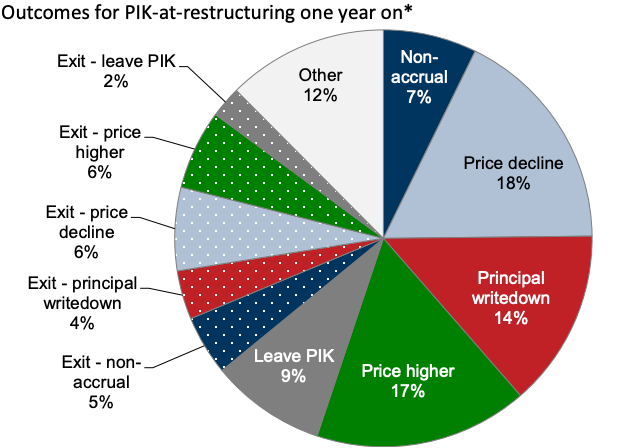

Loans tagged as PIK-at-restructuring tend to see negative outcomes, but not always

Although investors often treat loans that are flagged as PIK-atrestructuring or non-accrual as reliable markers of future credit impairment, in practice the outcomes are more mixed than that characterization implies. Looking at over 3,000 loans tagged as PIK-at-restructuring, we find that 53% experienced negative outcomes, including principal writedowns, lower prices, or transition into non-accrual status, four quarters later. But over a third improved, either by exiting PIK status or increasing in price. So, while less favorable outcomes are more likely, negative outcomes aren’t a certainty.

s

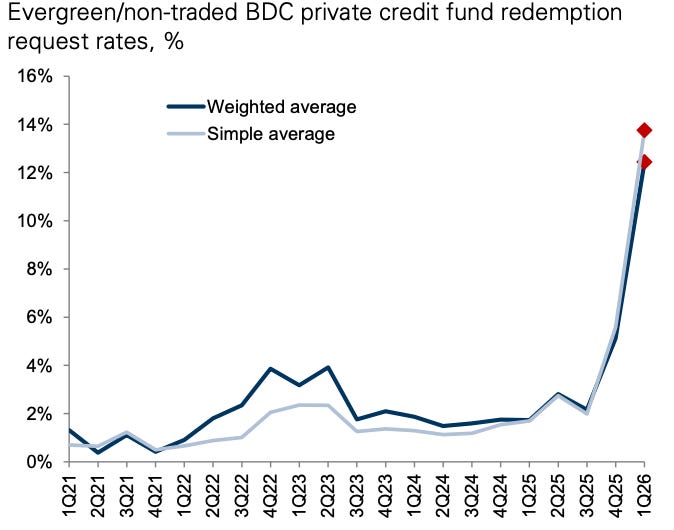

Redemption requests have increased >6x over the last two quarters

💰Fundraising News

Silver Rock Capital Partners, a New York-based alternative credit manager originally born from Michael Milken’s family office, raised $4 billion for its Tactical Allocation Strategy. The strategy provides capital solutions across corporate and real asset lending, targeting large borrowers globally. More here

Primary Wave Music, a music publisher and partner of Brookfield, closed its $2.2 billion Primary Wave Music IP Fund 4. The fund acquires music to generate consistent and long-term capital appreciation. To date, Fund 4 has invested $700 million in over 65 single-artist catalogs, including The Notorious B.I.G., Village People, and Neil Sedaka. More here

Apollo closed its $1.9 billion Accord Fund VII. The fund is the latest vintage of the Firm’s flagship Accord Dislocation Series, which has raised $11.6 billion since inception in 2017. More here

StepStone closed its $1.6 billion Credit Opportunities Fund II. The fund will invest across the private credit spectrum predominantly through secondaries and co-investment transactions. More here

Crescent Cove, a San Francisco-based manager, closed its $446 million Crescent Cove Fund IV. The fund lends to high-growth technology businesses, including businesses operating in defense tech, autonomous driving, AI infrastructure, and cybersecurity. More here

AllianzGI announced the first close of its $270 million Asia Pacific Infrastructure Credit Fund. The Fund provides secured loans to infrastructure and infrastructure‑like businesses predominantly across South and Southeast Asia. It is focused on energy transition, power, digital infrastructure, transportation and logistics, and environmental infrastructure. The fund is expected to hold its final close in 2027. More here

Hamilton Lane launched its Credit Income Fund, raising $350 million in commitments. The fund will invest in a portfolio of middle‑market senior loans, sourced through Hamilton Lane’s global multi‑manager platform rather than index‑based exposure. More here

This newsletter is for educational and entertainment purposes only. It should not be taken as investment advice.