Where Are the Signs of Stress? Hamilton Lane Weighs In

In a market full of warnings, Hamilton Lane is asking for evidence.

👋 Hey, Nick here. A big welcome to the new subscribers from Castlelake, Bonaccord Capital Partners, and Wilmington Trust. You’re now part of a select group of 2,661 subscribers. This is the 158th edition of my weekly newsletter.

A close friend recently asked me why the Credit Crunch is so clearly biased in favour of private credit. Why don’t I link to the negative coverage? If you’ve had similar thoughts, I want to clarify that this is intentional, and there are two main reasons for this:

There’s no shortage of negative news. Why would you want your inbox weighed down by yet another predictable private credit bubble article? If that’s the kind of coverage you want, I’d encourage you to subscribe to two far more reputable publications: the FT and Bloomberg.

The future is shaped by tough-minded optimists. The leading managers aren’t sitting on the sidelines and giving up because they’ve had a few bad deals or a portion of their investors are concerned about their performance. The leaders are addressing the defaults, originating new deals, and raising their next fund. I’m focused on learning from these managers, and hopefully, reading this newsletter will allow you to do the same.

I’m always open to being challenged and would love to hear from you.

If you’re reading this on Outlook, most of the graphs won’t show. I’d recommend you read it online

📕 Reads of the Week

Market Updates

Non-Investment Grade Credit has a 3% default rate.

The private non-investment world is $1.8 billion.

That means $50 billion of defaults. There will be defaults.

Goldman Sachs: Taking The Keys: A Closer Look at the European Private Credit Market

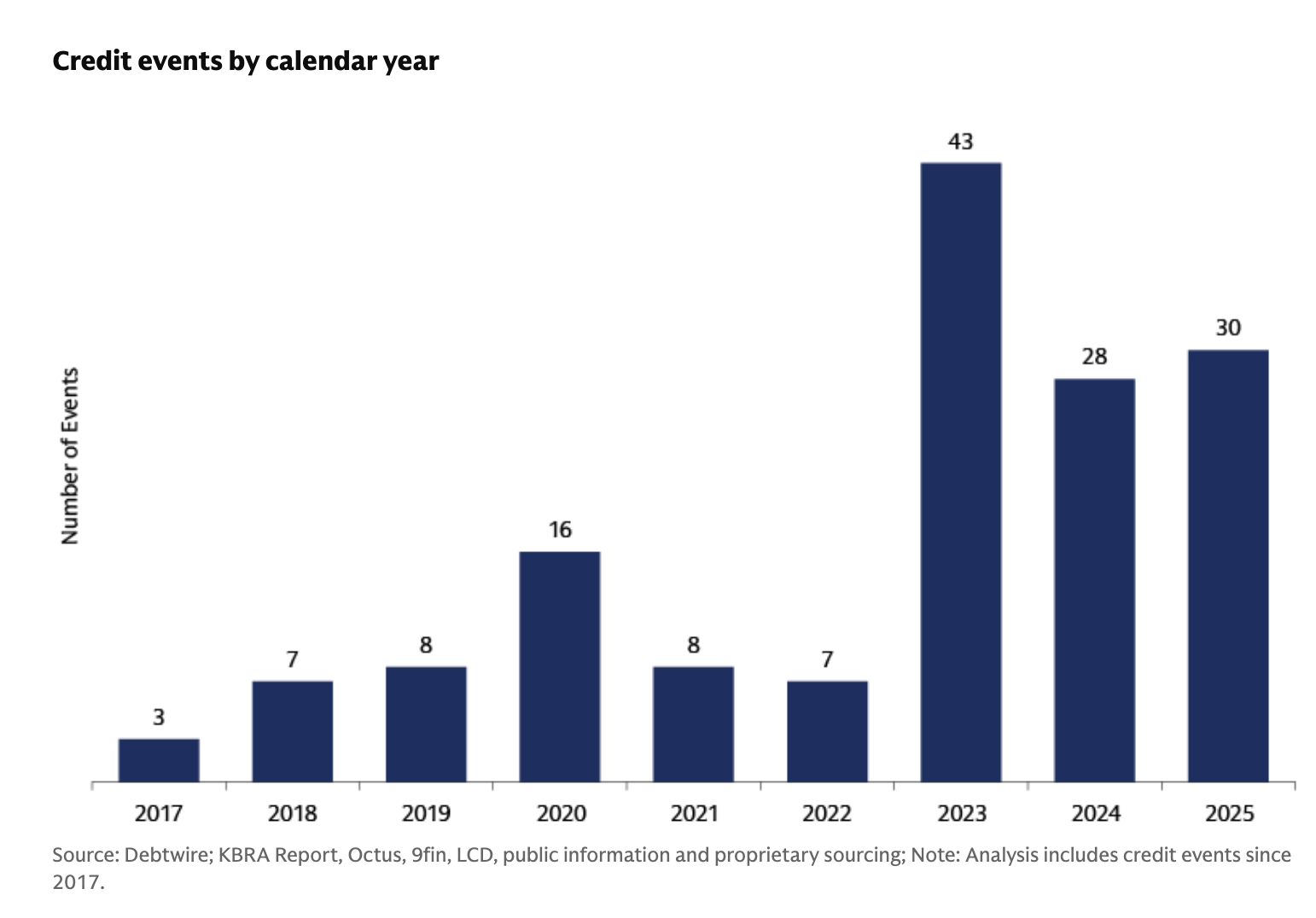

Credit events in Europe are neither random nor evenly distributed.

Instead, they reflect an evolving macroeconomic backdrop and underwriting discipline.

Stress has not been market-wide; rather, it appears concentrated in specific segments

Stress events are likely to remain elevated relative to the last decade.

Manager selection in the asset class, therefore, should matter more than it has in the past.

🎾 The Business of Pickleball: From niche to everywhere. Link

Manager Updates

Deutsche Bank is expanding its private credit offerings. Link

Apollo: The Evolution of Sustainable Credit. Link

BDC Updates

Accredited Investor Insights takes a closer look at Cliffwater Corporate Lending Fund. Link

Blue Owl recommends shareholders reject the unsolicited offer from Cox and Saba. Link

Morgan Stanley received redemption requests for 10.9% of shares. The fund will pay out the quarterly 5% repurchase cap. Link

Cliffwater received redemption requests for 13.9% of shares. The fund repurchased 7% of shares outstanding, which is the maximum amount permitted without changing the terms of the repurchase offer. Link

Partnership Updates

Bank of Ireland and Kennedy Lewis announced a €2 billion partnership to originate and jointly finance European mid‑market buyouts. Link

Dignari secured a commitment from the Abu Dhabi Investment Authority (“ADIA”) for its APAC Developed Markets Private Credit Strategy. The real estate fund will finance developers, construction companies, financial institutions, and investors in APAC’s developed markets, with a particular focus on Hong Kong. The strategy will target financing opportunities for residential, office, retail, student accommodation, serviced apartment, co-living, data centers, and logistics segments. Link

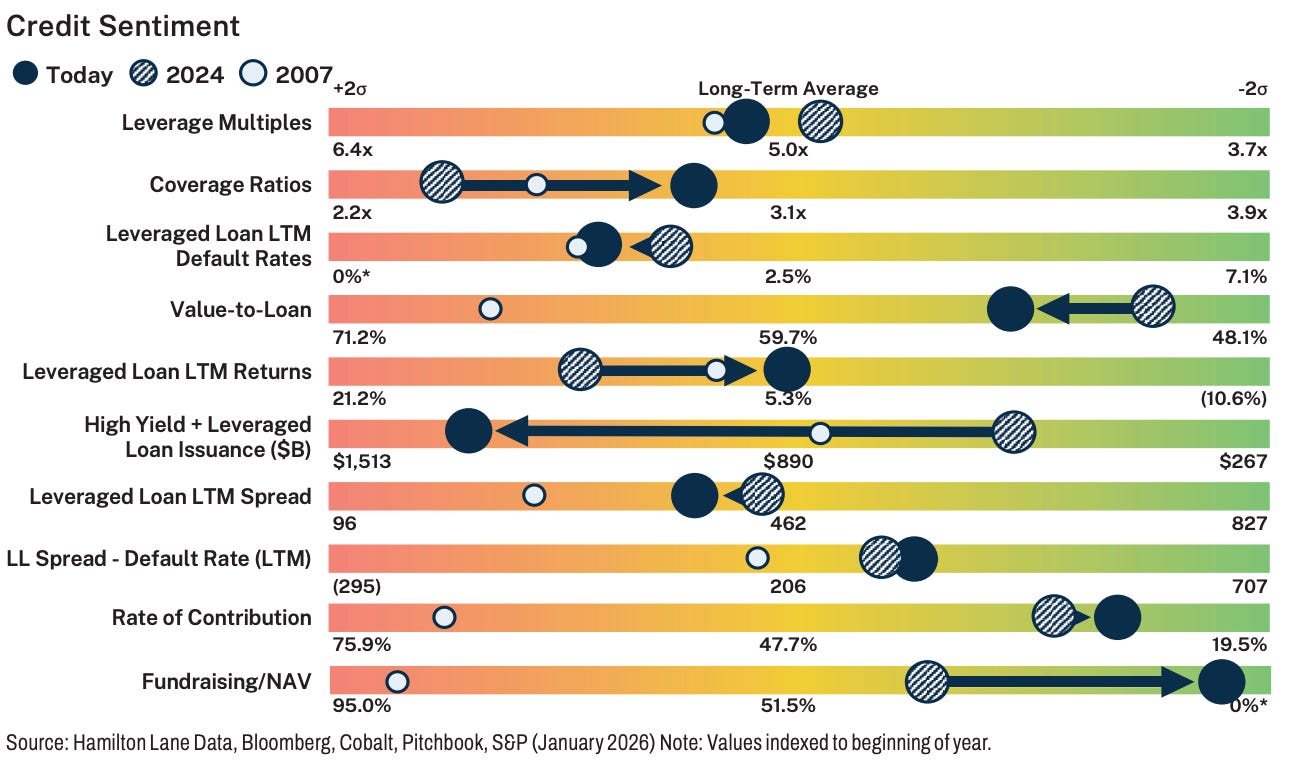

Hamilton Lane: Where Are the Signs of Stress?

If you’re looking for support for private credit, start with this year’s Hamilton Lane report.

👉 Hamilton Lane: Private credit fundamentals are solid.

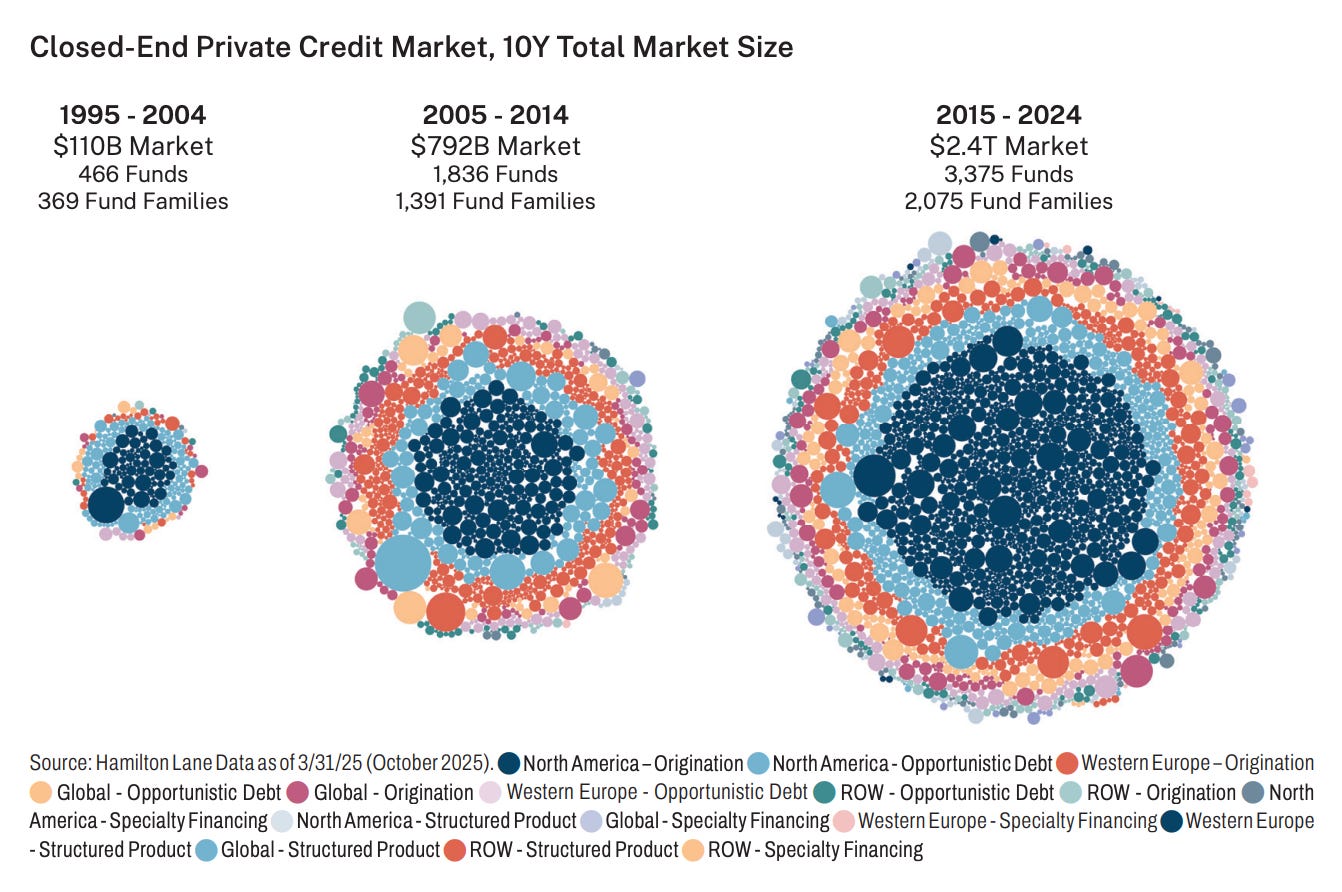

20 years ago, private credit was a cottage industry

There were only 466 closed-end funds, which were primarily mezzanine and distressed managers.

Private credit is about 24 times the market size now.

Over this time, private credit took almost 50% of the LBO financing market from the public and syndicated bank lending markets.

Let’s ask a question about that: At what cost?

Do we think the recent spate of defaults and frauds is a function of private credit actions?

With the increased capital available

With the increase in market share

With the ongoing press about the pressures on private credit

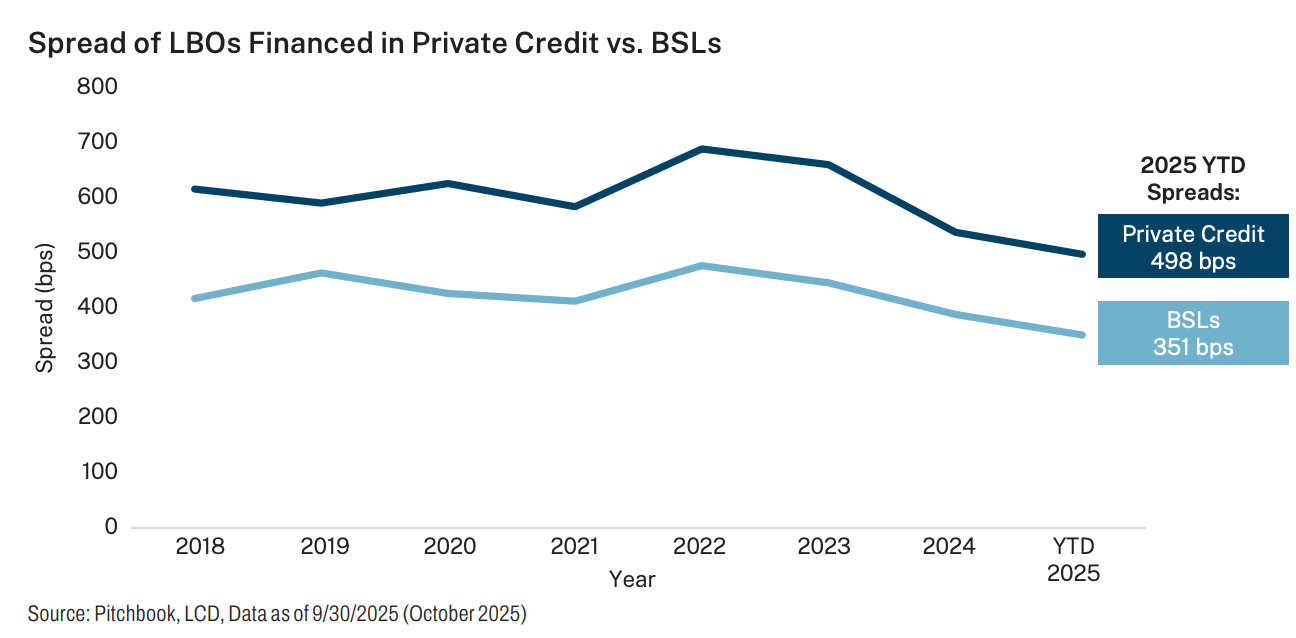

The casual observer would think that yields and spreads of private credit over broadly syndicated loans were collapsing.

That would be a completely incorrect assumption.

Sponsors want private credit and seem willing to pay for what it has to offer.

There is no sign of stress with these spreads or returns, relative to BSLs.

But let’s keep looking because we are incessantly told private credit is in a bubble.

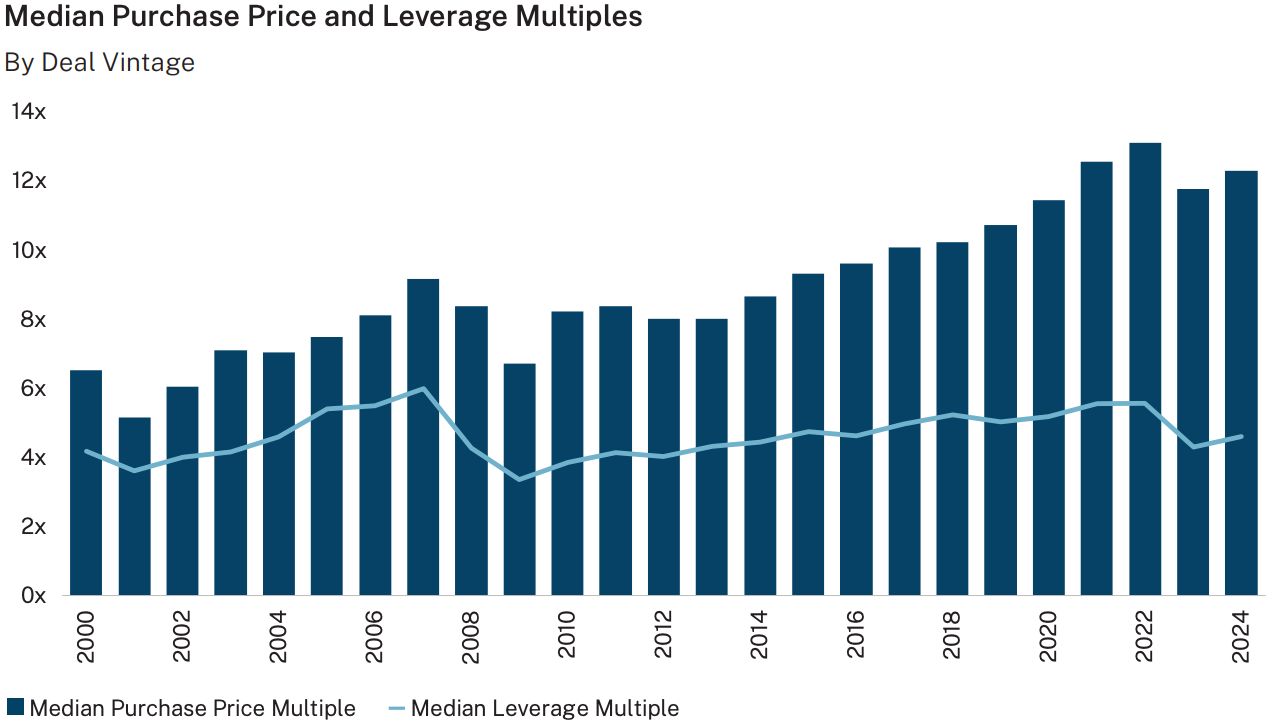

Here is one of the features of this current cycle that is different from prior cycles

As prices went up for acquisitions, leverage levels didn’t follow them up.

For all the talk of the desperate private capital providers throwing money at deals, well, they didn’t.

The equity cushion, that layer below the credit providers, is large.

Very large.

Tell us, where are the signs of stress?

Where are the signs of a bubble? Sure, they may be metaphysical, beyond the comprehension of numbers. Even there, we’re not seeing it.

Everything looks average.

Even coverage ratios are getting better.

Is it super bullish? No.

Is it super bearish with any indication of imminent danger or collapse? No. We’ll say it clearly:

Private credit is not in a bubble. If it’s not in its Golden Age, it is in its Silver Age.

💰Fundraising News

Eagle Point, a Connecticut-based private credit manager, closed its $559 million Defensive Income Fund III. The fund originates and invests in Portfolio Debt Securities, which are primarily debt securities issued by credit funds to finance a portion of their portfolios. Since the launch of the strategy in 2020, Eagle Point has originated and invested in over $8 billion of PDS across a range of credit funds, including private credit funds, closed-end funds, commercial mortgage REITs and BDCs. More here

This newsletter is for educational and entertainment purposes only. It should not be taken as investment advice.