Why NAV Pref Equity Behaves Like Credit: 17Capital’s NAV Playbook

Fundraising from Twin Brook, Castelake, Nuveen and More

👋 Hey, Nick here. A big welcome to the new subscribers from Ares, Golub, Joele Frank and Fasanara. This is the 128th edition of my weekly newsletter. If someone forwarded this to you, you can subscribe here and read my previous articles here.

📕 Reads of the Week

Must Read

If you’re a homeowner installing a new water system, a UK landlord refinancing a buy-to-let, or a CFO lining up a multi-billion-dollar facility, odds are you can borrow from Apollo. Covenant Lite on How Apollo Manufactures Credit at Megabank Scale?

Market Insights

Howard Marks writes about The Calculus of Value

🎧 Car Repossessions are Above 2019 Levels. Oaktree assesses today’s credit markets.

Deals

JPMorgan and MUFG are in talks to underwrite a $22 billion loan to build a 1,200-acre data center campus for Vantage Data Centers.

Data

Cliffwater’s Direct Lending Index – Q2 2025.

Opinions

It’s not a default if you never ask for cash, right?

🏭 Why NAV Pref Equity Behaves Like Credit: 17Capital’s NAV Playbook

Nick here. The NAV Finance market has grown nearly 4x since 2020 and accounts for nearly 10% of total private credit fundraising in 2025. 17Capital’s latest paper is one of the clearest primers on how NAV preferred equity works.

What makes this strategy so impressive?

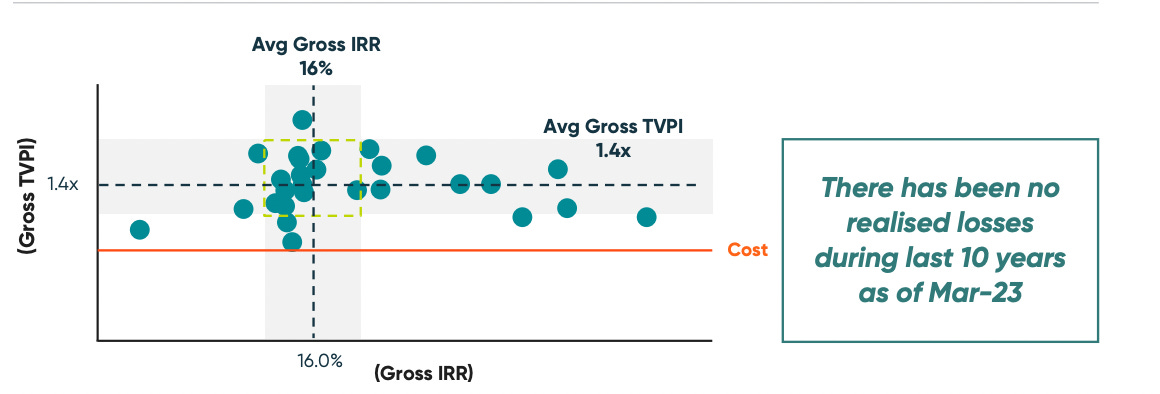

17Capital’s pref equity strategy has produced:

Mid-Teen IRRs

<4-year average payback

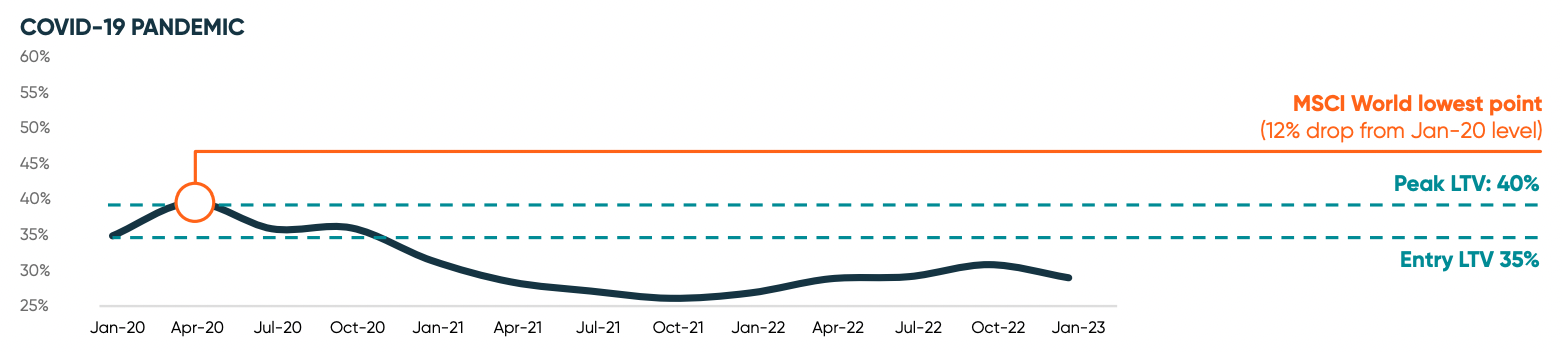

Average LTVs of 40%

Despite having borrower friendly terms:

Fixed PIK

No contractual maturity

No financial covenants

Unsecured

Below are my key highlights but you should read the full report here.

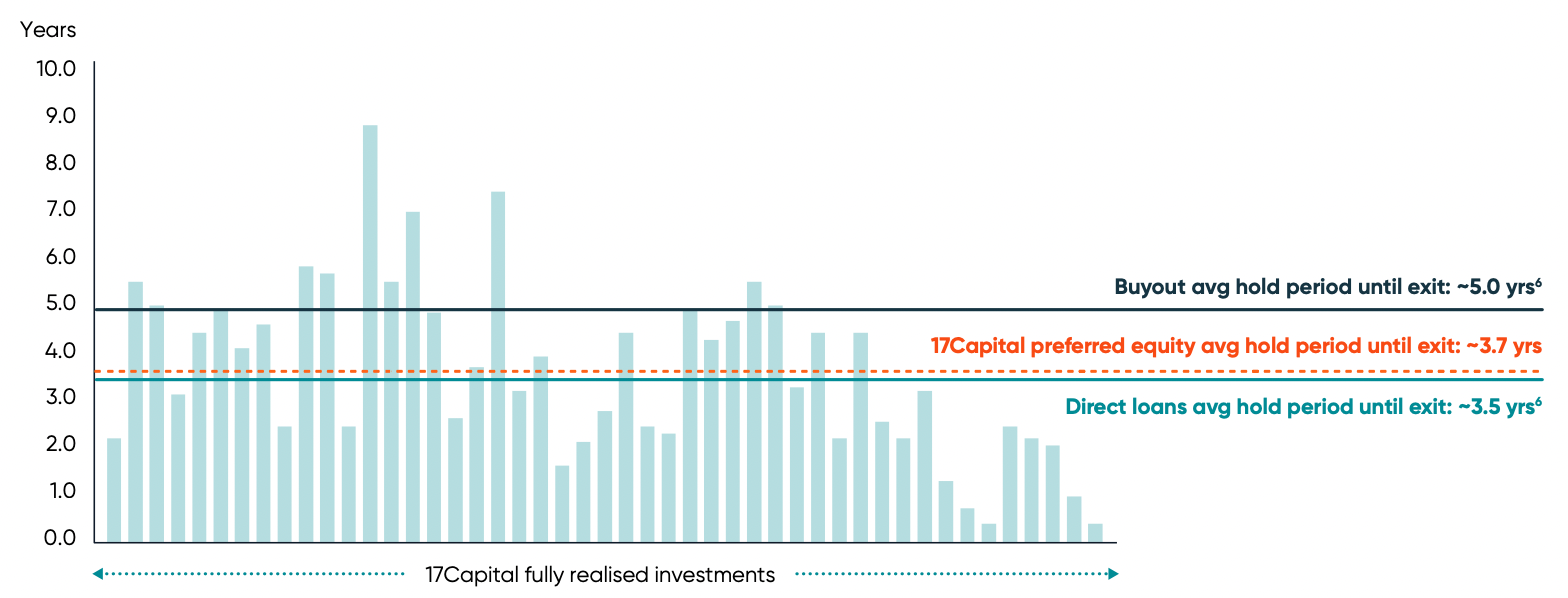

Short Duration Loans

Unlike secured credit, preferred equity has no defined maturity date.

Despite this, 17Capital’s preferred equity exit track record shows a “credit” like maturity profile with an average duration until final repayment of ~3.7 years.

This is driven by two key factors:

Borrowers are incentivized to repay by the compounding higher cost of capital.

The lender has seniority over initial cashflows until repaid, with subsequent distributions being retained by the borrower.

Mid-teen IRRs

Another key characteristic that differentiates NAV finance preferred equity is the absence of security and covenants.

The increased borrower flexibility is reflected by higher interest rates and minimum return on capital.

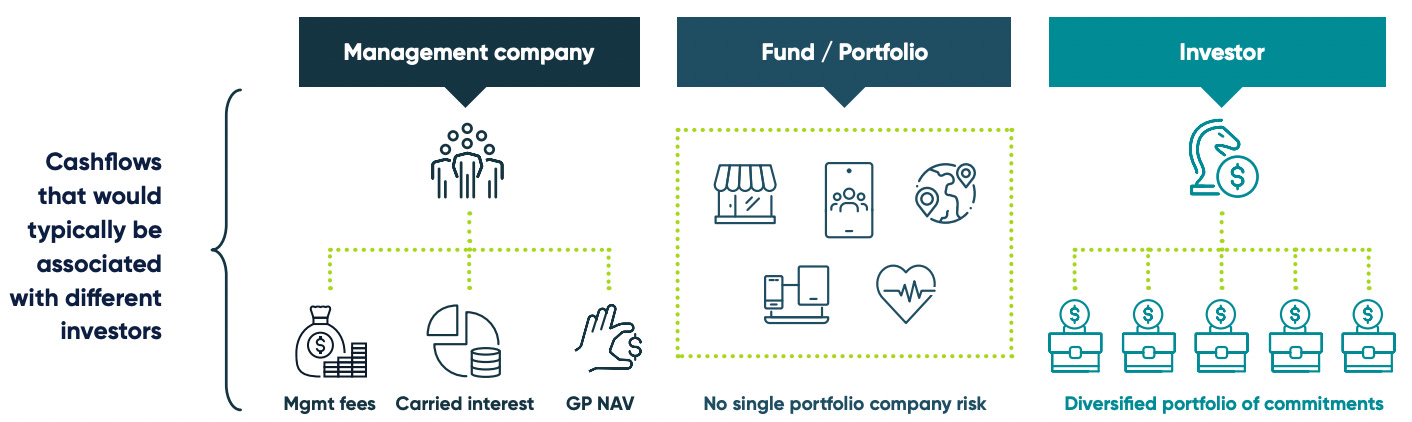

Diversified Repayment Streams

In the abscence of security, 17Capital believes the “portfolio effect” created by diversified exposures creates inherently greater “security” for the lender.

This is further supported by the low loss ratio of the strategy, which would be most comparable to the average capital loss ratio for European corporate debt of ~2% (average default rate of ~3%) and low volatility of returns.

Downside protection

Preferred equity has a contractual fixed PIK interest rate. In times of stress, the investments continue to accrue in-line with the contractual returns.

17Capital’s investment performance over the last 15 years supports a more “credit” like profile rather than equity .

LTVs peaked at 40% during the Covid-19 pandemic and the market volatility experienced in 2022.

I’ve only touched the surface of this primer. Access the Full Report to learn more.

💰Fundraising News

Middle Market

Twin Brook Capital Partners, the middle-market direct lending platform of TPG, closed its $3 billion continuation vehicle. The continuation vehicle will acquire a portfolio of floating-rate, senior secured, sponsor-backed loans from Twin Brook’s 2016 and 2018 vintage funds. Coller Capital led the transaction, which is the largest private credit continuation vehicle ever raised. More here

BC Partners Credit, the credit arm of London-based investment firm BC Partners, launched its $1.6 billion BCP Great Lakes III Fund. The fund is a joint venture between BC Partners’ private equity strategy and focuses on middle-market companies in North America and Europe. It has exclusive first right of refusal on new unitranche lending opportunities, providing the fund with a steady pipeline of opportunities. More here

ABL

Castlelake launched its new $1.8 billion aviation lending entity, Merit AirFinance. The strategy will provide debt capital to airlines and leasing companies for new and used aviation assets. More here

Sound Point Capital, a New York-based alternative credit manager, announced a first close of $1.1 billion for its Strategic Capital Fund III. The fund provides asset-based finance to US businesses. Since the strategy’s inception, Sound Point has originated more than $4.4 billion of investment activity, of which over 70% is investment-grade rated. More here

Neuberger Berman launched its first interval fund focused on private asset-based credit. The NB Asset-Based Credit Fund will invest more than 80% of its portfolio in asset-backed lending opportunities. The closed-end vehicle will offer limited quarterly liquidity through periodic repurchase offers. The fund will be managed by Neuberger’s specialty finance team and will maintain a weighted average duration of approximately 18 months. More here

Infrastructure

Nuveen, a New York-based investment manager, announced a $1.3 billion first close for its Energy & Power Infrastructure Credit Fund II. The fund finances the build-out of secure and reliable energy and power generation to companies in North America, Europe, and other OECD countries. It invests across the entire energy and power ecosystem, from renewables and energy storage to hydrocarbons, midstream, and liquefied natural gas. Nuveen is targeting a final close of $2.5 billion. More here

PGIM, the asset management business of Prudential Financial, closed its $619 million Energy Partners II fund. PEP II provides financing to middle-market upstream oil & gas and midstream companies in North America. More here

Prime Capital, a Germany-based alternative manager, announced a third close of $150 million for its Sustainable Infrastructure Debt Fund. The fund’s objective is to contribute to decarbonization, promote energy efficiency, and increase access to inclusive and modern infrastructure. It finances independent infrastructure developers in Continental Europe and the Nordics and targets a return of ~9.5% to 10.5% (gross in EUR). It is classified as an Article 9 fund under SFDR. More here

Real Estate

HDFC Capital, a subsidiary of the Indian bank HDFC, is raising $1 billion for its H-DREAM Fund, anchored by the IFC. The fund will finance projects that prioritize affordable and mid-income housing in India and will enable the development of at least 25,000 green and affordable housing units. More here

LaSalle, a Chicago-based real estate investment manager, announced it has secured $700 million for its open-ended real estate debt strategy. The strategy focuses on multifamily and multi-tenant industrial properties in growth markets and gateway cities across the US, targeting floating-rate senior loans between $25 million and $75 million. More here

This newsletter is for educational or entertainment purposes only. It should not be taken as investment advice.