It's Time to Invest in Europe

Fundraising from Goldman Sachs Alternatives, Tree Line Capital, PGIM, RedBird Capital and Weatherford Capital

👋 Hey, Nick here. If you’re new, this is the 64th edition of my weekly newsletter. Each week I write about private credit insights and fundraising announcements. You can read my previous articles here and subscribe here. Scroll to the bottom, if you’re here for the fundraising news.

📚 Reads of the week

Ninepoint suspends cash distributions on three private credit funds. Link

The rise of synthetic PIK. Link

KKR: Significant Risk Transfers: Is There Really an Endgame in Sight? Link

CalPers is bullish on private credit. Link

In case you missed it, I wrote a deep dive on CalPers Private Debt Program Here

🇪🇺 Why now is a great time to invest in Europe

While North America is the largest, most liquid, and longest-established private credit market, Europe offers a compelling opportunity. In the past six months alone, Europe has witnessed several significant fundraises:

Goldman Sachs Alternatives, $1.5 billion European Middle Market Fund below

Eurazeo’s, ~$4.3 billion Direct Lending Fund VII Link

Ardian's $5.4 billion Private Credit Fund VI.

Arcmont Asset Management’s $11 billion Direct Lending Fund IV. Link

Hayfin’s, ~$6.5 billion Hayfin Direct Lending Fund IV Link

If you’re wondering why this is, Hayfin has the answers. See the three highlights below:

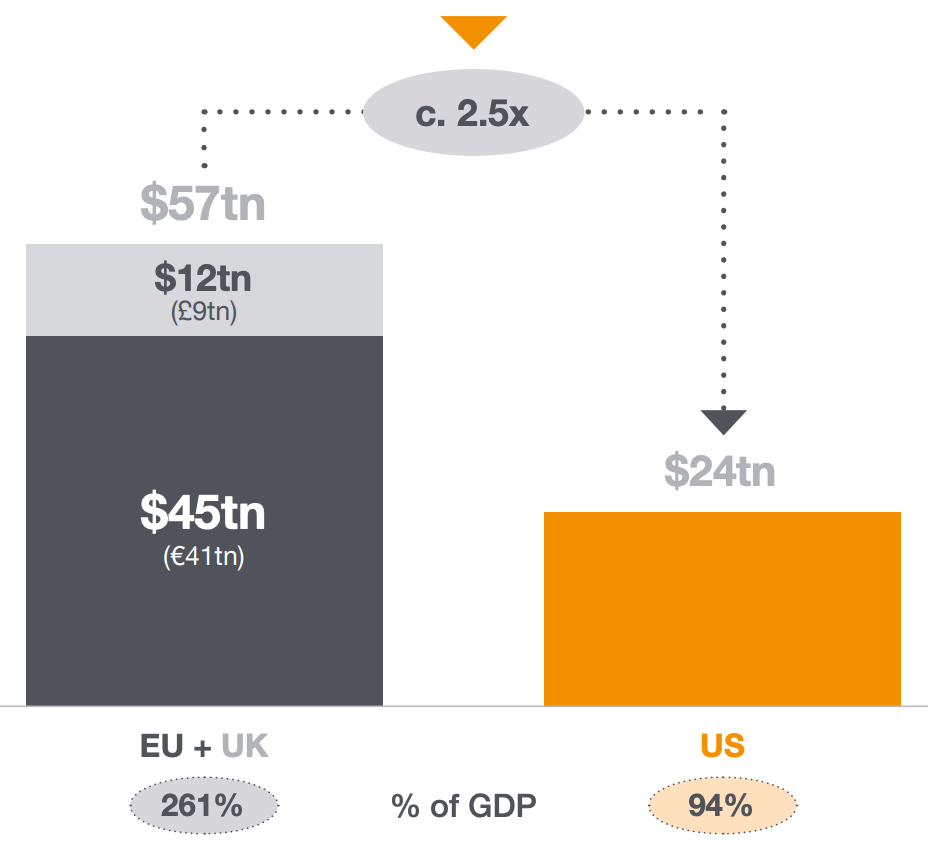

Europe’s banks have further to retrench

Europe remains a more bank-centric market than the US. The total assets held by European banks are >2x larger than their US counterparties, despite US GDP being 1.8x Europe’s.

Europe has fewer funds with scale

The European market has fewer private credit funds with the scale to underwrite the large loans that account for an increasing share of total lending volumes. This is particularly true in the upper-mid-market range.

The 25 largest managers in Europe account for 75% of all capital raised since 2007, compared to approximately 50% in the US.

Europe offers higher margins and lower leverage

Europe’s less homogeneous and less efficient market enables private credit managers to charge more at lower leverage levels.

Link to Hayfin’s full article here

💰Fundraising news

Goldman Sachs Alternatives closed its $13.1 billion flagship large-cap senior direct lending fund, West Street Loan Partners V. The fund has already invested or committed $4 billion across 37 portfolio companies. Goldman Sachs has invested nearly $70 billion in large-cap senior direct lending. This fund will be Goldman’s first Article 8 fund. More here

Goldman Sachs Alternatives closed its $1.5 billion West Street European Middle Market Credit Fund. The fund lends senior loans to sponsored middle market companies in EMEA. It targets companies with EBITDA between €10 and €50 million. Pantheon’s private credit secondaries business and Temasek invested in the fund. More here

Tree Line Capital Partners, a San Francisco-based credit asset manager, raised funds for its fourth Direct Lending Fund. Tree Line focuses on US lower middle-market companies. It lends between $10 and $150 million to companies with EBITDA between $5 and $30 million. Tree Line has committed over $5.0 billion since inception with the majority committed to companies with less than $15 million of EBITDA. Montana Board of Investments disclosed its $75 million commitment in its May Board meeting. More here and here

PGIM, the asset management arm of Prudential Financial, launched its first European Long-Term Investment Fund (ELTIF). The ELTIF will support its direct lending strategy in Europe. This strategy focuses on core middle-market lending, with the ability to underwrite sponsored and non-sponsored loans. More here

Learn more about ELTIF’s here

RedBird Capital and Weatherford Capital announced the launch of their Collegiate Athletic Solutions platform. The platform provides revenue-based lending to public and private university athletic departments across the United States. The fund reportedly plans to partner with five to ten athletic departments, offering $50 to $200 million to each. More here and here