Sixth Street: The Rise of the Factory Model

Fundraising rebounds with nearly $50 billion raised...

👋 Hey, Nick here. A big welcome to the new subscribers from Chorus Capital, AON, and Amberlake Capital. You’re now part of a select group of 2,776 subscribers. This is the 162nd edition of my weekly newsletter.

If you’re reading this on Outlook, most of the graphs won’t show. I’d recommend you read it online

📕 Reads of the Week

The conscientious manager’s biggest problem arises when too much capital is being pushed into their market and investors are too eager to put it to work.

Fundraising Updates

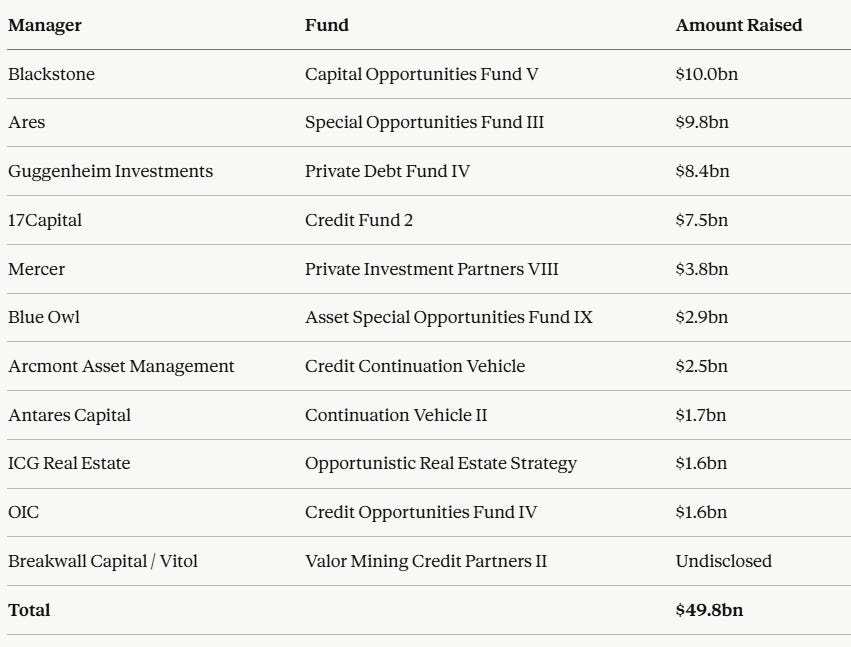

Last week’s post was tough reading but thankfully April has roared back with managers raising nearly $50 billion in first two weeks. For context, there was only $89 billion raised in the whole of Q1. Below with summary, see the full details here.

Manager Updates

🎧Promote Giving - A New Model for Performance-Driven Giving. Link

Vista Credit is launching a Tactical Credit Fund to focus on software businesses that could withstand AI-driven pressure. Link

Market Updates

🎧Alan Waxman, CEO of Sixth Street, on the History and Future of Private Capital. Link

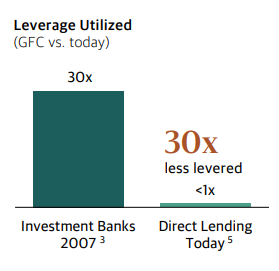

Blackstone: Today's market looks nothing like 2008

Banks then were levered 25 to 40 times, primarily funded by short term deposits and commercial paper.

The underlying assets were 90%+ loan-to-value and layered on top were highly complex derivatives that obscured the risk.

This is nothing like what is happening today.

Business development companies typically operate with less than 1x leverage, lend at roughly 40% loan-to-value to corporate borrowers, and use structures that don’t rely on deposits or overnight capital.

Partnership Updates

King Street, the New York-based manager, signed an MoU for PIF to be an anchor investor in a new private credit fund focused on Saudi Arabia and the wider MENA region. Link

Tikehau, the Paris-based alt manager, announced a joint venture with Amova Asset Management, one of Asia’s largest asset managers. Tikehau Amova Investment Management will be focused on developing Asia-focused private assets investment strategies for global distribution. The joint venture will include offering private credit focused on Asia. Link

BDC / Interval Fund Updates

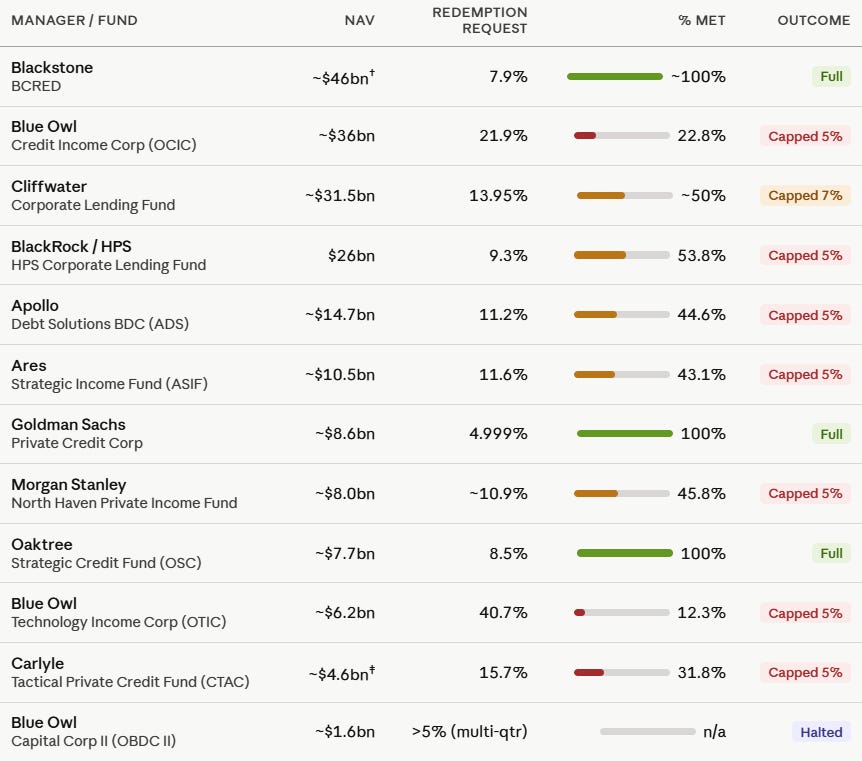

Moody's Reaffirms Blue Owl’s OCIC rating but changes outlook to negative.

The change in outlook to negative is in response to OCIC’s significantly higher-than-peer redemption requests in the first quarter.

OCIC reported net debt-to-equity leverage of 0.8x, which is lower than the peer median and $11 billion in cash, revolver capacity and Level 2 investments, which together could more than cover the full first-quarter redemption request.

In addition, OCIC has relatively limited unsecured debt maturities coming due over the next 12 months, consisting of $350 million in senior unsecured notes due in September and $500 million due in February 2027.

Deterioration in leverage or liquidity could weaken the company’s relative strengths at its Baa2 rating, which is at the top of the BDC peer group.

The headlines are much louder than the spreads

The Rise of the Factory Model

Alan Waxman, co-founder and CEO of Sixth Street, appeared on Invest Like the Best. Below are my key highlights.

👉Listen to the interview here.

Everything that is covered in the media is just talking about the symptoms and not actually getting to the root cause.

The SMA was a symptom.

The wealth system is a symptom.

When you think about some of the stuff you see in stuck private assets, where there’s so many assets around the world in private real estate, private infrastructure, private equity, that literally were companies or assets that were bought in post-COVID, in sort of ‘20, ‘21, early ‘22 – paid way too much. They’re stuck assets.

All that stuff is symptoms.

The root cause of this is the change of behavior patterns of the factory model. That’s the root cause.

The Rise of the Factory Model

So the way that we define the factory model in our industry is there’s two parts to it and then there’s an output.

First part is the industrialization of the fundraising process. Say liability gathering. Literally raising as much capital as you possibly can, as fast as you can. So that’s the industrialization of the liability side of the fundraising side. That comes first.

And then what comes second is then, as a result of that, the industrialization of the asset side. So think about investing. If you’re on an investment team and all of a sudden your firm has a lot of money to invest, and it’s just sitting there and maybe there’s a timestamp on it. All of a sudden your behavior has to start to change, because you have to deploy that money much quicker.

And what’s the best way to raise a lot of capital quickly?

Make it very simple.

Make it very narrow, because if it’s wide, that’s too hard to explain.

So you want to make it as narrow as possible and you’re also willing to take – let’s say, make concessions on the type of capital you raise. Meaning maybe it’s got a term where they can ask for your money back.

When people hear this, they’re going to think I’m only talking about the bigger firms

But it filtered down to mid-sized firms, smaller firms for a whole bunch of reasons, but this whole factory model behavior started to reveal itself in 2018…

The story of the factory model starts to correspond with FRE multiples. Our industry started trading between 10 to 15 times FRE in early 2010s. In 2018, when all this started, it stepped up to – call it 15 to 20 times, obviously depends on the comp set. Before this current moment, we’re at 25 to 30 times plus. That’s where it is

You know when you see it.

You can see it in the underwriting. We're in a bunch of different asset classes. You can see it, particularly if you're a fixed income investor or credit investor because you have capped upside. There's terms you just don't give. A lot of those terms have been given.

You should not do those terms, because it’s all good when you’re in a procyclical environment. But if you have capped upside and you’re earning a 10% return and all the collateral that your 10% is based on can literally be taken out of your collateral package overnight.

Or for that 10% return, you can be levered up because let’s say there’s an AI disruption and some software company needs to reposition their business and they can basically lever you up. So you go from 50% loan to value to 120% loan to value.

Those are just things that you shouldn’t do for a 10% return.

There’s No Such Thing as Semi-Liquid

Some of the factory models that are out there have raised capital from the wealth channel in irresponsible ways. So first of all, in general, you’re taking an illiquid asset and you’re giving investors an ability to get their money back quarterly. They say semi-liquid. There’s no semi-liquid, okay, there’s no such thing as semi-liquid. Anyone that’s an investor that’s been through a bunch of cycles – there’s liquid, and then there’s illiquid.

Because again, going back to the history of the wealth channel or individuals or retail, the one thing we know, it’s very procyclical. We’re in a procyclical environment. It’s easy to raise money. And when you’re not, and when there’s problems or dislocation like there is today, they want their money back. So you basically had mismatching of illiquid assets and liabilities. So that’s one part of it.

The second thing is that they would raise these very narrow – what I mean by narrow is it’s just direct lending. So it’s not like you can invest in direct lending and real estate and infrastructure or in asset-based finance. No, no, it’s just very narrow. Just direct lending or just asset-based finance or just this strategy. That’s a narrow strategy.

And maybe that’s okay if you raise the right amount of capital. But if you raise an unlimited amount of capital where your investing is dictated, not on good investments in the market, but basically dictated by how much money you can raise. There’s never a governor on how much money to raise.

And the thing about these wealth vehicles, when they raise it, they have to invest it right away. We call it inflow investing. They have to invest it right away. So they raise as much money as they can, and if they don’t invest it right away, it dilutes the return of that vehicle.

The best answer is a market mechanism, like you have with institutional investors.

If you do irresponsible things or you're not a good investor, if you change your business model, they're going to punish you by not giving you money for your next fund.

What’s your clarity of purpose?

Does that stay consistent over time?

Is your clarity of purpose to raise a bunch of liabilities or is it to drive good returns for investors?

Maybe it’s both. Maybe you can do that. Maybe some firms can do that.

But, what is your clarity of purpose is something we talk a lot about at Sixth Street, is that if you look at all the great companies that have been around for a long time, they got one thing right. They never forgot what their purpose was, which is to serve their customers.

It’s enticing to raise a bunch of money. It’s enticing once you raise it to invest a lot of money. That doesn’t mean that you have to do it.

Sixth Street, we’re a multi-strategy private capital firm. We do a bunch of things. One of the things we do is direct lending. We have one of the best track records. We’ve been here longer than – in direct lending, I started the direct lending business in 2001 when there was only two of us.

So we’ve watched this and we could have gone to the wealth channel and raised all the same vehicles because of our track record. And we have – you know how many dollars of perpetual private BDCs we have? Exactly zero. It’s not that we couldn’t have. We just didn’t think it was the right thing and we didn’t think it was consistent with our clarity of purpose, and that’s why we didn’t do it.

It’s easy to get FOMO.

I just think you just got to block out that noise and it always comes back to first principles of clarity of purpose. What are your values? And if you stay consistent with that, judging by the best companies that have been around for a long time, that’s your pathway to building a great company that’s going to be here for a long time, not short-termism.

Four Reasons Why Howard Thinks Oaktree will Outperform

Superior investing doesn’t result from omniscience and perfect decision making, but rather from decisions that are better than those made by others.

We’ve been investors in high yield bonds and broadly syndicated loans since their inception decades ago, but we never went overboard in private credit. As I mentioned a year ago in my memo, Gimme Credit, whereas for a few years the most popular question has been “can we talk about private credit?” my rejoinder has been “can we talk about credit?” We insisted there was a place in portfolios for both private credit and liquid credit.

We never pursued direct lending to the same extent as others. At the beginning of its existence in the early 2010s, we thought the returns from direct lending, while high in relative terms, were low in the absolute. And later, we thought the superiority in pricing and terms had been competed away by the newly arrived managers and capital, rendering it average in attractiveness, not exceptional. Private credit represents well under half of Oaktree’s performing credit assets, and direct lending represents less than half of our private credit book. Thus, direct lending is only around 20% of Oaktree’s investments in performing credit and less than 15% of our overall assets under management.

Since (a) we expanded our assets far less than many other alternative credit managers (Oaktree’s AUM “only” doubled over the last decade) and (b) direct lending was a limited part of our AUM growth, we’ve felt less pressure to invest quickly or compromise our standards. That meant we could remain highly selective, limiting the amount invested in software and restricting it to what we believe to be the best opportunities. Most of Brookfield/Oaktree’s private credit funds operate outside of direct lending and thus have only limited holdings in software.

80% of Oaktree’s total investment in private credit is on behalf of institutional clients, meaning very little was placed with the public. While the leading managers of public direct lending vehicles have $40-50 billion or more there, we have just over $10 billion.

👉 Read Howard’s full memo here

💰Fundraising News

Opportunistic

Blackstone closed its $10 billion Capital Opportunities Fund V, its largest opportunistic credit fund raised to date. Blackstone’s opportunistic credit strategy has generated a 13% net IRR since inception in 2007. More here

Ares closed its $9.8 billion Special Opportunities Fund III. The fund provides private debt, equity and hybrid solutions that fill the gap between for-control private equity and more traditional corporate lending, while also opportunistically purchasing stressed public corporate credits. Since inception, the strategy has deployed over $17 billion and generated over $11 billion of realized proceed. More here

Blue Owl closes its $2.9 billion Asset Special Opportunities Fund IX. The fund employs a flexible mandate with the ability to allocate dynamically throughout changing market conditions. More here

Direct Lending

Guggenheim Investments, a New York-based manager, closed its $8.4 billion Private Debt Fund IV. The fund sources first lien senior secured loans in both sponsor-backed and non-sponsor-backed companies within the US core middle market. Guggenheim currently serves as the lead investor on over 90% of the capital invested by PDF IV and is the sole investor on 35% of invested capital. More here

Real Estate

ICG Real Estate, the real estate division of London-based manager, ICG, closed its $1.6 billion Opportunistic Real Estate strategy. The Portfolio comprises of approximately 100 assets on long-term, inflation-linked leases. It offers investors access to opportunistic returns within the European Industrial and Logistics sector, with assets typically sourced off-market through non-traditional routes, including proprietary sale-and-leaseback transactions with corporates. More here

Secondaries

Antares Capital, a London-based manager, closed its second continuation vehicle with over $1.7 billion in commitments. The transaction was led by Ares Credit Secondaries funds. The fund was established to purchase assets from a closed-end private credit fund comprising over 300 underlying first-lien, floating-rate loans. More here

Arcmont Asset Management, a London-based private credit manager, closed its $2.5 billion credit continuation vehicle. The transaction was led by Ares Credit Secondaries. The CV acquired a portfolio of largely first-lien senior secured loans from Arcmont’s 2019 vintage, Direct Lending Fund III. More here

Other

17Capital, a London-based NAV lender, closed its $7.5 billion Credit Fund 2. According to PitchBook, Credit Fund 2 represents the largest NAV loan fundraise. The fund provides NAV loans to well-established private equity funds across the U.S. and Europe. Since launching its dedicated NAV loan program in 2020, 17Capital has deployed more than $7.5 billion across 30 NAV loans, including $2 billion already deployed from Credit Fund 2. More here

OIC, a New York-based manager, closed its $1.6 billion Credit Opportunities Fund IV. The infrastructure fund invests in middle-market infrastructure. OIC’s target investment sectors include transportation, storage & logistics, digital infrastructure, renewable power and fuels, waste & recycling, energy efficiency and other infrastructure. More here

Mercer announced its $3.8 billion Private Investment Partners VIII. The fund offers investors access to a spectrum of global private assets across private equity, private debt, infrastructure, and real estate. PIP consists of a US vehicle for US investors (Onshore) and a Luxembourg vehicle for non-US investors (Offshore). The funds invest across primaries, co-investments and secondary opportunities. More here

Breakwall Capital, a New York firm specializing in the energy industry, and Vitol, a leader in energy and commodities, closed their Valor Mining Credit Partners II. The fund makes structured credit investments in mining and critical minerals companies. It primarily targets event-driven financing opportunities, including debt refinancing, acquisition financing, and development capital. In less than three years, the Valor energy credit franchise has invested over $2.1 billion to support the upstream oil & gas, mining, and critical minerals sectors. More here

This newsletter is for educational and entertainment purposes only. It should not be taken as investment advice.

Always great read!