The State of Private Credit in Q1 26

Fundraising Slows as Capital Concentrates at the Top

👋 Hey, Nick here. A big welcome to the new subscribers at 5C, Robeco, and Axos Bank. This is the 161st edition of my weekly private credit newsletter, and you’re now part of a select group of 2,760 subscribers. You can read my previous articles here and subscribe here.

If you’re reading this on Outlook, most of the graphs won’t show. I’d recommend you read it online

Private Credit’s Tough Reality

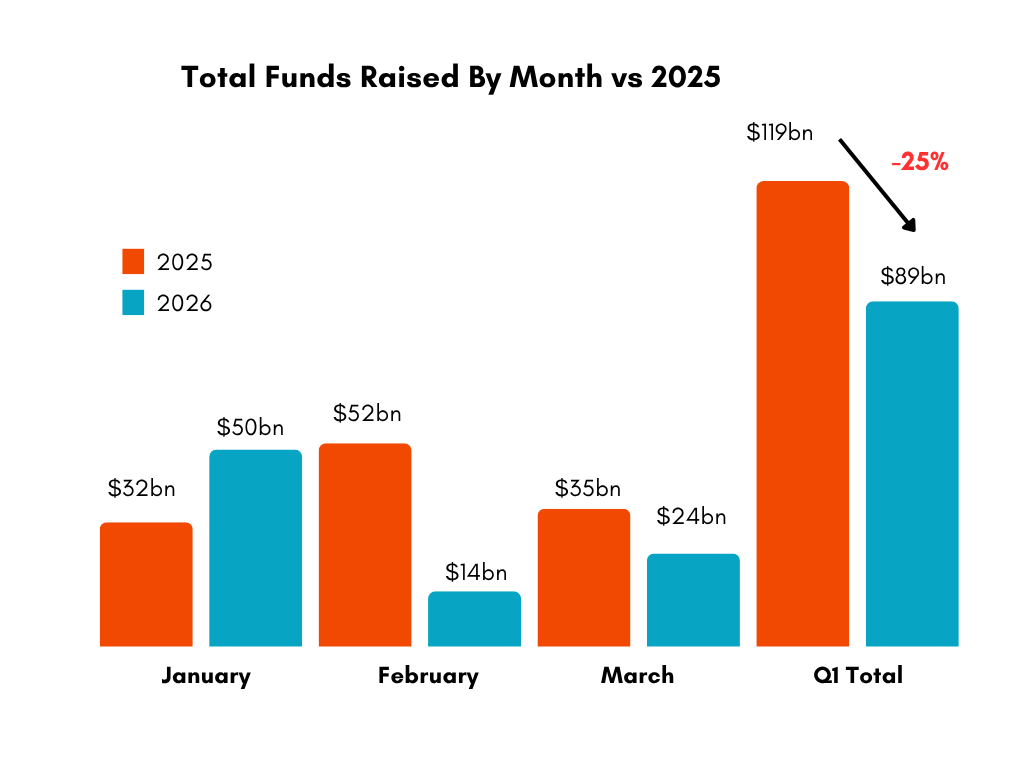

There’s no sugar-coating it. The fundraising environment has taken a noticeable turn for the worse. Fewer funds came to market, and those that did were smaller, with average fund size down nearly 10% year-on-year.

Number of funds raised: 51 (DOWN 18% YoY)

Total amount raised: $89 billion (DOWN 25% YoY)

Number of Countries where funds were raised: 11 (DOWN 21% YoY)

Lending money isn’t hard. Getting repaid can be hard. The managers who understood that during the very good times are the ones who will stand out now in this less certain environment.

Asia is the Growth Story 🌎

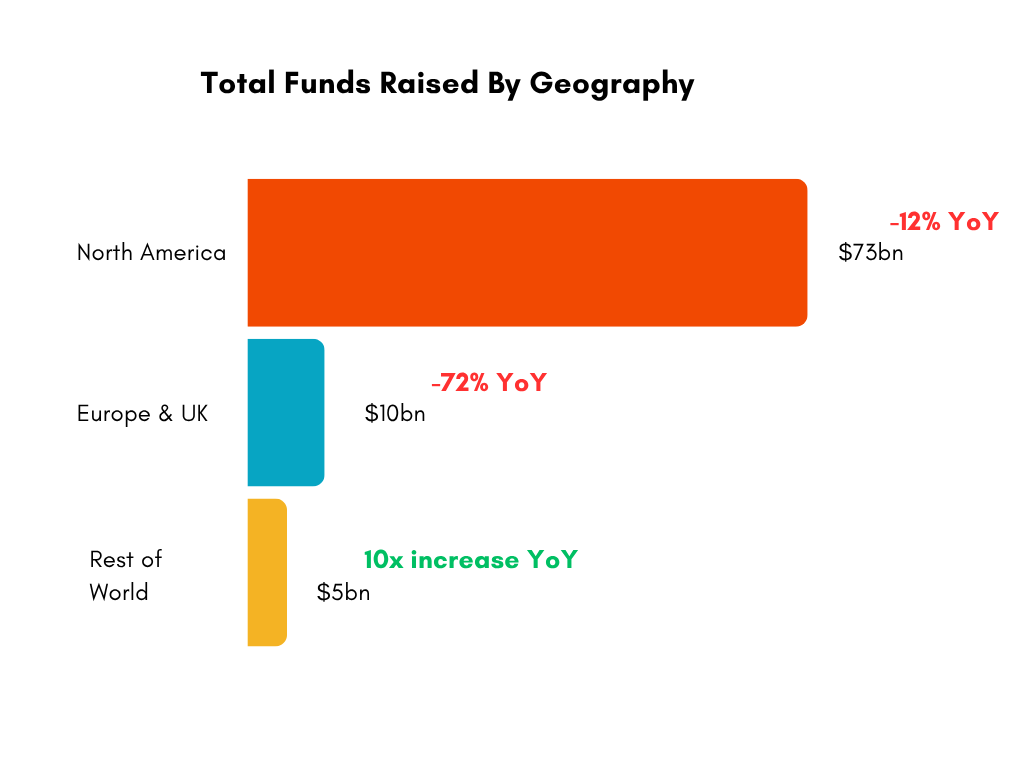

Asian private credit fundraising surged, with fundraising growing 10x year-on-year. While KKR’s latest $2.5bn Asia fund accounted for half of this, a growing number of managers are expanding their presence in the region. This momentum is being reinforced by partnerships, such as Citigroup’s collaboration with Blackstone, Blue Owl, and KKR.

Europe’s 70% decline is exaggerated by the absence of mega-funds this quarter. Last year, Ares raised $17.6 billion for its Ares Capital Europe V. Excluding this, the decline is closer to 40%

We’re taking this strategy global. When you think about why we were just in Japan, when you think about the Industrial Renaissance and that part of the globe, Asia Pac, along with how we’re focused on Europe, the answer to your question, big picture, is we’re going to take a very successful strategy of integrating origination to every aspect of our business.

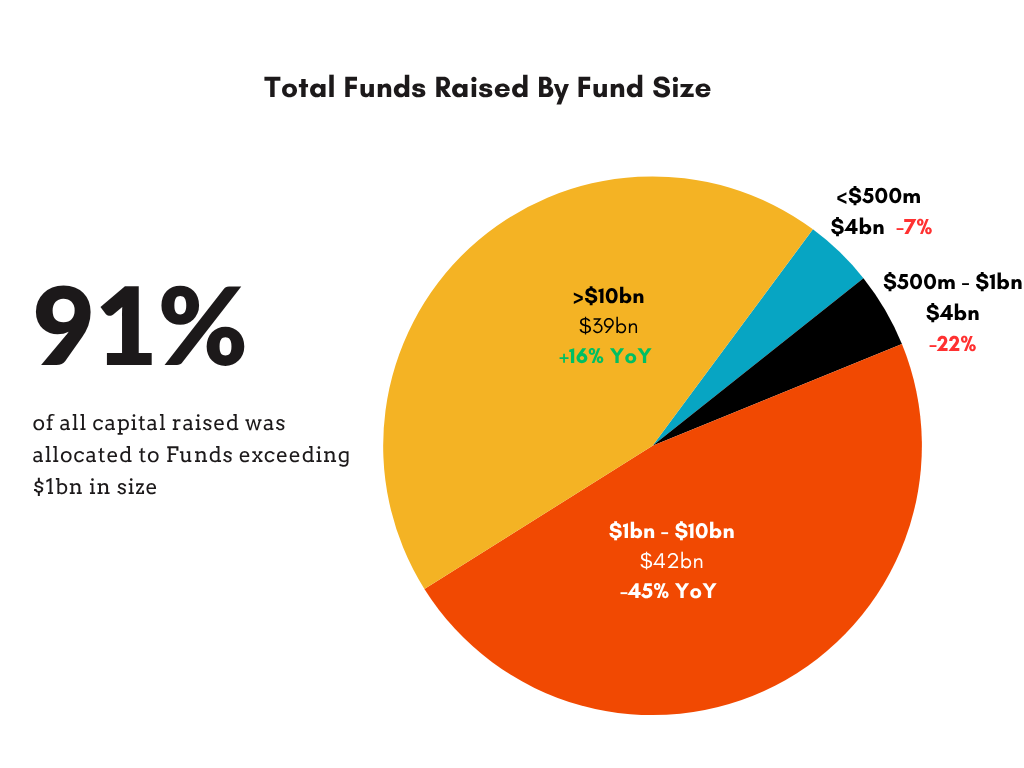

The Five Largest Funds Raised 60% of the Capital…

Churchill Asset Management’s $16 billion Senior Loan Strategy

Benefit Street Partners $10 billion Real Estate Opportunistic Debt Fund II

The Middle is Getting Smaller…

👉 This is the single most important takeaway this quarter: capital is concentrating at the top.

The average fund size for the top 5 managers is relatively stable:

$10.6bn (2024)

$11.0bn (2025)

$9.7bn (2026).

The mega-managers raise the same amount of capital regardless of market conditions.

Everyone below these managers is under pressure. The average fund size for these dropped from $1.1bn to $0.9bn, and total capital raised has halved—from $64.3bn in Q1 2025 to $32.3bn in Q1 2026.

This is where the real dislocation lies. If you are a GP ranked outside the top 5, your available LP capital pool shrank by roughly 50% in twelve months.

📕Nick’s Top Articles for Q1

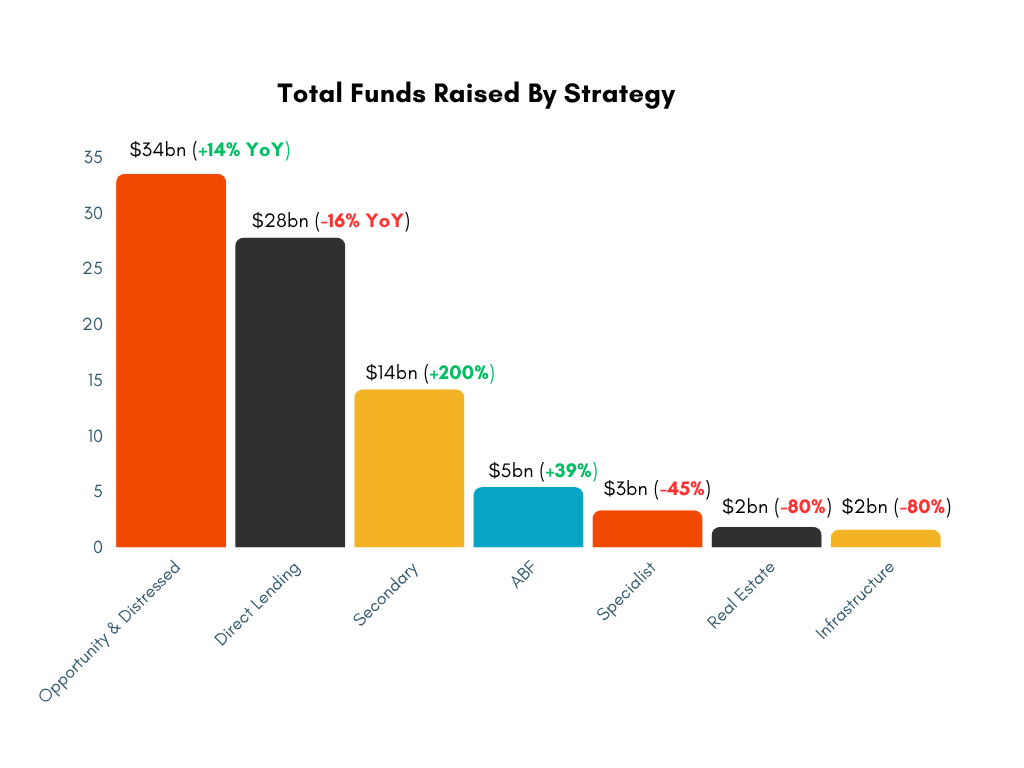

Opportunistic Overtakes Direct Lending

Opportunistic capital surpassed direct lending for the first time on record with fundraising doubling over the last two years. Not only did they raise more, Opportunistic funds were also 70% larger than other strategies. Goldman’s $13bn mezzanine fund and Benefit Street’s $10bn CRE opportunistic fund were the standout funds.

For more on this trend, see Dispersion Is Back

Credit secondaries volume has set new highs every year post 2020. Credit secondaries fundraising tripled year-on-year, with Ares $7 billion raise leading the way.

For more on this trend, see The State of Private Credit Secondaries.

Direct Lending’s decline continues with 40% fewer funds raised YoY. Direct Lending accounted for 33% of new fundraising vs 66% in 2024. Churchill’s $16bn fund shows that mega-managers can still raise. The problem is for mid-market managers ($500m-$5bn). These funds raised 60% less YoY.

🏆 Nick’s Funds of the Quarter

During “risk off” periods, when risk premiums are attractive, both capital and liquidity leave the system. This is wrong-way risk for both the capital and manager

🗄️ Brigade Capital’s $1 Billion Inaugural Private Credit Fund

In contrast to broader trends, Brigade raised its inaugural direct lending private credit fund. The New York-based manager will finance lower-to-middle market and non-sponsored borrowers.

⛏️ Orion Resource Partners’ $2.2 billion Mine Finance Fund IV

Orion, a New York-based manager, completed its largest ever fundraise. The fund finances the construction and acquisition of strategic metals and critical mineral assets. The fund is already 61% committed across a portfolio of projects, spanning North and South America, Europe, Australasia, and Africa.

🦒 XSML Capital’s $142 million African Rivers Fund IV

The fund finances SMEs in African frontier markets with loan sizes between $300,000 to $10 million. Investments to date are concentrated in the DRC (47%), Angola (22%), Uganda (17%), and Zambia (14%), across manufacturing, retail, beverages, food processing, and the pharmaceutical sector.

This newsletter is for educational or entertainment purposes only. It should not be taken as investment advice.