The State of Private Credit in H1 2026

Don’t Trust the Headlines, Focus on Fundamentals

👋 Hey, Nick here. A big welcome to the new subscribers at Chicago Atlantic, Fitch Group, and Kirkland & Ellis. This is the 173rd edition of my weekly private credit newsletter, and you’re now part of a select group of 3,123 subscribers. You can read my previous articles here and subscribe here.

If you’re reading this on Outlook, most of the graphs won’t show. I’d recommend you read it online

“Watch the flows…

The interaction of pools of capital, along with inflows and outflows, drives the supply and demand balance...The universe is ruled by supply and demand.

Watching the flows is looking through the telescope”

That line from Ares’ Alternative Credit is one I often think about when writing these quarterly pieces.

It’s easy to get pulled into media narratives, anecdotes, individual portfolio workouts, or whatever controversy is dominating the week. Taken together, they often leave us with a distorted view of the overall market.

So once a quarter, I try to step back and look through the telescope: where is capital really flowing?

That means analysing every fundraising announcement I’ve tracked during the quarter. The dataset is not perfect, but it is good enough to reveal the bigger picture. If you think the conclusions are wrong, I’d be happy to be challenged.

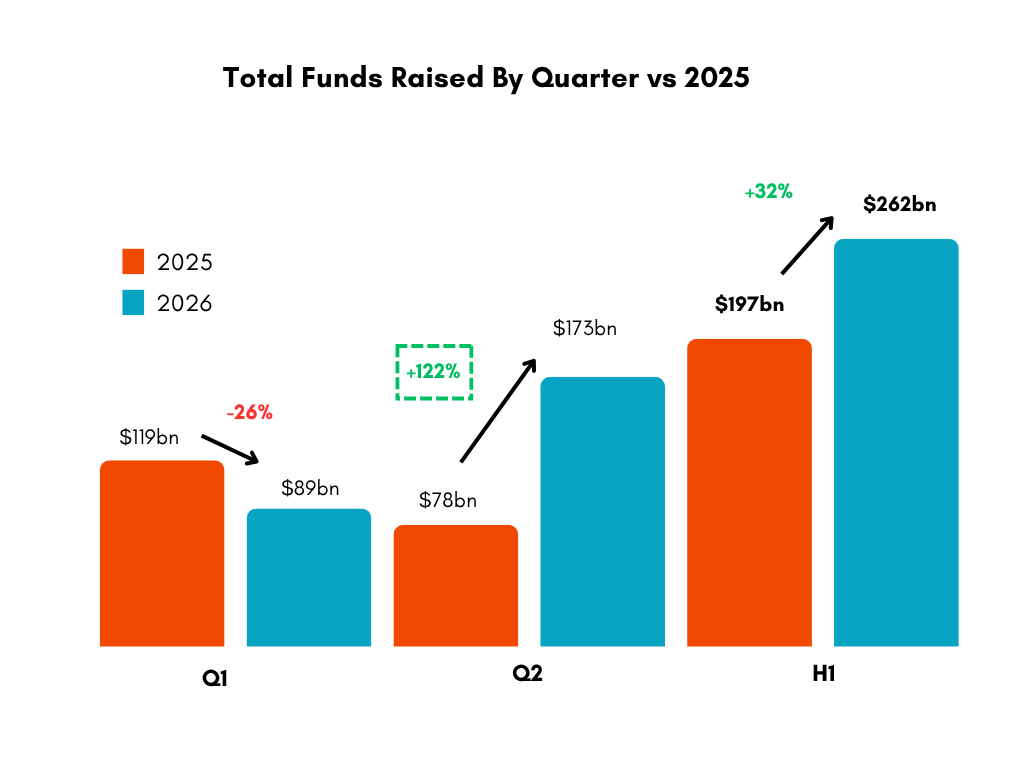

Redemptions have dominated the conversation for the past six months

It feels like everyone has been so focused on redemptions that we forgot the other side of the equation, fundraising.

Private credit managers raised $262 billion in H1, 30% more than last year. That was not the outcome I expected given how poor Q1 was. The growth was entirely driven by Q2, when managers raised $173 billion, accounting for nearly 70% of H1 fundraising.

Stepping back, several recurring themes continue to stand out:

Fewer funds are raising in the market.

The largest managers are taking most of the capital.

Credit secondaries set all time highs.

Asia continues to outperform.

But there were also a few surprises:

Fund sizes are getting larger.

Direct lending is back.

Europe is declining.

Let’s look at each of these in more detail.

History does not punish optimism. It punishes the absence of preparation and discipline.

Both conditions can exist in the same market, and that is the lens through which we are approaching this note.

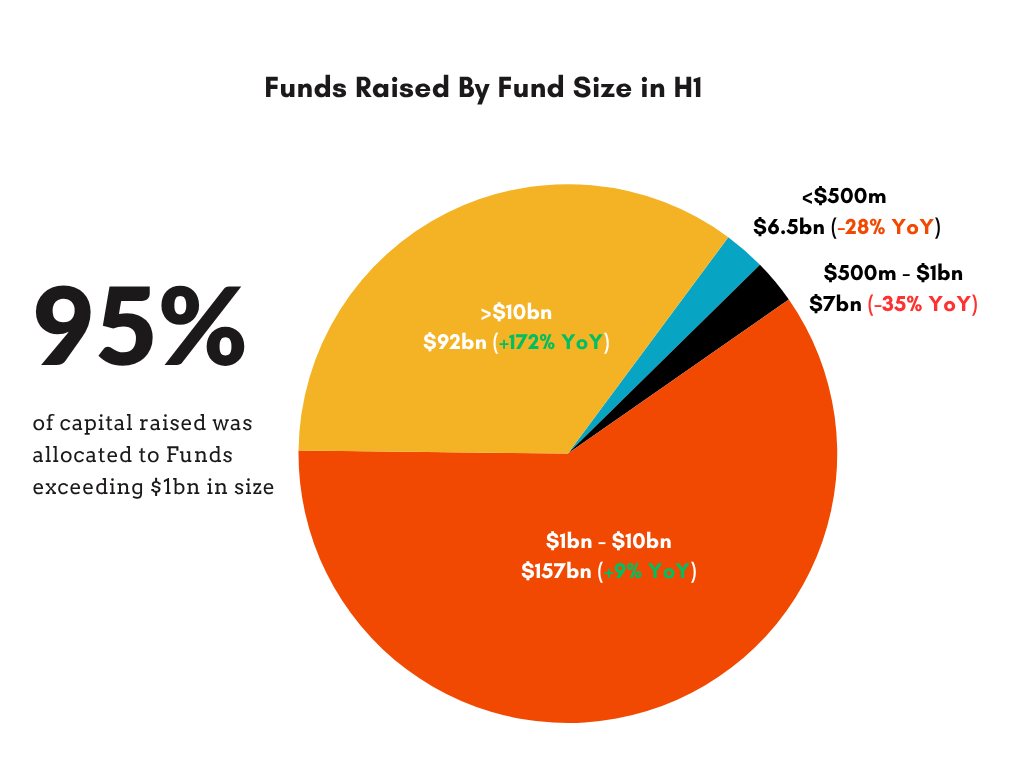

Capital is concentrating at the top.

👉 This continues to be one of the most important takeaways

The average size of the top 5 funds has grown every year for the last 3 years.

$10.6bn (2024)

$11.0bn (2025)

$14.3bn (2026).

Despite all the redemption noise, mega-managers are raising larger funds than ever before. More strikingly, there were three times as many funds above $10bn as there were last year.

At the other end of the market, smaller funds are struggling. The number of sub-$1bn fundraises fell 40% year-on-year, and the capital raised by those funds declined 30%.

This is best shown in the graph below. Capital concentration has reached the highest level I’ve recorded. In short, LPs are focusing on the largest managers.

To understand why capital is concentrating around the largest managers, it’s worth listening to Alan Waxman on Invest Like the Best and reading WTF Is Going On In Private Credit? Both help explain the rise of the factory model.

Nobody’s abandoning private credit.

Institutions will continue to stay the course, and private credit will prove itself to be very resilient.

The Top 10 Funds Raised 60% of the Capital…

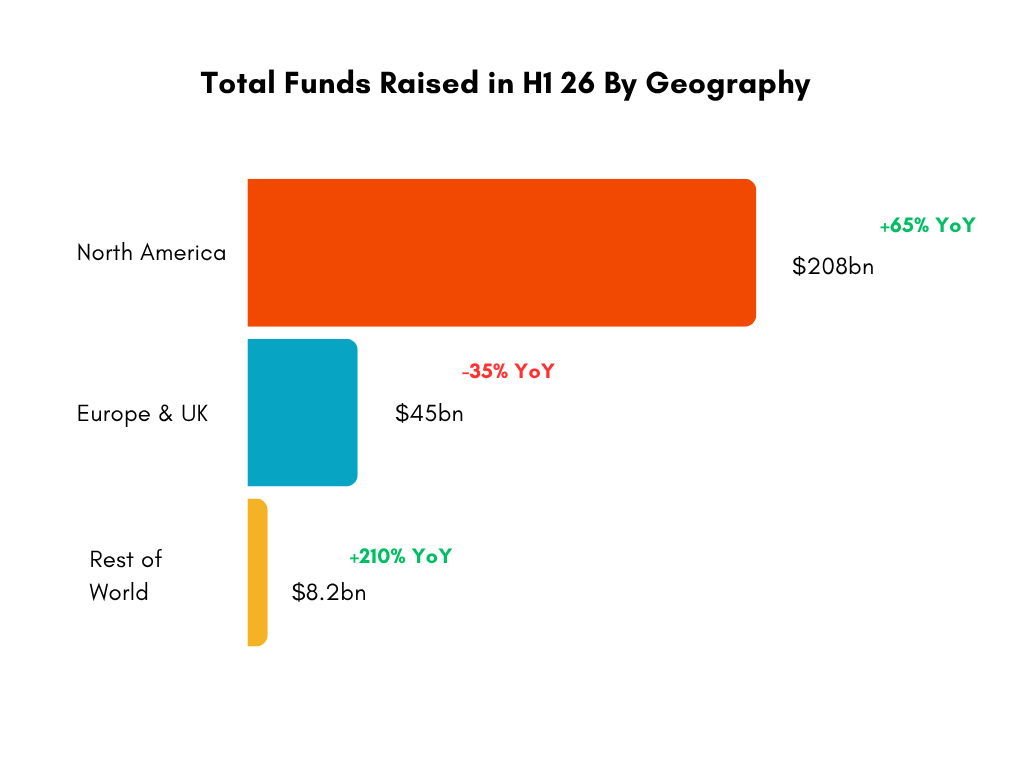

The US took a record share of capital

North American funds raised 61% of the capital in H1 2026, up from 52% a year ago and reaching the highest market share I have ever recorded. The concentration was mainly driven by the mega-managers.

Every one of the $10 billion+ vehicles was raised by a US manager.

European fundraising, meanwhile, fell 35% YoY, a massive retreat for a region that has been a steady third of the market.

Asia continued to outperform, with 12 funds raising $7.5 billion in H1. This was a 5x increase in 2025. The clearest sign of this momentum is fund size: KKR, RRJ, and Varde each raised Asian vehicles of more than $1bn.

📕Nick’s Top Articles for Q2

Institutional Investors are Coming Back to Direct Lending

Institutional investors are coming back to direct lending and saying, okay, I see all these headlines about wealth, that should mean that risk/reward is getting better on new deals.

And therefore, I’m going to take a fresh look at it again.

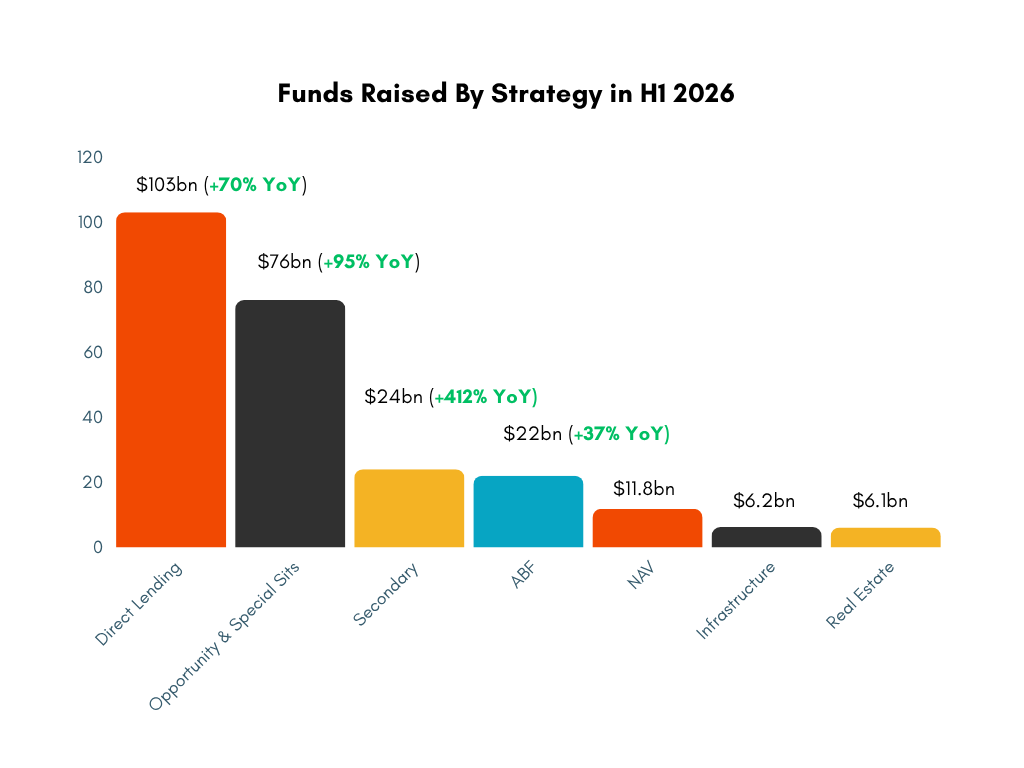

This was the second biggest insight of the quarter: Direct lending is still very much alive. Five of the top 10 funds were direct lending vehicles. Yes, the number of direct lending fundraises fell 35% year-on-year, but the funds that did close were twice as large on average.

Opportunistic credit remains one of the clearest growth areas, with fundraising doubling year-on-year. While many strategies saw fewer funds close, the number of opportunistic fundraises rose for the third year running.

For more on this trend, see Dispersion Is Back

Credit secondaries volume has set new highs every year since 2020. Credit secondaries fundraising is up 6 x year-on-year, with Ares $7 billion raise leading the way.

For more on this trend, see Solving Private Credit’s DPI Problem.

🏆 Nick’s Funds of the Quarter

It was only two years ago that Barings lost a meaningful portion of its team to Nomura. They’ve now managed to raise the largest fund I’ve recorded in 2026, despite this setback and despite being a direct lending fund.

Secondaries are going to reshape the private credit landscape over the next five years, and I expect Stepstone to play a key part in this.

Secondaries also appear to be a key focus for Ares. Ares Alt Credit team supported the Stepstone transaction, its Secondaries team led the Antares and Arcmont continuation funds, and the firm raised a $7bn credit secondaries fund in Q1.

While the “SaaS apocalypse” took most of the media attention, Crescent Cove showed that specialist managers can still raise capital in less obvious corners of the market.

Crescent Cove lends to high-growth technology businesses, including businesses operating in defense tech, autonomous driving, AI infrastructure, and cybersecurity.