Credit Crunch H1 Recap

Europe Outperforms, Direct Lending Slows, and Mega Funds Shrink

👋 Hey, Nick here. A big welcome to the new subscribers at Apollo, Goldman Sachs, and Credcore. This is the 121st edition of my weekly newsletter. Each week, I write about private credit insights and fundraising announcements. You can read my previous articles here and subscribe here.

📊 2025 Fundraising Recap

With Q2 behind us, here are my top insights for H1. This recap isn’t exhaustive, and with a bit of luck, it’s enough to keep you ahead of 99% of your peers.

Key H1 stats 📈

Number of fundraising announcements covered: 102 (Up 34% YoY)

Amount raised: $197 billion (Up 12% YoY)

Number of fund managers covered: 109 (Up 30% YoY)

Number of Countries where funds were based: 19 (Up 6% YoY)

Scroll down to the bottom if you’re here for my Fund’s of the Quarter.

Private Credit Fundraising Declines in Q2

Europe Outperforms 🌎

🇪🇺 European-focused funds raised 50% more in H125 compared to last year, with 41 funds raising $65 billion.

This was a massive outperformance compared to the US-focused fundraising, which declined YoY.

Looking for context? I broke this trend down in two newsletters, Apollo, Pictet.

🇺🇸 US private credit funds continue to raise the most capital, with 61 funds raising $126 billion in the first half of 2025.

📕Nick’s Top Articles of the Quarter

Three Nonconventional Takes on the Private Credit’s “Crowded Market”

“Origination Is the Key to Growth”: How HPS and BlackRock Plan to Win Private Credit

Why Apollo Thinks Europe is the Key to Private Credit's Growth

Is Direct Lending Overcrowded?

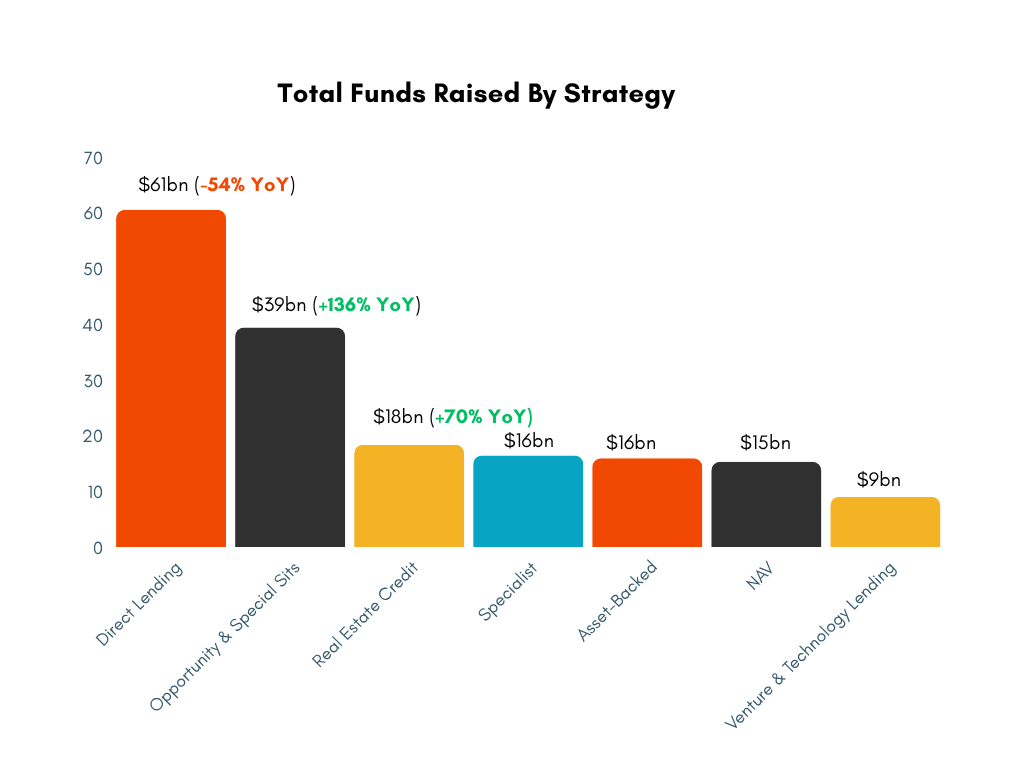

Opportunity fundraising outperformed in H1, raising more than double compared to last year.

Oaktree’s $16 billion fund was the clear outlier.

Looking for context? Howard Marks explained why Oaktree is accelerating the deployment of its Opportunity Fund. (Link)

Direct Lending continues to underperform, raising less than half of what was raised last year.

Finally, Real Estate Credit is coming back. KKR and Brookfield both wrote about this trend. (KKR, Brookfield)

The Five Largest Funds Raised in Over a Third of the Capital…

The $10B Club is Getting Smaller

Large funds (>$1 billion) continue to raise the bulk of capital, but appetite for the largest funds (>$10 billion) slowed in H1. Capital raised by funds with more than $10 billion dropped by 50% YoY.

The average fund size also declined 25% YoY to $1.7 billion

🏆 Nick’s Funds of the Quarter

Proof that private credit is more than senior and “special sits.”

🏝️ KSL Capital Partners’ $1.4 billion Tactical Opportunities II Fund

In a market that shuns cyclicality, KSL shows that you can be non-consensus and succeed. Specializing in travel and leisure investing, KSL has invested in businesses such as The Rosewood Bermuda, Camelback Ski Resort, and Heritage Golf Group.

🛫 SKY Leasing’s $1.35 billion Fund VI.

The team at SKY Leasing has deployed more than $20 billion in aircraft transactions and sold three of its prior franchises. Whilst the largest managers are only beginning to focus on these assets, SKY Leasing shows that the opportunity has been around for years.

See Oaktree’s and PIMCO’s thoughts on aviation leasing, Oaktree, PIMCO

🔐 Apollo’s Diversified Credit Securitize Fund

Using the blockchain for private credit is something I’ve actively dismissed. Apollo’s Securitize feeder fund made me question this assumption. It’s already raised more than $100 million and allows investors to invest using cryptocurrencies such as Ethereum or Solana. I’m not expecting a flood of capital, but it does introduce two interesting innovations to the industry. Firstly, 24/7 liquidity and secondly, the ability for UNHW investors to leverage their private credit assets.

If you’re looking to understand this, I’d highly recommend this deep dive into the Fasanara Tokenized fund.

A reminder that you can still launch a small, niche strategy in private credit. UK-based BFS Marine announced it raised ~$30 million for its Marine Fund. The fund will help smaller marine businesses acquire newer vessels to expand or upgrade their existing coastal fleets.

🌱 Legal & General’s $235 million Nature and Social Outcomes Strategy

ESG may be out of fashion, but there’s still room to work in private credit and do good for the world. L&G will target habitat and biodiversity conservation, as well as socially beneficial infrastructure to support education, healthcare, and access to clean water.

This newsletter is for educational or entertainment purposes only. It should not be taken as investment advice.